Although the S&P 500 is down 1% over the past six months, Datadog’s stock price has fallen further to $124.16, losing shareholders 14.5% of their capital. This might have investors contemplating their next move.

Following the pullback, is this a buying opportunity for DDOG? Find out in our full research report, it’s free.

Why Are We Positive On DDOG?

Named after a database the founders had to painstakingly look after at their previous company, Datadog (NASDAQ: DDOG) provides a software platform that helps organizations monitor and secure their cloud applications, infrastructure, and services.

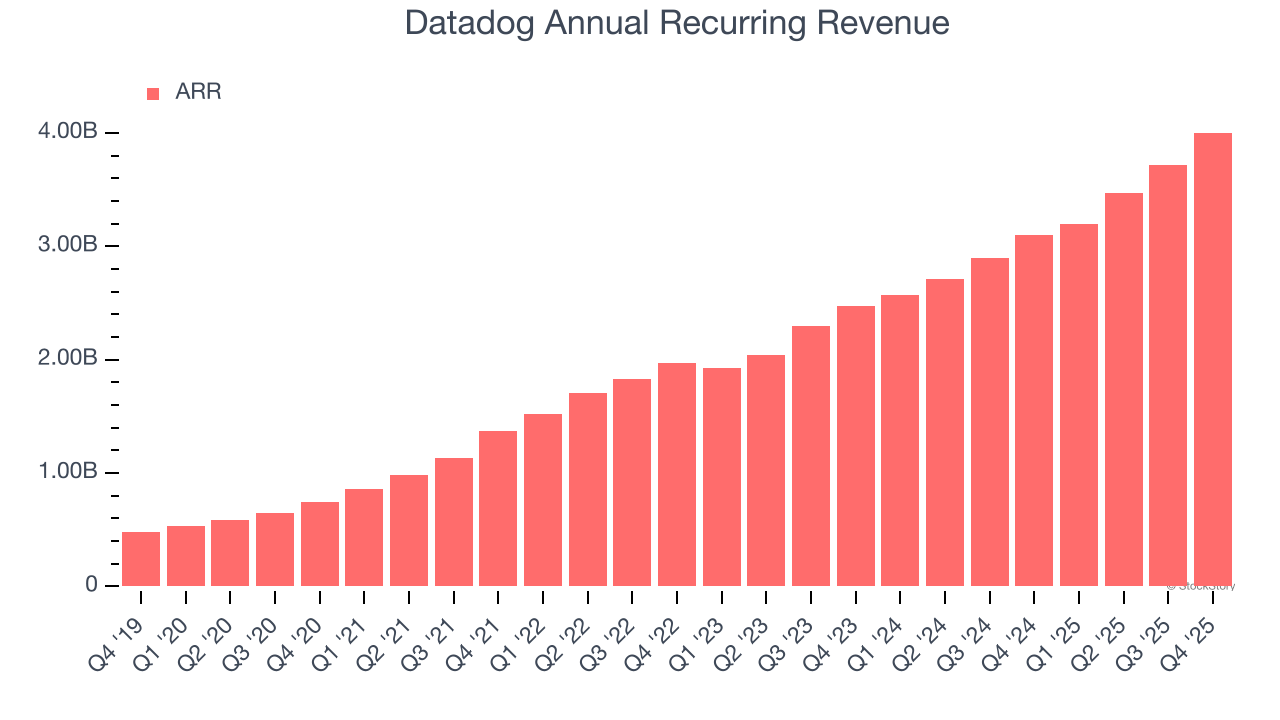

1. ARR Surges as Recurring Revenue Flows In

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Datadog’s ARR punched in at $4.00 billion in Q4, and over the last four quarters, its year-on-year growth averaged 27.6%. This performance was fantastic and shows that customers are willing to take multi-year bets on the company’s technology. Its growth also makes Datadog a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

