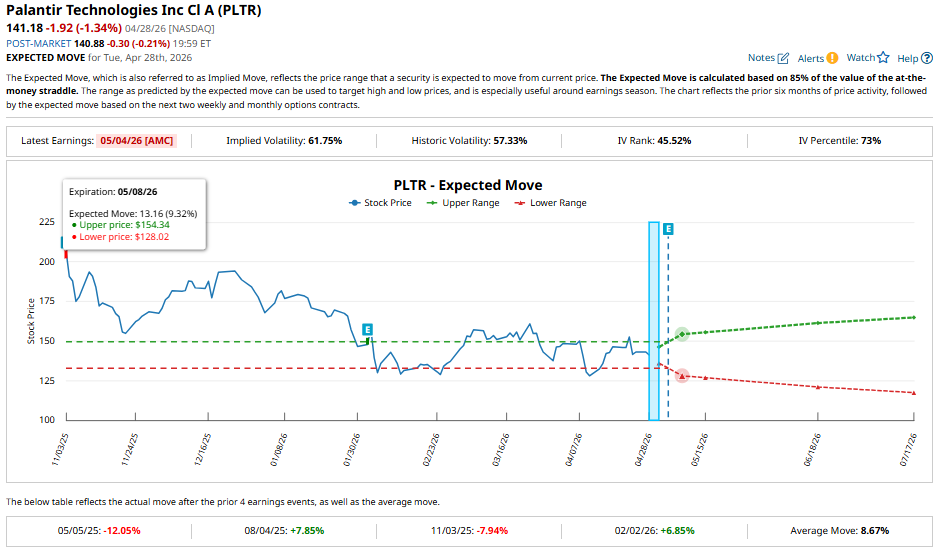

Palantir (PLTR) will release its Q1 earnings on May 4. However, ahead of the earnings report, PLTR stock has declined approximately 24% year-to-date (YTD) and now trades about 32% below its 52-week high, reflecting a notable shift in investor sentiment.

The pullback in PLTR stock appears to be driven less by deterioration in operating performance and more by concerns around valuation and competitive positioning in an increasingly crowded artificial intelligence landscape.

Prior to the recent decline, PLTR stock commanded a significantly high valuation relative to its peers, pricing in strong growth expectations for its artificial intelligence (AI) initiatives. At the same time, competitive dynamics within the AI sector have evolved rapidly. The emergence of advanced models from players such as Anthropic has introduced credible alternatives, raising questions about the durability of software providers’ competitive moats and their ability to sustain long-term pricing power.

However, Palantir’s underlying fundamentals remain solid. Demand for Palantir’s Artificial Intelligence Platform (AIP) remains robust, supporting both expansion within existing accounts and new customer acquisition. Additionally, the company is growing its profitability at a solid pace, which strengthens its investment appeal and is likely to spark a recovery in PLTR stock.

Looking ahead, the upcoming first-quarter earnings release could serve as a catalyst for Palantir's stock. Strong execution, continued acceleration in the top-line growth rate, and expanding margins could lift PLTR stock higher.

Market expectations suggest heightened volatility in PLTR stock relative to recent earnings cycles. Options pricing suggests a potential post-earnings move of approximately 9.3% in either direction, up from the average 8.7% move observed over the past four quarters.

Palantir to Deliver Massive Growth in Q1

Palantir appears well-positioned to deliver another quarter of outsized growth, extending its streak of accelerating revenue. The company’s quarterly revenue growth rate has climbed sharply, from 36% in the fourth quarter of 2024 to 70% by the fourth quarter of 2025. This reflects strong adoption of its AIP.

The company’s guidance suggests this trajectory may continue into the first quarter of 2026, with management projecting revenue of $1.532 billion to $1.536 billion, implying approximately 74% year-over-year (YoY) growth at the midpoint.

The acceleration of its top-line growth rate is likely to be driven by sustained momentum in the U.S. business. In the previous quarter, U.S. revenue surged 93% YoY, supported by both commercial and government demand. Within this segment, the commercial business stands out as a key catalyst. It delivered a 137% increase in revenue in Q4 2025, driven by the rapid enterprise adoption of AIP solutions, which is leading to customer expansion and new client acquisition.

The U.S. government business is also likely to contribute meaningfully to its top line in Q1. The business is expected to benefit from continued execution on existing contracts and incremental program wins, reflecting a broader structural shift toward AI-enabled software.

Supporting Palantir's strong outlook is its growing customer base. Customer count increased 34% YoY to 954 in Q4. At the high end of the customer spectrum, spending intensity is also rising. Notably, trailing twelve-month revenue per top-20 customer reached $94 million in Q4, up 45% YoY. Meanwhile, total contract value (TCV) bookings hit a record $4.3 billion in the fourth quarter, representing a 138% increase. This surge in bookings provides a solid pipeline for future growth.

Palantir’s profitability is also growing rapidly. For Q1 2026, Palantir expects adjusted operating income between $870 million and $874 million, indicating solid YoY and sequential growth.

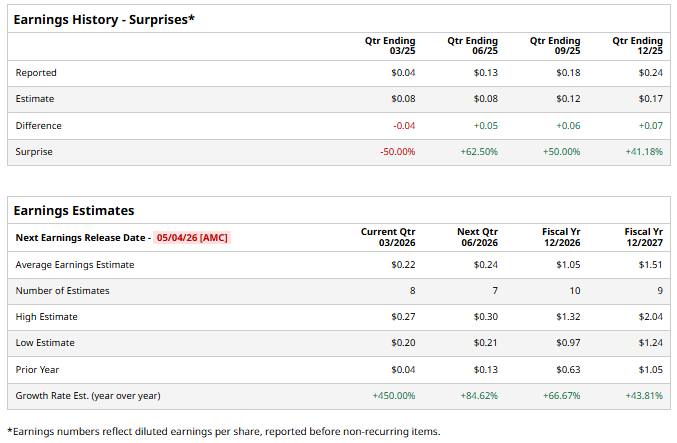

On the bottom line, the company has consistently outperformed market expectations, beating analyst EPS estimates by a wide margin in each of the past three quarters. For the upcoming quarter, consensus forecasts call for earnings of $0.22 per share, a substantial increase from $0.04 in the prior-year period. If historical trends persist, there remains potential for further upside relative to analysts’ estimates.

Will Q1 Lift PLTR Stock?

Analysts maintain a “Hold” consensus rating on Palantir stock ahead of Q1 earnings. However, the expected acceleration in Palantir’s revenue growth, led by higher adoption of AIP, an expanding customer base, record contract bookings, and improving profitability, points to a recovery in PLTR stock. Moreover, valuation concerns have eased moderately following the recent pullback in its share price.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Semiconductor Stocks Are the New Elephant in the Room at 14% of the S&P 500. How to Play This Tech Super-Sector.

- As Alibaba Rolls Out the Happy Horse AI Model, Should You Buy, Sell, or Hold BABA Stock?

- Seagate Technology Just Landed a $1,000 Price Target. Should You Buy Shares Here?

- As Uber Breaks Into Travel, Is Uber Stock a Buy, Sell, or Hold?