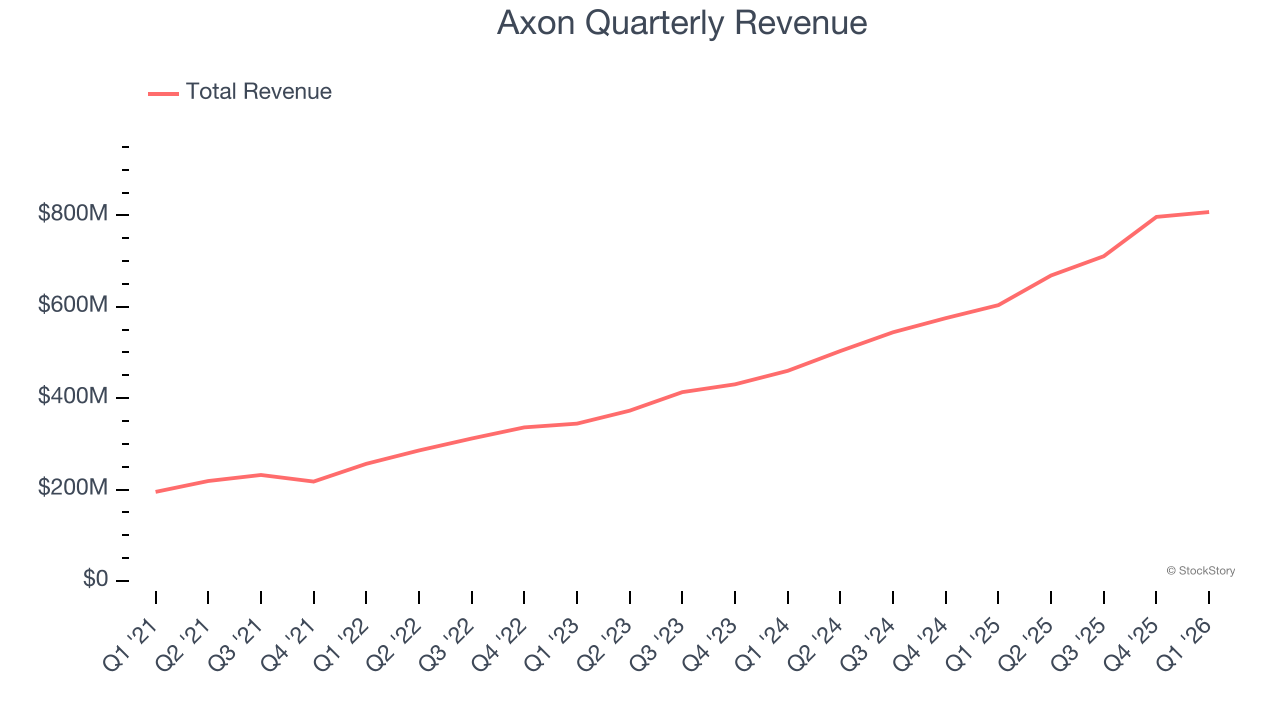

Self defense company AXON (NASDAQ: AXON) announced better-than-expected revenue in Q1 CY2026, with sales up 33.7% year on year to $807.3 million. Its non-GAAP profit of $1.61 per share was 0.8% above analysts’ consensus estimates.

Is now the time to buy Axon? Find out by accessing our full research report, it’s free.

Axon (AXON) Q1 CY2026 Highlights:

- Revenue: $807.3 million vs analyst estimates of $778.6 million (33.7% year-on-year growth, 3.7% beat)

- Adjusted EPS: $1.61 vs analyst estimates of $1.60 (0.8% beat)

- Adjusted EBITDA: $201.6 million vs analyst estimates of $181.4 million (25% margin, 11.1% beat)

