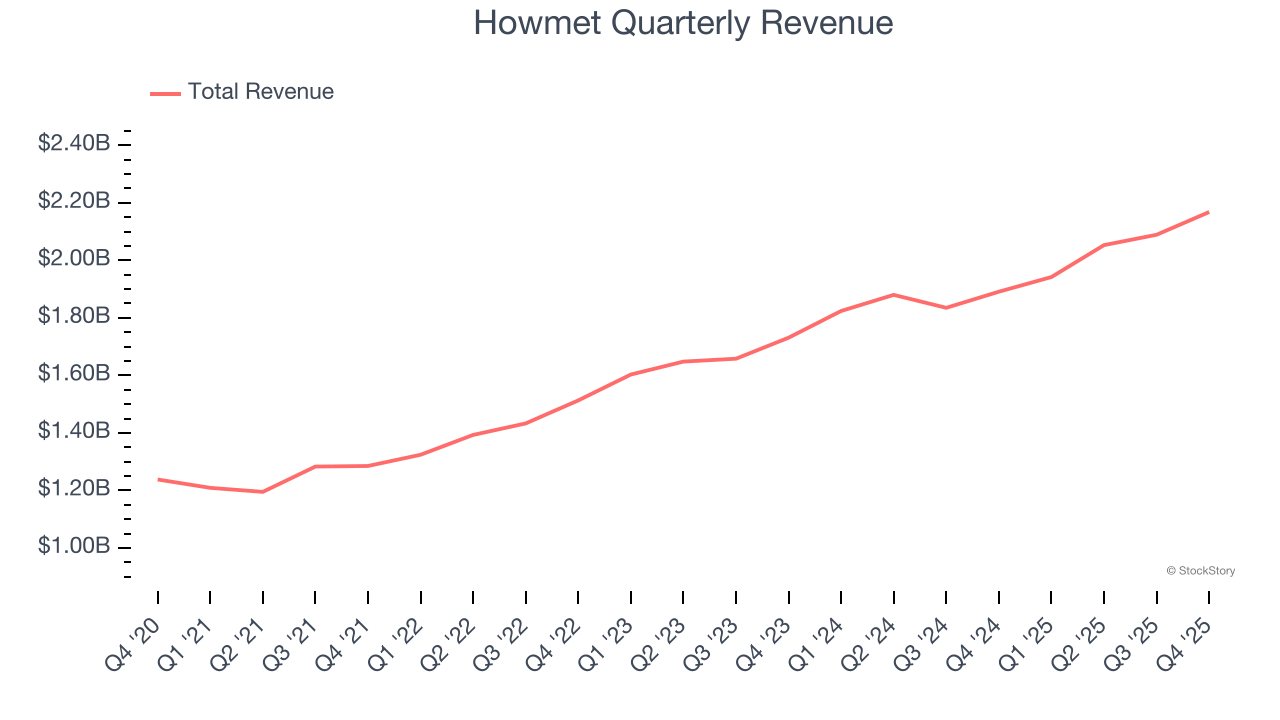

Aerospace and defense company Howmet (NYSE: HWM) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 14.6% year on year to $2.17 billion. On top of that, next quarter’s revenue guidance ($2.24 billion at the midpoint) was surprisingly good and 3.5% above what analysts were expecting. Its non-GAAP profit of $1.05 per share was 8.7% above analysts’ consensus estimates.

Is now the time to buy Howmet? Find out by accessing our full research report, it’s free.

Howmet (HWM) Q4 CY2025 Highlights:

- Revenue: $2.17 billion vs analyst estimates of $2.12 billion (14.6% year-on-year growth, 2.3% beat)

- Adjusted EPS: $1.05 vs analyst estimates of $0.97 (8.7% beat)

- Adjusted EBITDA: $650 million vs analyst estimates of $623.2 million (30% margin, 4.3% beat)

- Revenue Guidance for Q1 CY2026 is $2.24 billion at the midpoint, above analyst estimates of $2.16 billion

- Adjusted EPS guidance for the upcoming financial year 2026 is $4.45 at the midpoint, in line with analyst estimates

- EBITDA guidance for the upcoming financial year 2026 is $2.76 billion at the midpoint, in line with analyst expectations

