Dublin, Ireland-based Smurfit Westrock Plc (SW) manufactures, distributes, and sells containerboard, corrugated containers, and other paper-based packaging products in North America and internationally. The company has a market cap of $21 billion and produces containerboard and paperboard, packaging of corrugated containers, consumer packaging, and offers solid board, kraft paper, and graphic board, among others.

SW shares have lagged behind the broader market over the past year, declined 14.1% compared to the S&P 500 Index ($SPX) 27.3% surge. Moreover, in 2026, the stock has grown nearly 3.5%, underperforming the SPX’s 9.6% rise as well.

Focusing on its industry benchmark, the State Street Consumer Discretionary Select Sector SPDR ETF (XLY) has risen 9.8% over the past year, outperforming the stock. In 2026, XLY has declined marginally and has lagged behind the stock.

On Apr. 30, SW stock declined 3.3% following the release of its Q1 2026 earnings. The company’s net sales totaled $7.7 billion, and its adjusted EPS was $0.33, down from $0.68 in the previous year’s quarter. Management cited adverse weather events, primarily in its North American business, as the reason for its negatively impacted net income and adjusted EBITDA, both of which fell from their values last year.

For the current year, which ends in December, analysts expect SW’s EPS to rise 13.2% to $2.32 on a diluted basis. The company failed to surpass the consensus estimate in any of the last four quarters.

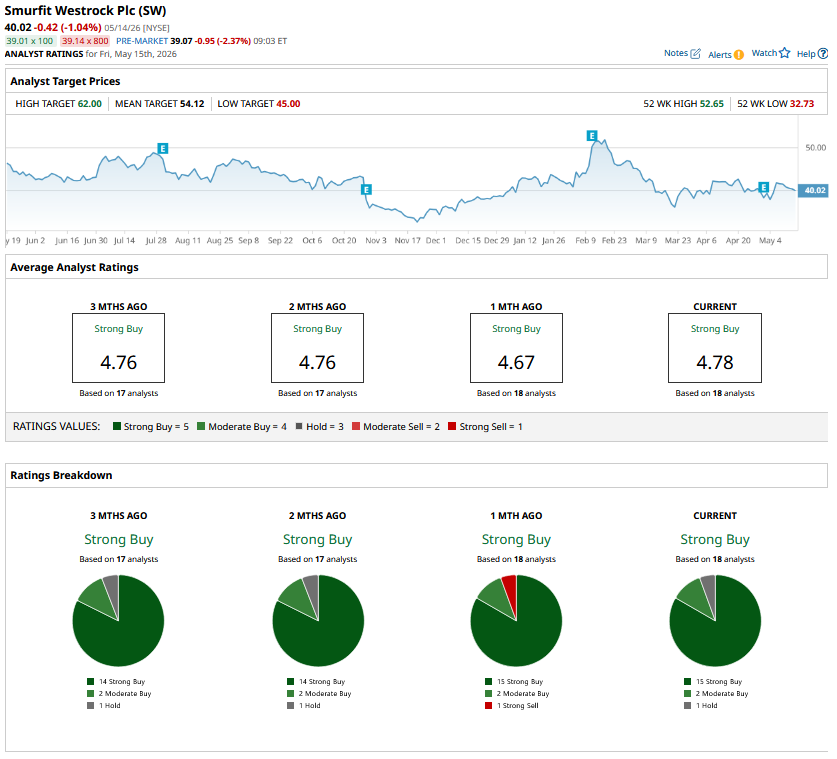

Among the 18 analysts covering SW stock, the consensus is a “Strong Buy.” That’s based on 15 “Strong Buy” ratings, two “Moderate Buys,” and one “Hold.”

The configuration has remained unchanged over the past month.

On Apr. 15, Citi analyst Anthony Pettinari maintained a “Buy” rating on Smurfit Westrock and set a price target of $53.

SW’s mean price target of $54.12 indicates a premium of 38.3% from the current market prices. Its Street-high target of $62 suggests a robust 58.4% upside potential from current price levels.

On the date of publication, Aritra Gangopadhyay did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Robust Earnings Growth and Innovation Will Help the Marvell Stock Uptrend Keep Going

- Akamai Stock Is Surging on an Analyst Upgrade. It’s No Longer a Legacy Tech Company.

- Cerebras Stock Pulls Back After Blockbuster IPO. Here's What's Next for the Potential Nvidia Rival.

- Marvell Technology Has a Hidden Growth Engine That Could Cause MRVL Stock to Skyrocket