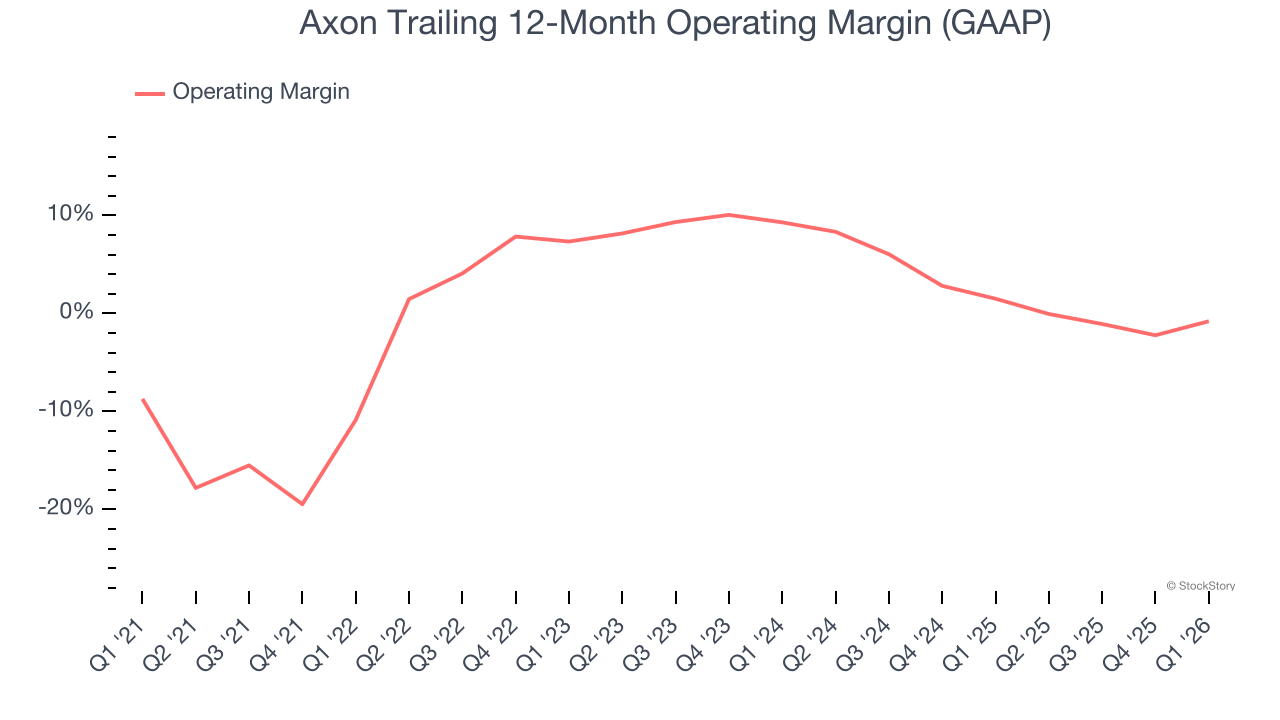

- Operating Margin: 3.6%, up from -1.5% in the same quarter last year

- Free Cash Flow was -$54.64 million, down from $2.71 million in the same quarter last year

- Market Capitalization: $30.67 billion

Company Overview

Providing body cameras and tasers for first responders, AXON (NASDAQ: AXON) develops technology solutions and weapons products for military, law enforcement, and civilians.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Axon’s 32.6% annualized revenue growth over the last five years was incredible. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Axon’s annualized revenue growth of 33.4% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

This quarter, Axon reported wonderful year-on-year revenue growth of 33.7%, and its $807.3 million of revenue exceeded Wall Street’s estimates by 3.7%.

Looking ahead, sell-side analysts expect revenue to grow 28.7% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is healthy and indicates the market is baking in success for its products and services.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Axon was profitable over the last five years but held back by its large cost base. Its average operating margin of 1.7% was weak for an industrials business.

On the plus side, Axon’s operating margin rose by 10.1 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q1, Axon generated an operating margin profit margin of 3.6%, up 5.1 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

