Mercury General’s 15.3% return over the past six months has outpaced the S&P 500 by 10%, and its stock price has climbed to $92.03 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Mercury General, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Mercury General Not Exciting?

We’re glad investors have benefited from the price increase, but we don't have much confidence in Mercury General. Here are three reasons you should be careful with MCY and a stock we'd rather own.

1. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Mercury General’s revenue to rise by 1.3%, a deceleration versus its 13.7% annualized growth for the past two years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

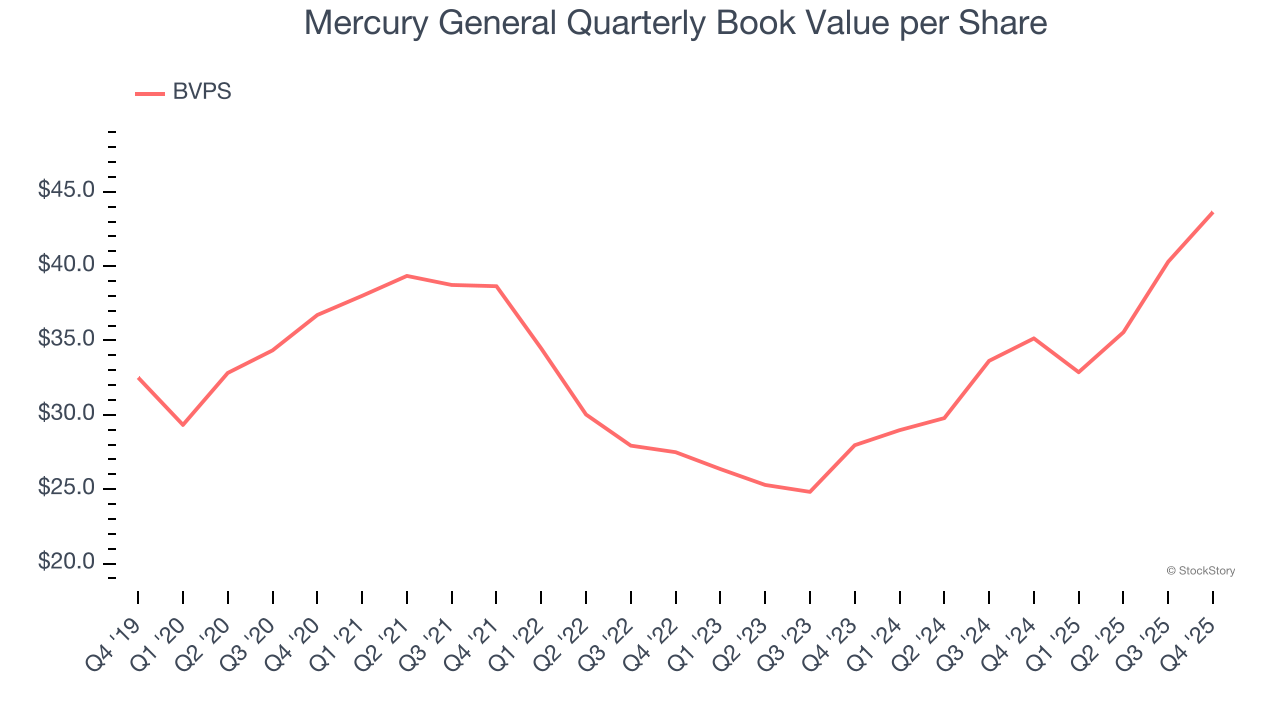

2. Growing BVPS Reflects Strong Asset Base

Book value per share (BVPS) serves as a key indicator of an insurer’s financial stability, reflecting a company’s ability to maintain adequate capital levels and meet its long-term obligations to policyholders.

Although Mercury General’s BVPS increased by a meager 3.5% annually over the last five years, the good news is that its growth has recently accelerated as BVPS grew at an exceptional 24.9% annual clip over the past two years (from $27.96 to $43.64 per share).

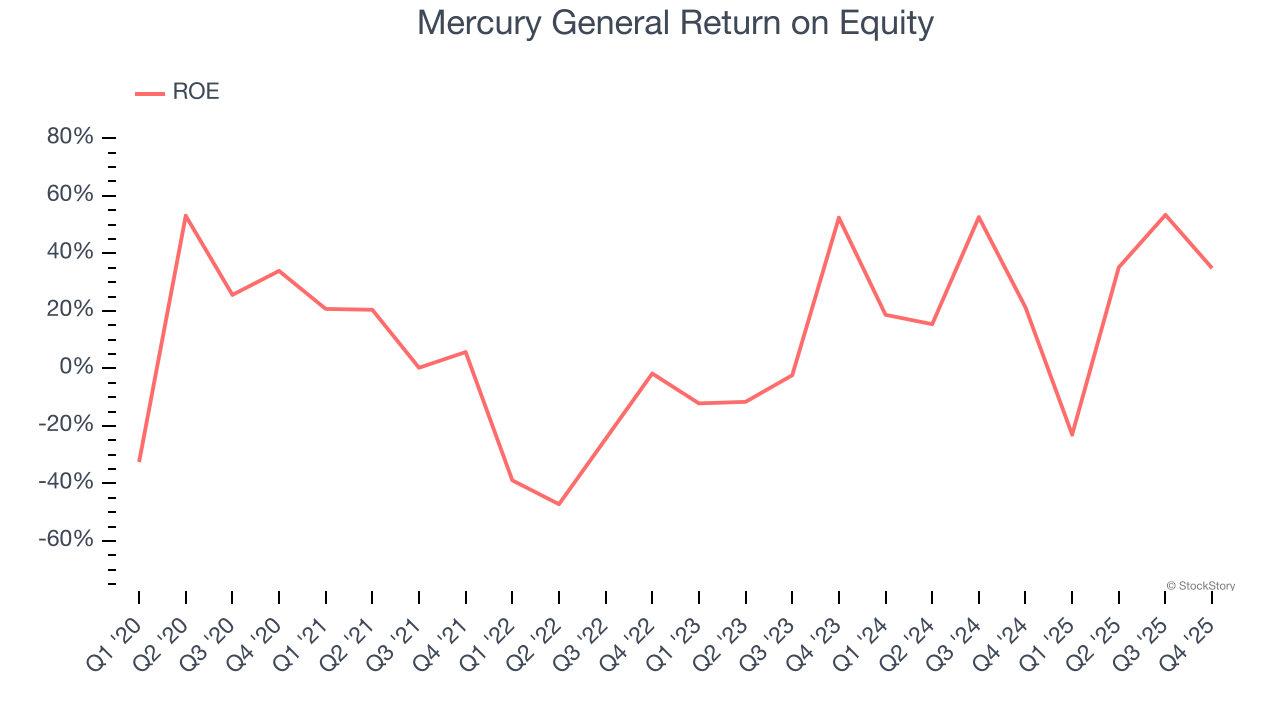

3. Previous Growth Initiatives Haven’t Impressed

Return on equity, or ROE, represents the ultimate measure of an insurer's effectiveness, quantifying how well it transforms shareholder investments into profits. Over the long term, insurance companies with robust ROE metrics typically deliver superior shareholder returns through a balanced approach to capital management.

Over the last five years, Mercury General has averaged an ROE of 8.5%, uninspiring for a company operating in a sector where the average shakes out around 12.5%.

Final Judgment

Mercury General isn’t a terrible business, but it doesn’t pass our bar. With its shares beating the market recently, the stock trades at 1.8× forward P/B (or $92.03 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're fairly confident there are better investments elsewhere. We’d recommend looking at one of our top digital advertising picks.

Stocks We Like More Than Mercury General

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.