Over the last six months, Columbia Banking System’s shares have sunk to $24, producing a disappointing 11.6% loss - a stark contrast to the S&P 500’s 2.8% gain. This may have investors wondering how to approach the situation.

Is now the time to buy Columbia Banking System, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Columbia Banking System Not Exciting?

Even with the cheaper entry price, we're sitting this one out for now. Here are three reasons why you should be careful with COLB and a stock we'd rather own.

1. Projected Net Interest Income Growth Is Slim

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Columbia Banking System’s net interest income to rise by 2.3%, a deceleration versus its 18.9% annualized growth for the past two years. This projection is below its 18.9% annualized growth rate for the past two years.

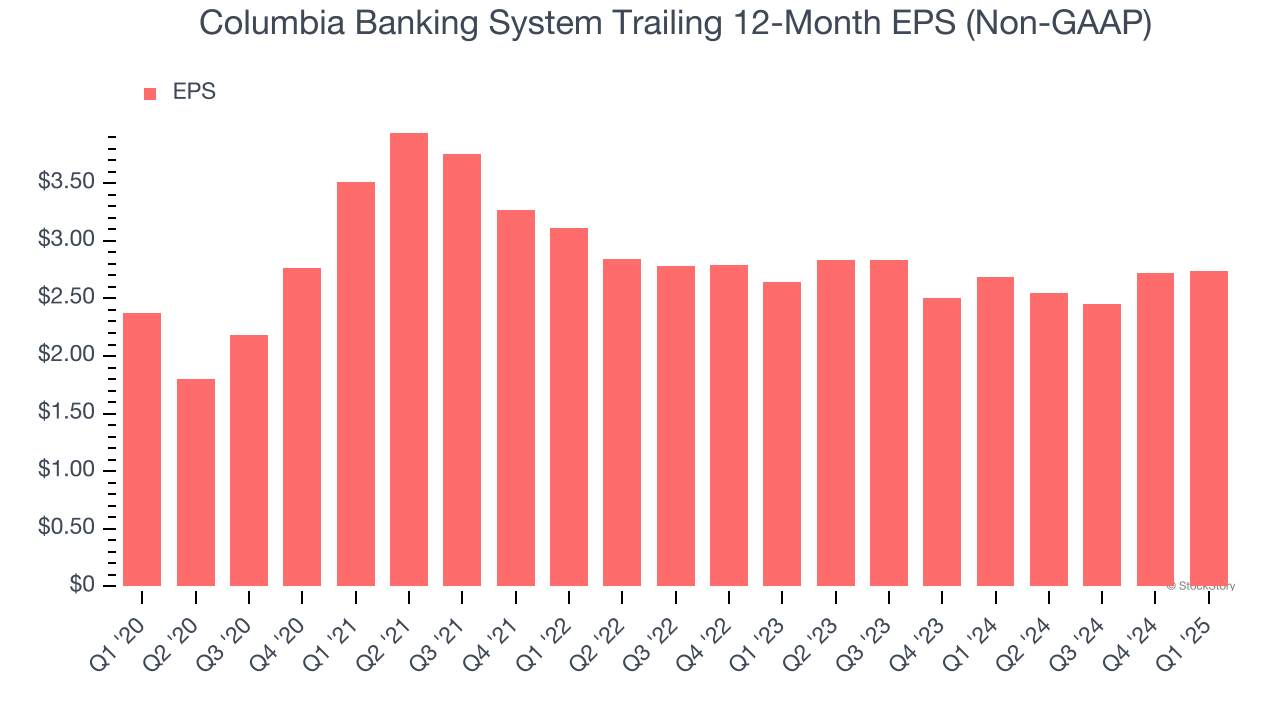

2. EPS Barely Growing

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Columbia Banking System’s EPS grew at an unimpressive 2.9% compounded annual growth rate over the last five years, lower than its 17.5% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

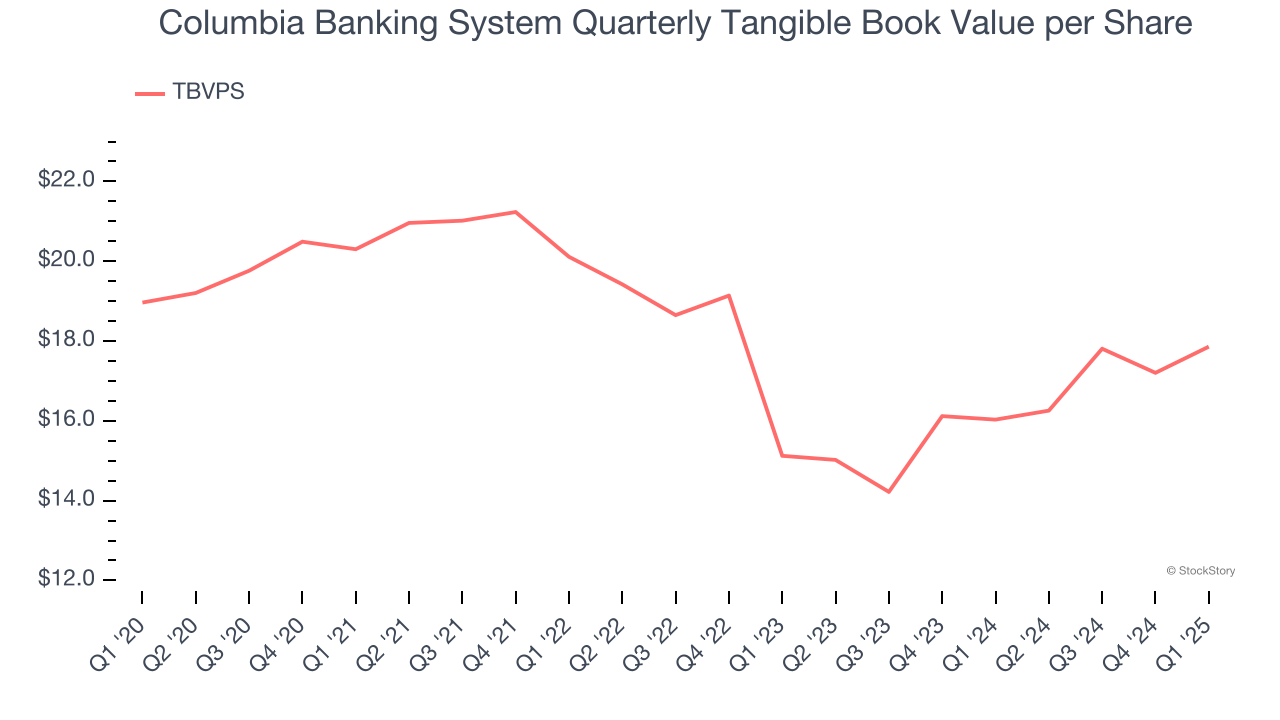

3. Substandard TBVPS Growth Indicates Limited Asset Expansion

In the banking industry, tangible book value per share (TBVPS) provides the clearest picture of shareholder value, as it focuses on concrete assets while excluding intangible items that may not hold value during challenging times.

Disappointingly for investors, Columbia Banking System’s TBVPS grew at a mediocre 8.7% annual clip over the last two years.

Final Judgment

Columbia Banking System’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 0.9× forward P/B (or $24 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. Let us point you toward an all-weather company that owns household favorite Taco Bell.

Stocks We Would Buy Instead of Columbia Banking System

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.