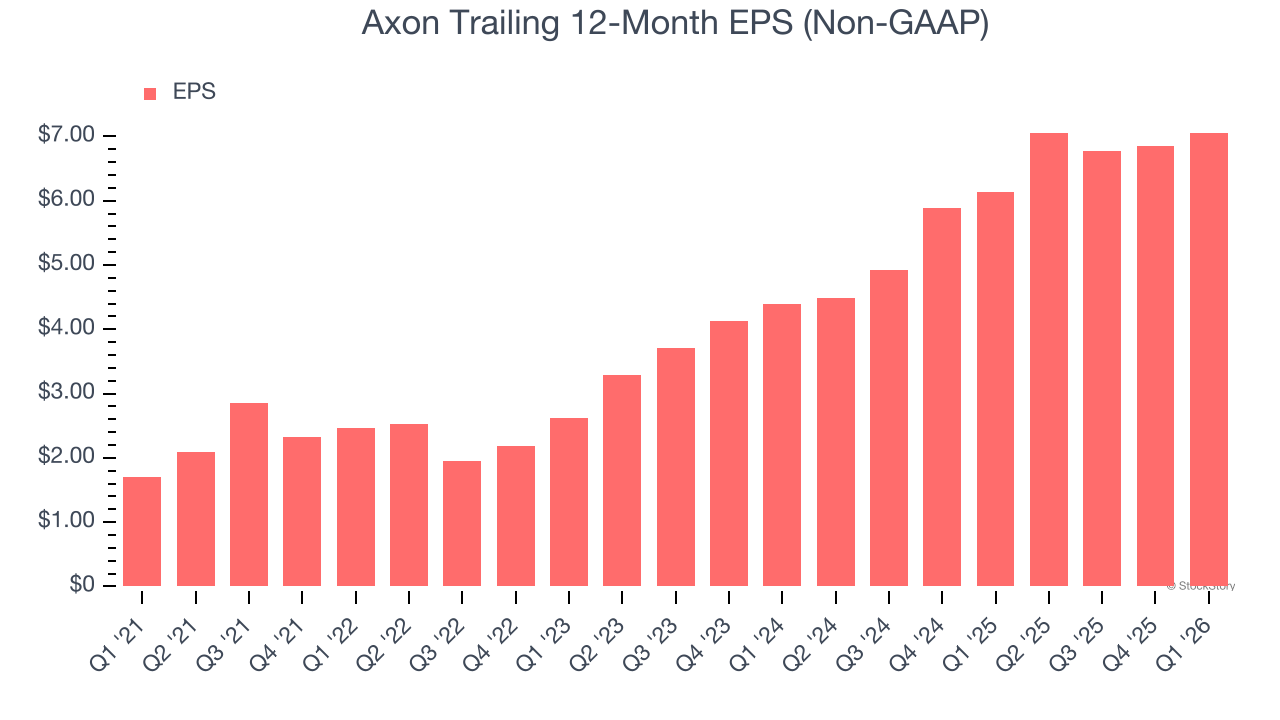

Axon’s astounding 32.9% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

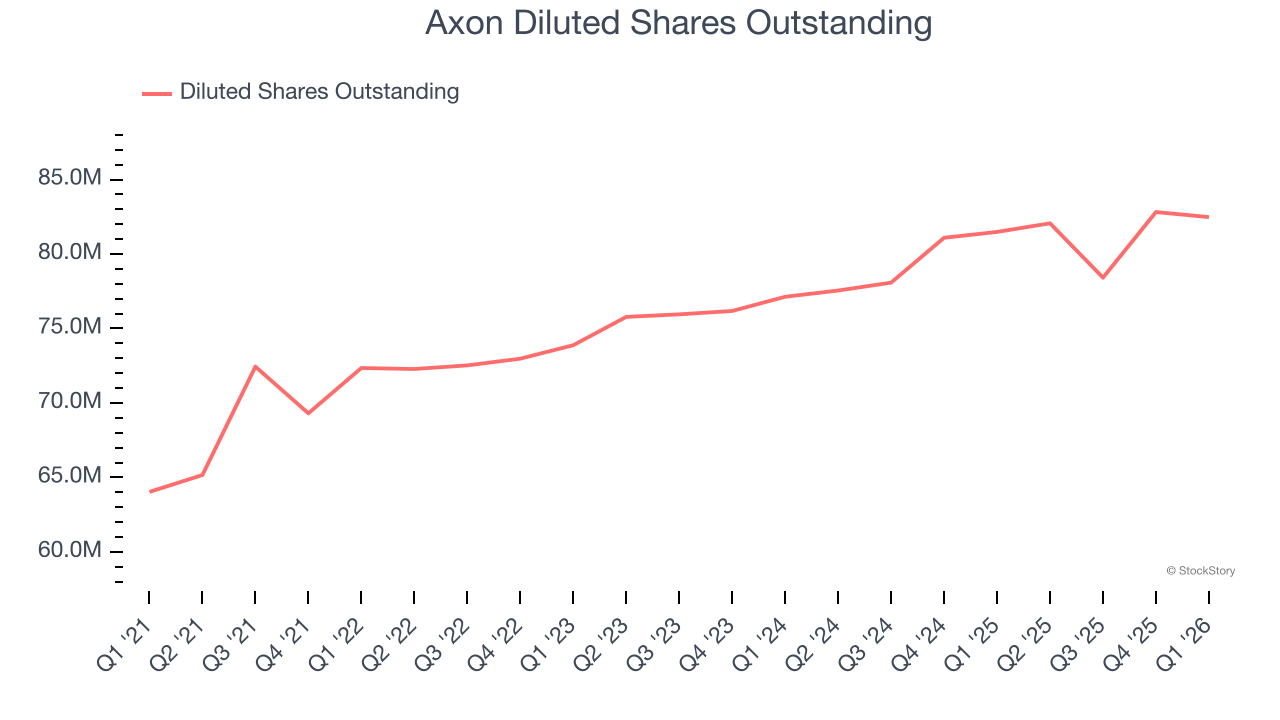

Although it performed well, Axon’s two-year annual EPS growth of 26.6% lower than its 33.4% two-year revenue growth.

We can take a deeper look into Axon’s earnings to better understand the drivers of its performance. A two-year view shows Axon has diluted its shareholders, growing its share count by 6.9%. This has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, Axon reported adjusted EPS of $1.61, up from $1.41 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Axon’s full-year EPS of $7.05 to grow 18.3%.

Key Takeaways from Axon’s Q1 Results

We were impressed by how significantly Axon blew past analysts’ EBITDA expectations this quarter. We were also excited its adjusted operating income outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock traded up 1.1% to $390.46 immediately following the results.

Axon put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).