Even during a down period for the markets, Triumph Financial has gone against the grain, climbing to $55.68. Its shares have yielded a 11.3% return over the last six months, beating the S&P 500 by 14.4%. This run-up might have investors contemplating their next move.

Is there a buying opportunity in Triumph Financial, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Triumph Financial Will Underperform?

We’re glad investors have benefited from the price increase, but we're sitting this one out for now. Here are three reasons we avoid TFIN and a stock we'd rather own.

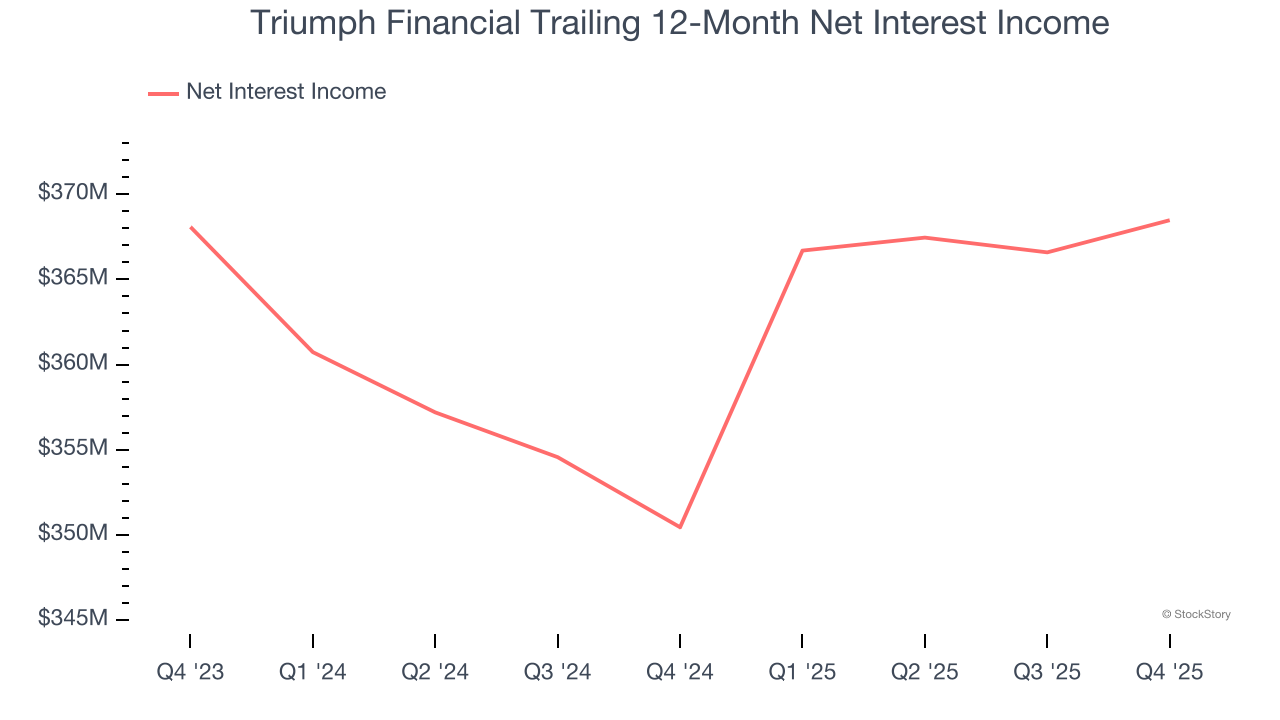

1. Net Interest Income Points to Soft Demand

Our experience and research show the market cares primarily about a bank’s net interest income growth as one-time fees are considered a lower-quality and non-recurring revenue source.

Triumph Financial’s net interest income has grown at a 5.3% annualized rate over the last five years, much worse than the broader banking industry and in line with its total revenue. Its growth was driven by an increase in its net interest margin, which represents how much a bank earns in relation to its outstanding loans, as its loan book shrank throughout that period.