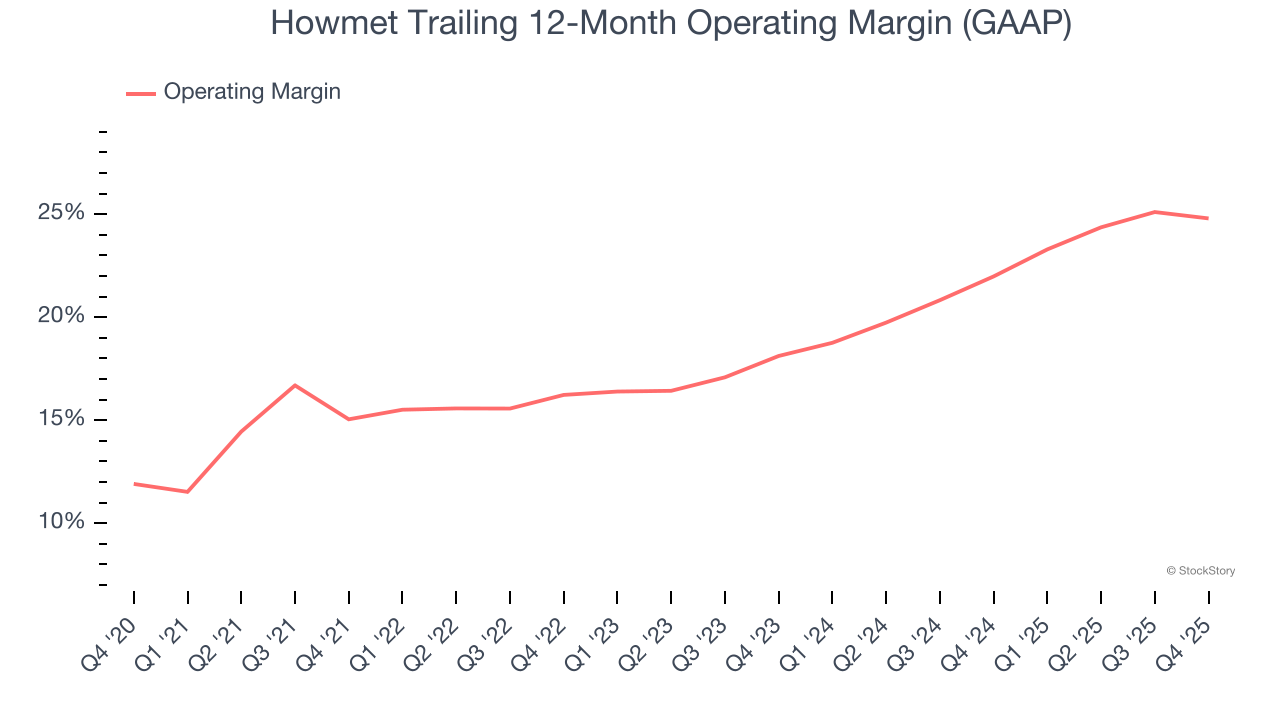

- Operating Margin: 22.6%, in line with the same quarter last year

- Free Cash Flow Margin: 24.4%, up from 20% in the same quarter last year

- Market Capitalization: $92.82 billion

Howmet Aerospace Executive Chairman and Chief Executive Officer John Plant said, "The Howmet team delivered an exceptional quarter to cap a strong 2025. Revenue growth accelerated in the fourth quarter 2025 to 15% year over year, reflecting healthy growth in the commercial aerospace, defense aerospace, and gas turbines markets. Adjusted EBITDA* grew 29% year over year to $653 million and Adjusted EBITDA Margin* increased approximately 330 basis points to 30.1%, both records. Adjusted Earnings per Share* grew 42% to a record $1.05. Free Cash Flow for full year 2025 was $1.43 billion and 93% conversion of Net Income* after record capital expenditures of $453 million as Howmet continued to invest for growth."

Company Overview

Inventing the first forged aluminum truck wheel, Howmet (NYSE: HWM) specializes in lightweight metals engineering and manufacturing multi-material components used in vehicles.

