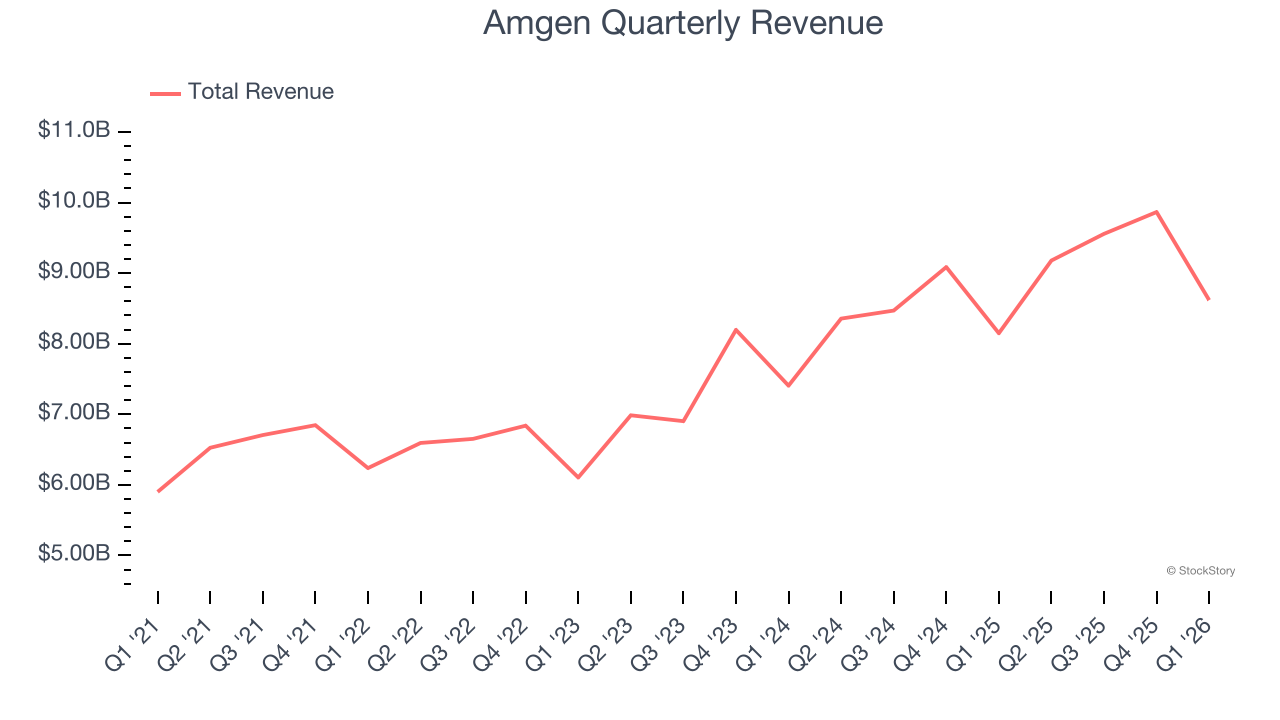

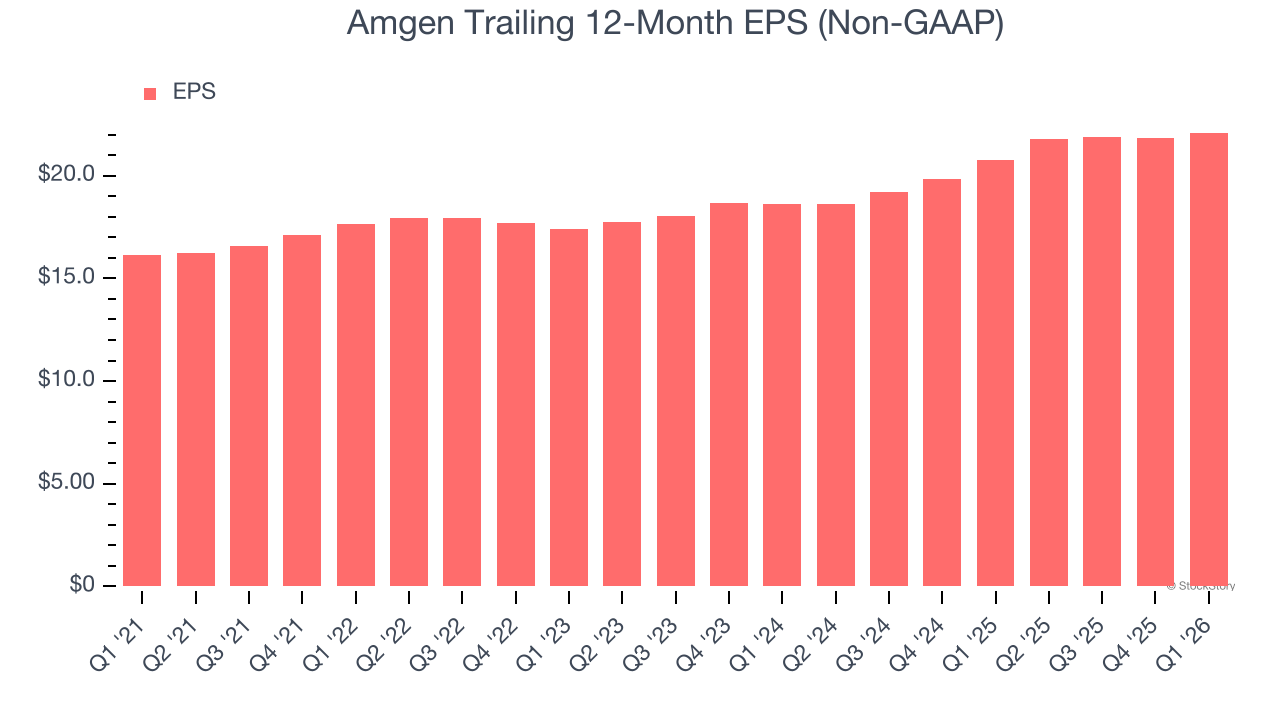

Biotech company Amgen (NASDAQ: AMGN) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 5.8% year on year to $8.62 billion. The company expects the full year’s revenue to be around $37.8 billion, close to analysts’ estimates. Its non-GAAP profit of $5.15 per share was 8% above analysts’ consensus estimates.

Is now the time to buy Amgen? Find out by accessing our full research report, it’s free.

Amgen (AMGN) Q1 CY2026 Highlights:

- Revenue: $8.62 billion vs analyst estimates of $8.5 billion (5.8% year-on-year growth, 1.4% beat)

- Adjusted EPS: $5.15 vs analyst estimates of $4.77 (8% beat)

- Adjusted Operating Income: $3.72 billion vs analyst estimates of $3.62 billion (43.2% margin, 2.8% beat)

- The company slightly lifted its revenue guidance for the full year to $37.8 billion at the midpoint from $37.7 billion

- Management slightly raised its full-year Adjusted EPS guidance to $22.40 at the midpoint

- Operating Margin: 30.9%, up from 14.5% in the same quarter last year

- Free Cash Flow Margin: 17.4%, up from 12% in the same quarter last year

- Market Capitalization: $182.4 billion

"Our first quarter results demonstrate the strength of our business, with 16 brands achieving double-digit growth, enabling us to grow through expected patent expirations and increased competition. With a new wave of molecules progressing in Phase 3 clinical development, we're confident in our ability to deliver attractive long-term growth," said Robert A. Bradway, chairman and chief executive officer.

Company Overview

Founded in 1980 during the early days of the biotechnology revolution, Amgen (NASDAQ: AMGN) is a biotechnology company that discovers, develops, and manufactures innovative medicines to treat serious illnesses like cancer, osteoporosis, and autoimmune diseases.