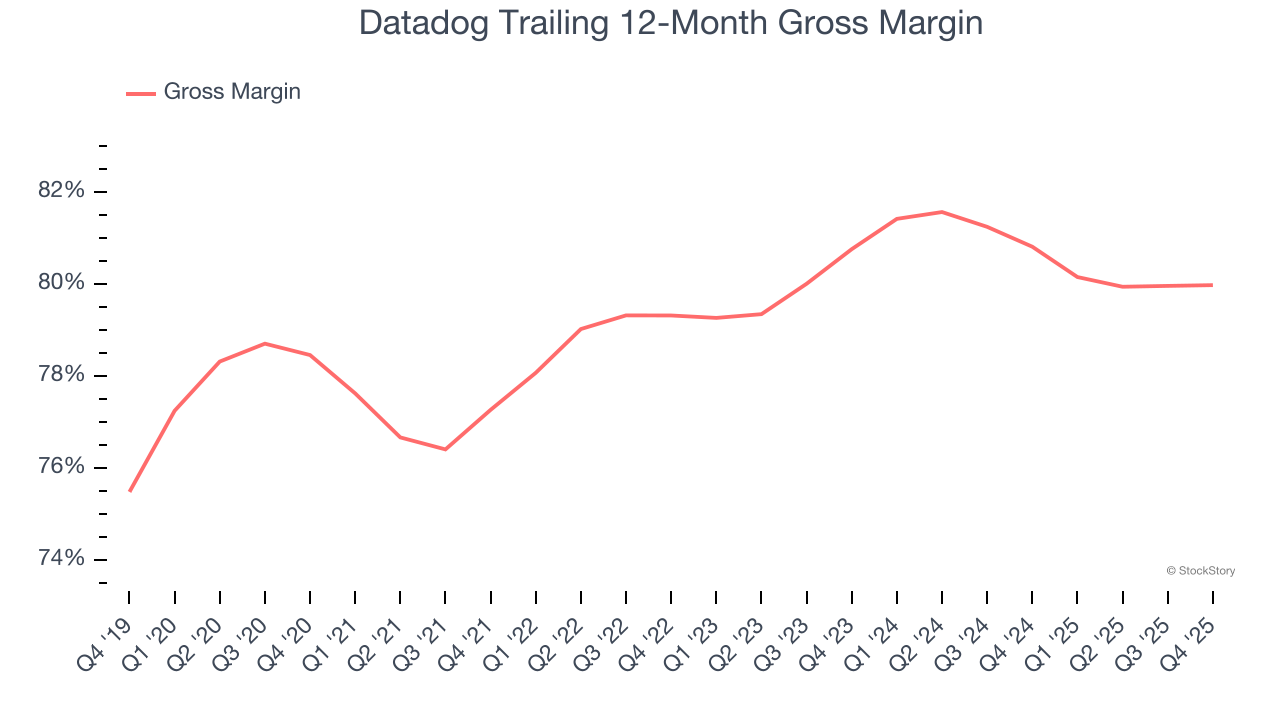

2. Elite Gross Margin Powers Best-In-Class Business Model

Software is eating the world. It’s one of our favorite business models because once you develop the product, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

Datadog’s robust unit economics are better than the broader software industry, an output of its asset-lite business model and pricing power. They also enable the company to fund large investments in new products and sales during periods of rapid growth to achieve outsized profits at scale. As you can see below, it averaged an excellent 80% gross margin over the last year. Said differently, roughly $79.98 was left to spend on selling, marketing, and R&D for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Datadog has seen gross margins decline by 0.8 percentage points over the last 2 year, which is slightly worse than average for software.

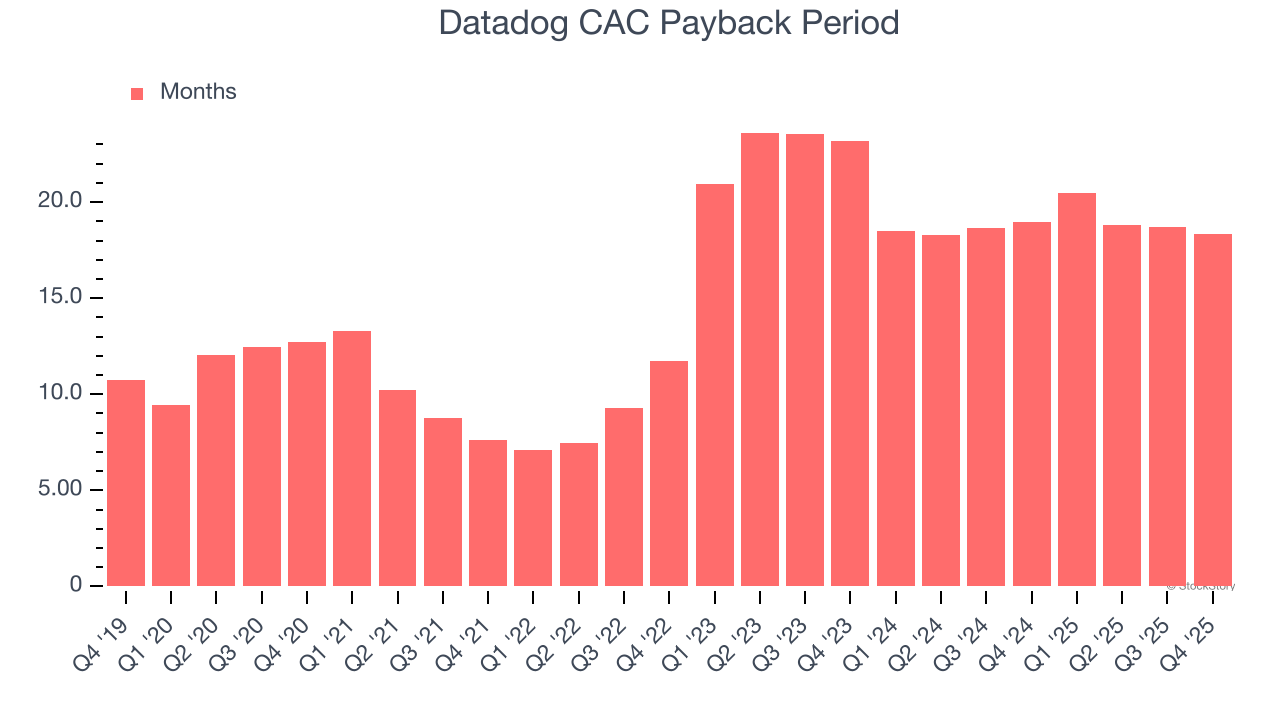

3. Customer Acquisition Costs Are Recovered in Record Time

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Datadog is extremely efficient at acquiring new customers, and its CAC payback period checked in at 18.3 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Datadog more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

Final Judgment

These are just a few reasons why Datadog is a cream-of-the-crop software company. After the recent drawdown, the stock trades at 11× forward price-to-sales (or $124.16 per share). Is now a good time to buy? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Datadog

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.