Revenue Growth

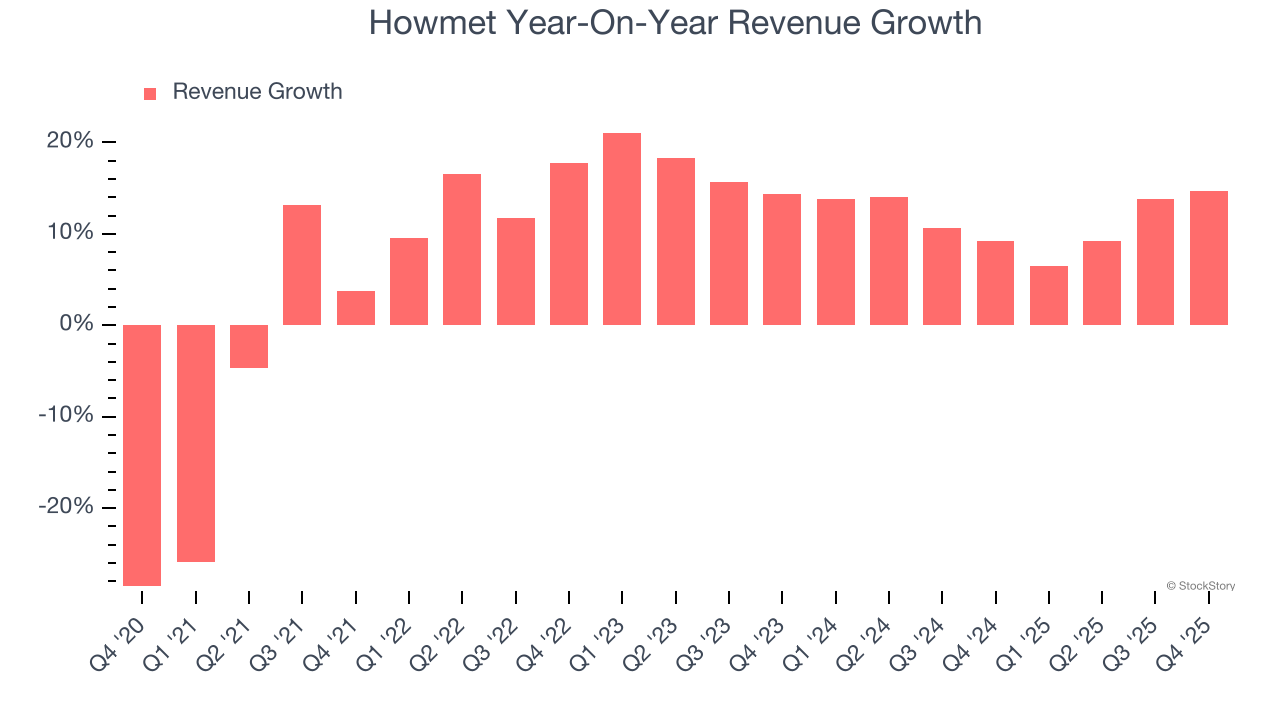

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Howmet grew its sales at a solid 9.4% compounded annual growth rate. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Howmet’s annualized revenue growth of 11.5% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

