Tesla (TSLA) is a vertically integrated American company with a focus on automotive manufacturing, energy storage, and artificial intelligence. The company has expanded from its luxury electric vehicles like the Model S and X to mass-market products like the Model 3 and Y.

Founded in 2003, the company is headquartered in Austin, Texas, and headed by billionaire Elon Musk. Today, Tesla is pivoting towards physical AI with its Full Self-Driving (FSD) software and Robotaxi, aiming to become a leader in autonomous robotics.

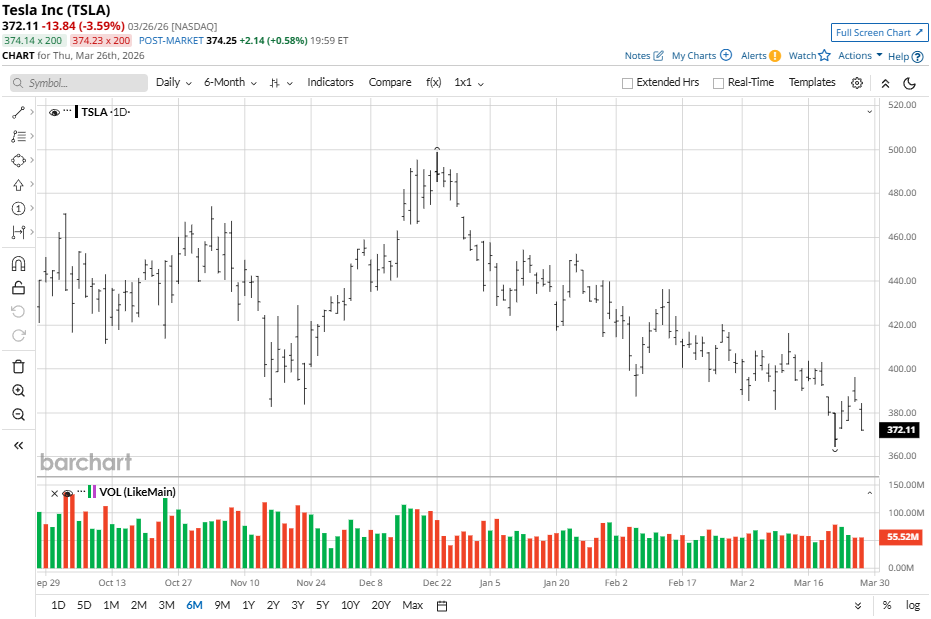

Tesla Stock Recovers from Volatility

Tesla’s stock continues to recover from a volatile 2025, which saw the company face back-to-back vehicle delivery declines. However, despite the issues, its stock has rebounded over 25% from 52-week lows thanks to robotaxi enthusiasm.

In comparison to the S&P 500 Consumer Discretionary Index ($SRCD), which has seen a 6% growth over the last year, Tesla’s performance has been more erratic due to its dual identity as a tech and auto stock.

Tesla Quarterly Results

Tesla concluded Q4 2025 with a revenue of $24.9 billion, a slight beat on market estimates despite falling 11% year-over-year (YoY) in automotive revenue. The company posted diluted EPS of $0.50 per share, beating analysts’ $0.45 per share estimates, while its net income landed at $3.8 billion.

The energy storage segment was reported as a top performer during the quarter with a record 14.2 GWh, taking the yearly total to 46.7 GWh and $12.8 billion in annual revenue. This eases pressure from Tesla’s highly competitive automotive segment, helping Tesla maintain its gross margin at 18%.

Looking ahead, Tesla CEO Elon Musk has pointed towards a massive “CapEx year” with expenditure surpassing the $20 billion mark, with support to its AI training and Cybercab production. The company aims for a full-scale volume ramp-up for its Robotaxi by mid-year. Tesla’s delivery guidance for the current quarter remains cautious, with 1.65 million units and an expected 1.1 million active FSD subscribers.

Analysts Bearish on Delivery Forecast

Tesla is expected to release its Q1 delivery numbers next week on April 2, with analysts queuing for another decline. RBC Capital estimates 367,000 deliveries, slightly below the consensus 370,000 estimate. This dip reflects a seasonal slowdown coupled with the absence of U.S. electric vehicle tax credits.

UBS calls for just 345,000 units delivered, citing softening demand from China and Europe.

RBC Capital analyst Tom Narayan points out that Tesla’s soft delivery consensus comes amid the company’s transition as it discontinues Model S and X in Q2 2026 to shift its focus towards its Robotaxi and Optimus Humanoid robot. However, elevated fuel prices should work in favor of the EV company in the near term.

Tesla bulls will point out that the company’s true value lies in its AI and autonomy segment; however, Tesla’s automotive business still remains its primary engine for cash flow.

Should You Get TSLA Stock?

Tesla remains a high-stakes play on autonomous robotics and AI despite near-term headwinds. Although the Q1 forecast suggests deliveries decline, the company’s shift to Robotaxi and Optimus robot continues to be an exciting part for investors.

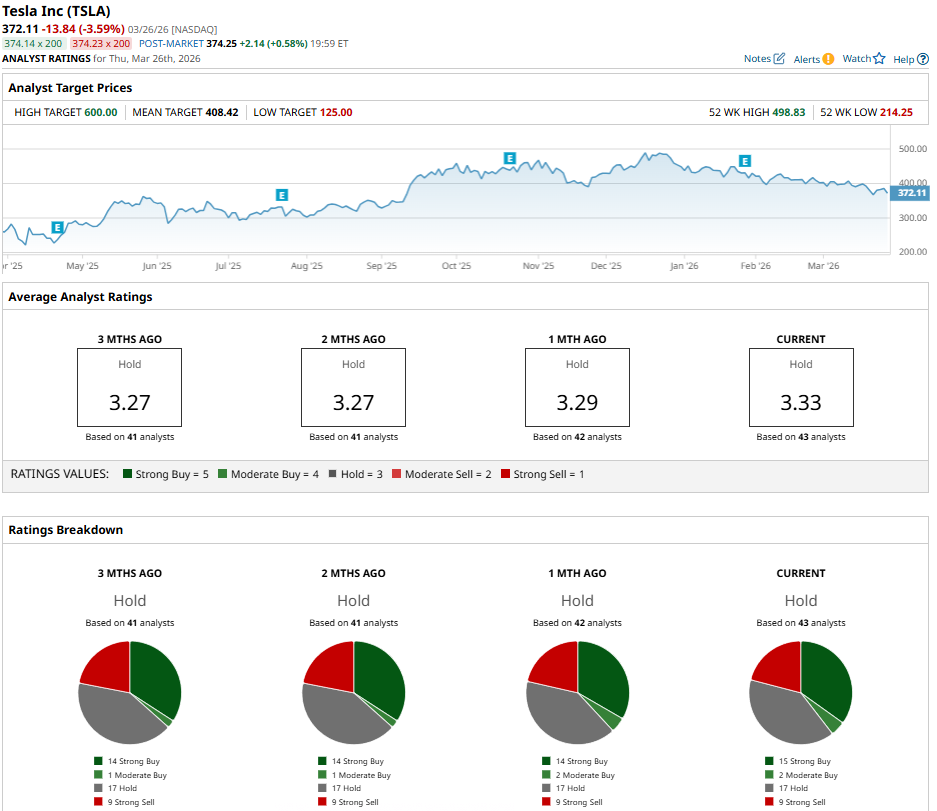

TSLA stock has a consensus “Hold” rating from 43 analysts with a diverse split of 17 “Buy” ratings, nine “Strong Sell” ratings, and 17 “Hold” ratings. A mean price target of $408.42 suggests a modest 10% upside potential for investors.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart