Wrapping up Q1 earnings, we look at the numbers and key takeaways for the home builders stocks, including D.R. Horton (NYSE: DHI) and its peers.

Traditionally, homebuilders have built competitive advantages with economies of scale that lead to advantaged purchasing and brand recognition among consumers. Aesthetic trends have always been important in the space, but more recently, energy efficiency and conservation are driving innovation. However, these companies are still at the whim of the macro, specifically interest rates that heavily impact new and existing home sales. In fact, homebuilders are one of the most cyclical subsectors within industrials.

The 12 home builders stocks we track reported a slower Q1. As a group, revenues beat analysts’ consensus estimates by 0.8%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 6.8% since the latest earnings results.

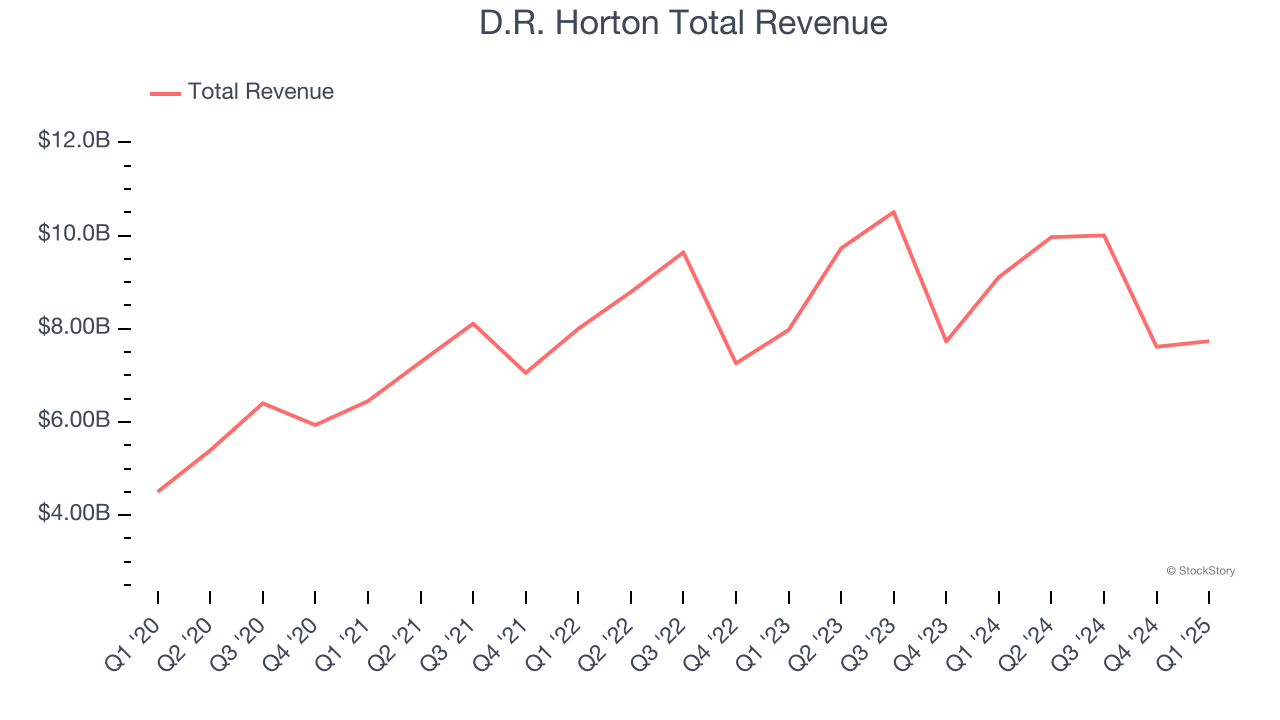

D.R. Horton (NYSE: DHI)

One of the largest homebuilding companies in the U.S., D.R. Horton (NYSE: DHI) builds a variety of new construction homes across multiple markets.

D.R. Horton reported revenues of $7.73 billion, down 15.1% year on year. This print fell short of analysts’ expectations by 3.9%. Overall, it was a disappointing quarter for the company with full-year revenue guidance missing analysts’ expectations and a significant miss of analysts’ EBITDA estimates.

David Auld, Executive Chairman, said, “For the second fiscal quarter of 2025, the D.R. Horton team delivered solid results, highlighted by earnings per diluted share of $2.58. Consolidated pre-tax income for the quarter was $1.1 billion on revenues of $7.7 billion, with a pre-tax profit margin of 13.8%. We leveraged our operational results and strong balance sheet to return $1.4 billion to shareholders through share repurchases and dividends during the quarter, and we have reduced our outstanding share count by 7% from a year ago.

D.R. Horton delivered the weakest full-year guidance update of the whole group. Interestingly, the stock is up 3.1% since reporting and currently trades at $121.28.

Read our full report on D.R. Horton here, it’s free.

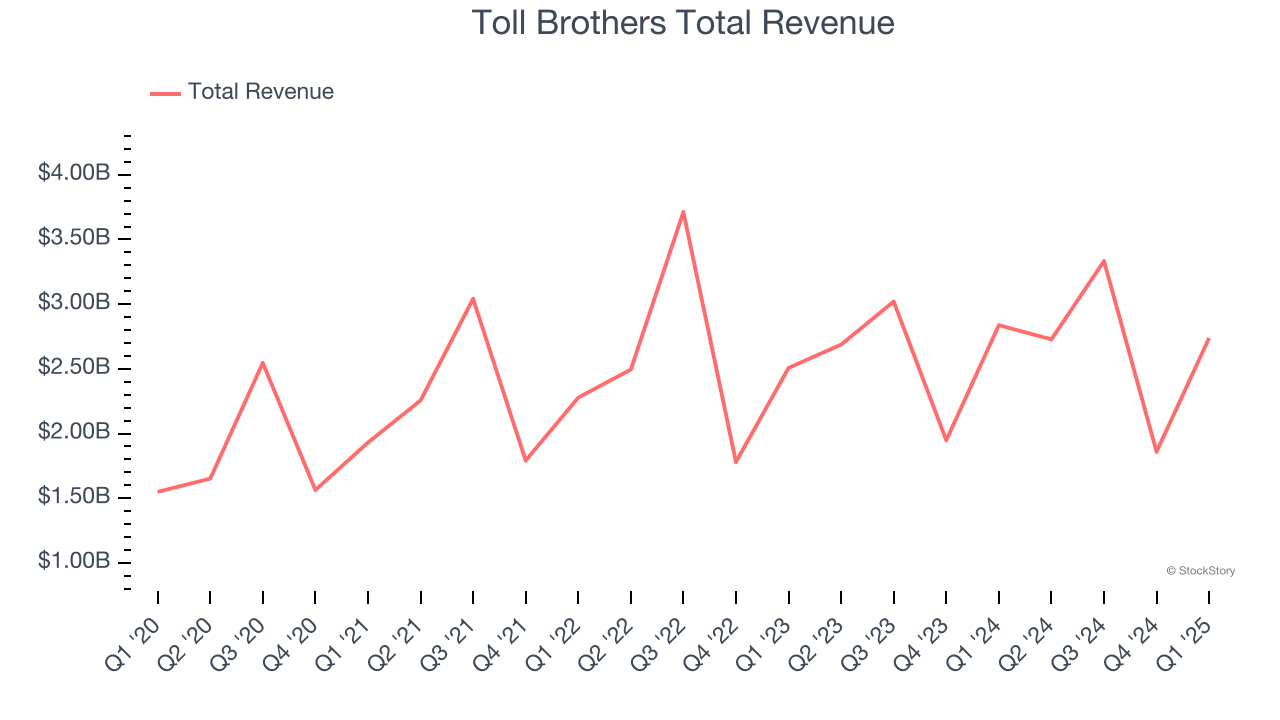

Best Q1: Toll Brothers (NYSE: TOL)

Started by two brothers who started by building and selling just one home in Pennsylvania, today Toll Brothers (NYSE: TOL) is a luxury homebuilder across the United States.

Toll Brothers reported revenues of $2.74 billion, down 3.5% year on year, outperforming analysts’ expectations by 9.9%. The business had an incredible quarter with a solid beat of analysts’ EBITDA estimates and an impressive beat of analysts’ EPS estimates.

Toll Brothers achieved the biggest analyst estimates beat among its peers. However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $105.24.

Is now the time to buy Toll Brothers? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: LGI Homes (NASDAQ: LGIH)

Based in Texas, LGI Homes (NASDAQ: LGIH) is a homebuilding company specializing in constructing affordable, entry-level single-family homes in desirable communities across the United States.

LGI Homes reported revenues of $351.4 million, down 10.1% year on year, falling short of analysts’ expectations by 5%. It was a disappointing quarter as it posted a significant miss of analysts’ adjusted operating income estimates.

As expected, the stock is down 20% since the results and currently trades at $47.35.

Read our full analysis of LGI Homes’s results here.

KB Home (NYSE: KBH)

The first homebuilder to be listed on the NYSE, KB Home (NYSE: KB) is a homebuilding company targeting the first-time home buyer and move-up buyer markets.

KB Home reported revenues of $1.39 billion, down 5.2% year on year. This print lagged analysts' expectations by 6.5%. It was a disappointing quarter as it also produced full-year revenue guidance missing analysts’ expectations.

KB Home had the weakest performance against analyst estimates among its peers. The stock is down 18.1% since reporting and currently trades at $50.62.

Read our full, actionable report on KB Home here, it’s free.

NVR (NYSE: NVR)

Known for its unique land acquisition strategy, NVR (NYSE: NVR) is a respected homebuilder and mortgage company in the United States.

NVR reported revenues of $2.40 billion, up 3% year on year. This number beat analysts’ expectations by 0.8%. Taking a step back, it was a disappointing quarter as it produced a significant miss of analysts’ adjusted operating income estimates.

The stock is down 2.3% since reporting and currently trades at $6,980.

Read our full, actionable report on NVR here, it’s free.

Market Update

In response to the Fed’s rate hikes in 2022 and 2023, inflation has been gradually trending down from its post-pandemic peak, trending closer to the Fed’s 2% target. Despite higher borrowing costs, the economy has avoided flashing recessionary signals. This is the much-desired soft landing that many investors hoped for. The recent rate cuts (0.5% in September and 0.25% in November 2024) have bolstered the stock market, making 2024 a strong year for equities. Donald Trump’s presidential win in November sparked additional market gains, sending indices to record highs in the days following his victory. However, debates continue over possible tariffs and corporate tax adjustments, raising questions about economic stability in 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.