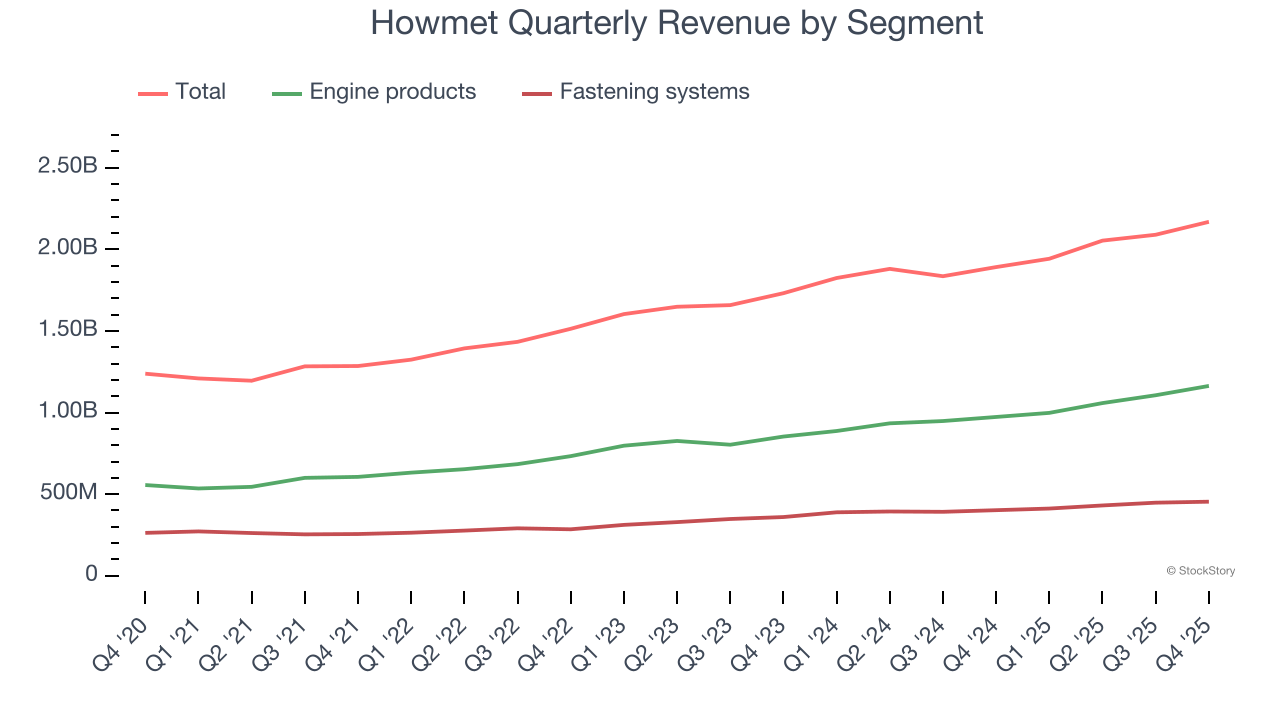

Howmet also breaks out the revenue for its most important segments, Engine products and Fastening systems, which are 53.6% and 20.9% of revenue. Over the last two years, Howmet’s Engine products revenue (aircraft engines, industrial turbines) averaged 14.8% year-on-year growth while its Fastening systems revenue (connector products and tools) averaged 13.9% growth.

This quarter, Howmet reported year-on-year revenue growth of 14.6%, and its $2.17 billion of revenue exceeded Wall Street’s estimates by 2.3%. Company management is currently guiding for a 15.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 11% over the next 12 months, similar to its two-year rate. This projection is commendable and indicates the market is baking in success for its products and services.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Howmet has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 19.9%.

Analyzing the trend in its profitability, Howmet’s operating margin rose by 9.7 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, Howmet generated an operating margin profit margin of 22.6%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

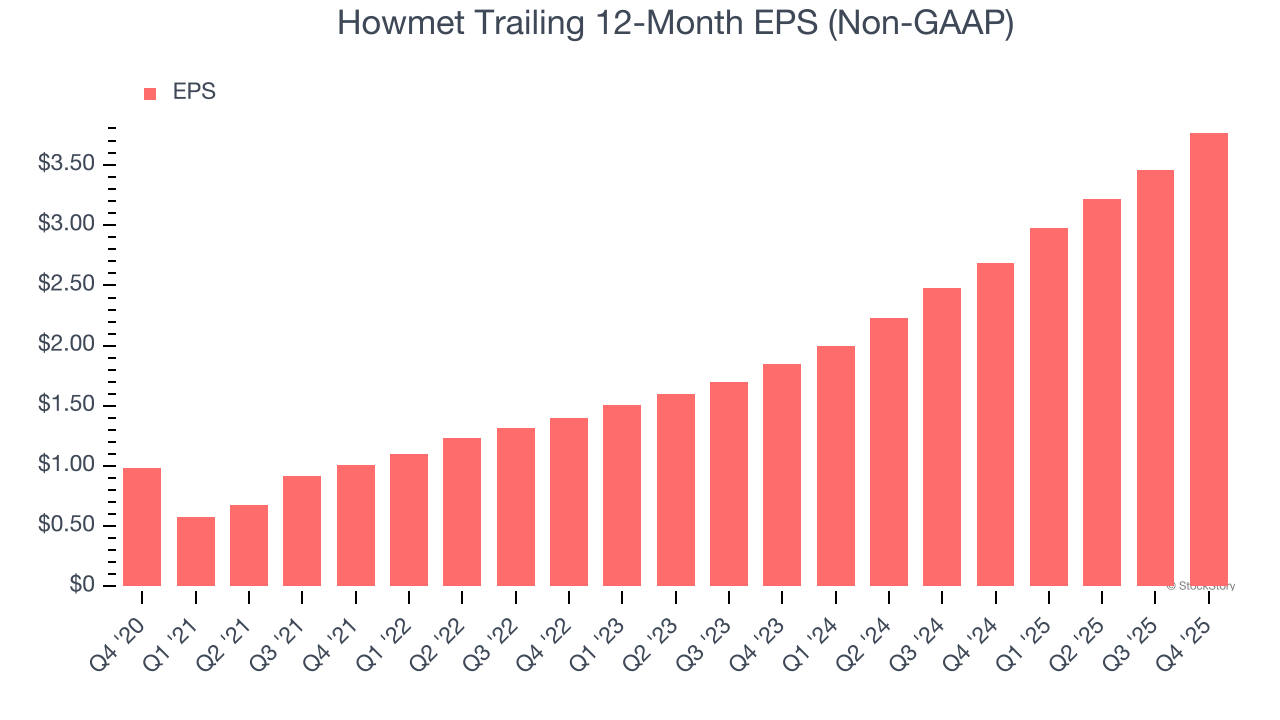

Howmet’s EPS grew at an astounding 30.9% compounded annual growth rate over the last five years, higher than its 9.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