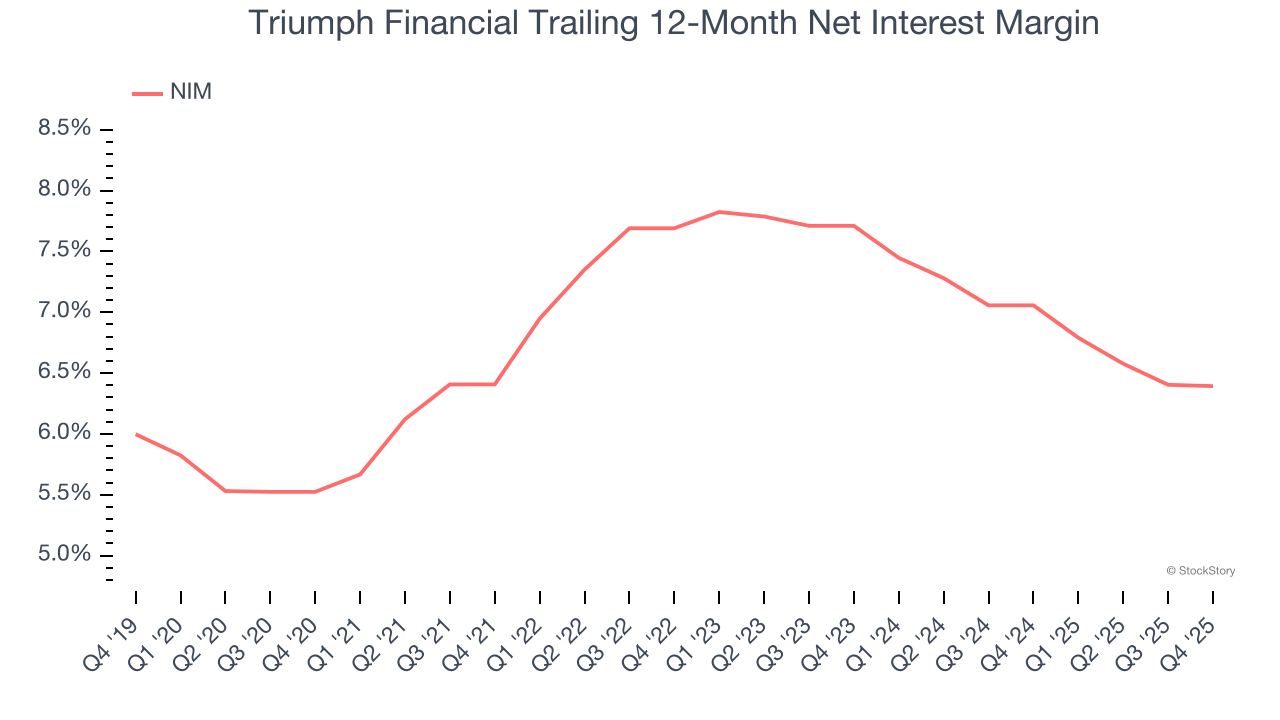

2. Net Interest Margin Dropping

Net interest margin (NIM) represents how much a bank earns in relation to its outstanding loans. It's one of the most important metrics to track because it shows how a bank's loans are performing and whether it has the ability to command higher premiums for its services.

Over the past two years, Triumph Financial’s net interest margin averaged 6.7%. However, its margin contracted from 7.7% to 6.4% over that period.

This decline was a headwind for its net interest income. While prevailing rates are a major determinant of net interest margin changes over time, the decline could mean Triumph Financial either faced competition for loans and deposits or experienced a negative mix shift in its balance sheet composition.

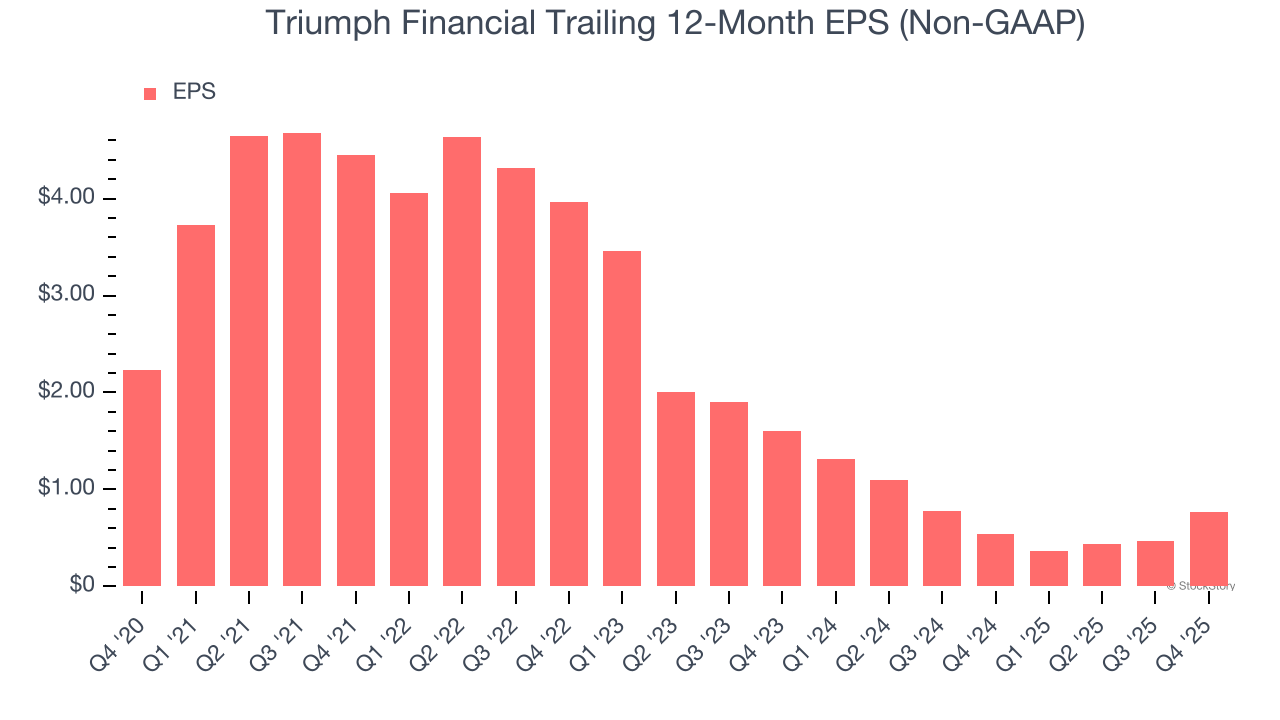

3. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Triumph Financial, its EPS declined by 19.1% annually over the last five years while its revenue grew by 5.9%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Triumph Financial doesn’t pass our quality test. With its shares topping the market in recent months, the stock trades at 1.5× forward P/B (or $55.68 per share). This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere. We’d suggest looking at one of our top digital advertising picks.

Stocks We Like More Than Triumph Financial

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.