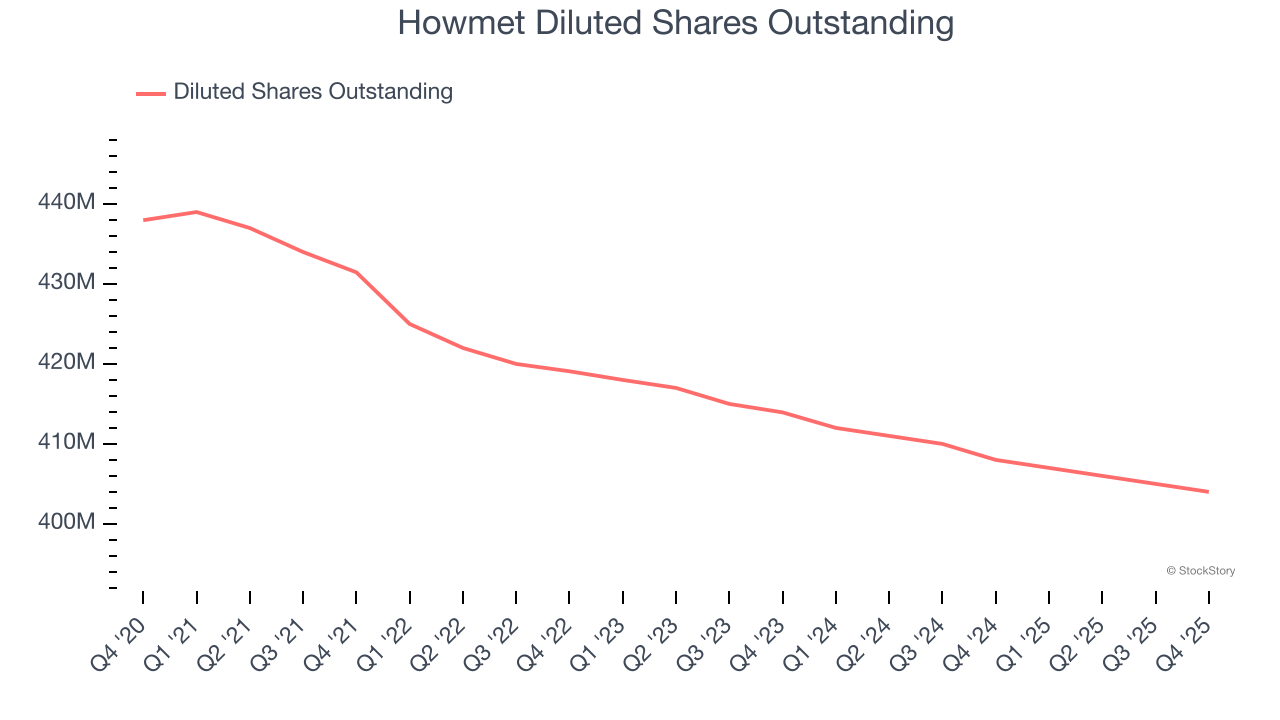

Diving into Howmet’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Howmet’s operating margin was flat this quarter but expanded by 9.7 percentage points over the last five years. On top of that, its share count shrank by 7.8%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Howmet, its two-year annual EPS growth of 42.8% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Howmet reported adjusted EPS of $1.05, up from $0.74 in the same quarter last year. This print beat analysts’ estimates by 8.7%. Over the next 12 months, Wall Street expects Howmet’s full-year EPS of $3.77 to grow 17.9%.

Key Takeaways from Howmet’s Q4 Results

It was great to see Howmet’s EBITDA guidance for next quarter top analysts’ expectations. We were also glad its Engine products revenue topped Wall Street’s estimates. On the other hand, its Fastening systems revenue missed and its full-year revenue guidance was in line with Wall Street’s estimates. Overall, we think this was still a solid quarter with some key areas of upside. The stock traded up 2.4% to $236.31 immediately after reporting.

Sure, Howmet had a solid quarter, but if we look at the bigger picture, is this stock a buy? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).