Revenue Growth

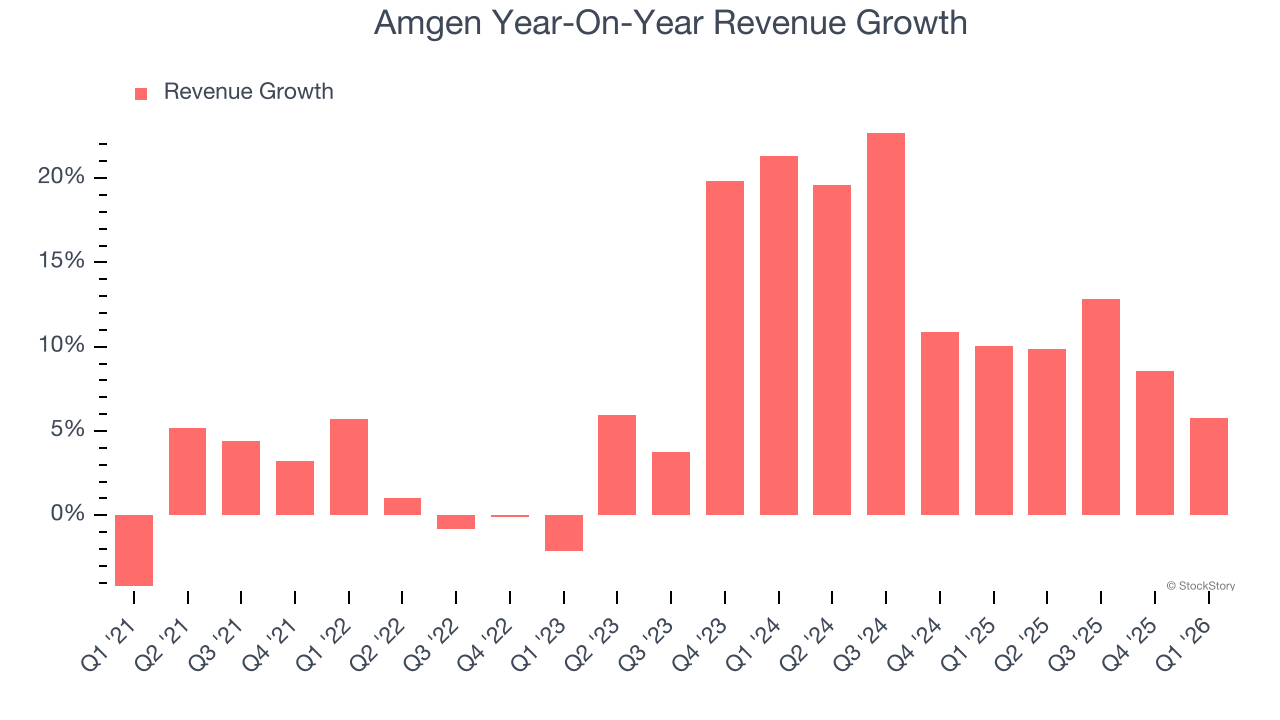

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, Amgen’s 8.1% annualized revenue growth over the last five years was decent. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Amgen’s annualized revenue growth of 12.3% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

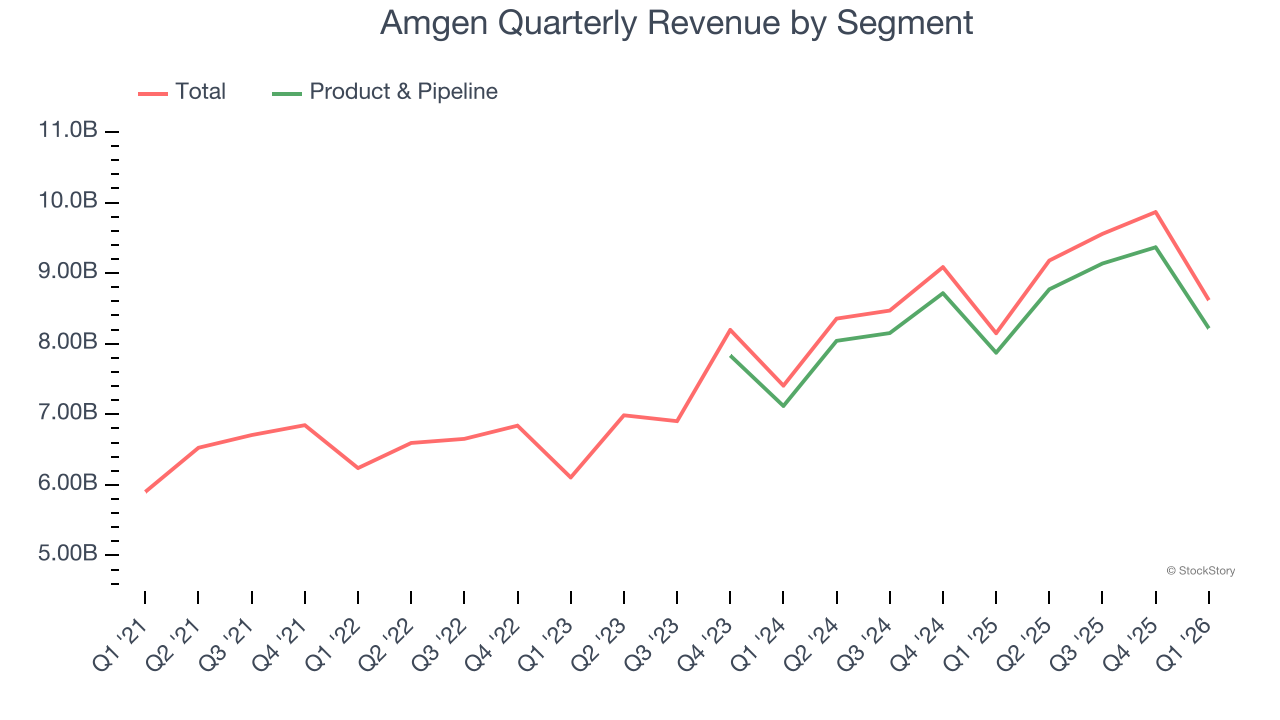

We can dig further into the company’s revenue dynamics by analyzing its most important segment, Product & Pipeline. Over the last two years, Amgen’s Product & Pipeline revenue averaged 9.2% year-on-year growth. This segment has lagged the company’s overall sales.

This quarter, Amgen reported year-on-year revenue growth of 5.8%, and its $8.62 billion of revenue exceeded Wall Street’s estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to grow 1.8% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Adjusted Operating Margin

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

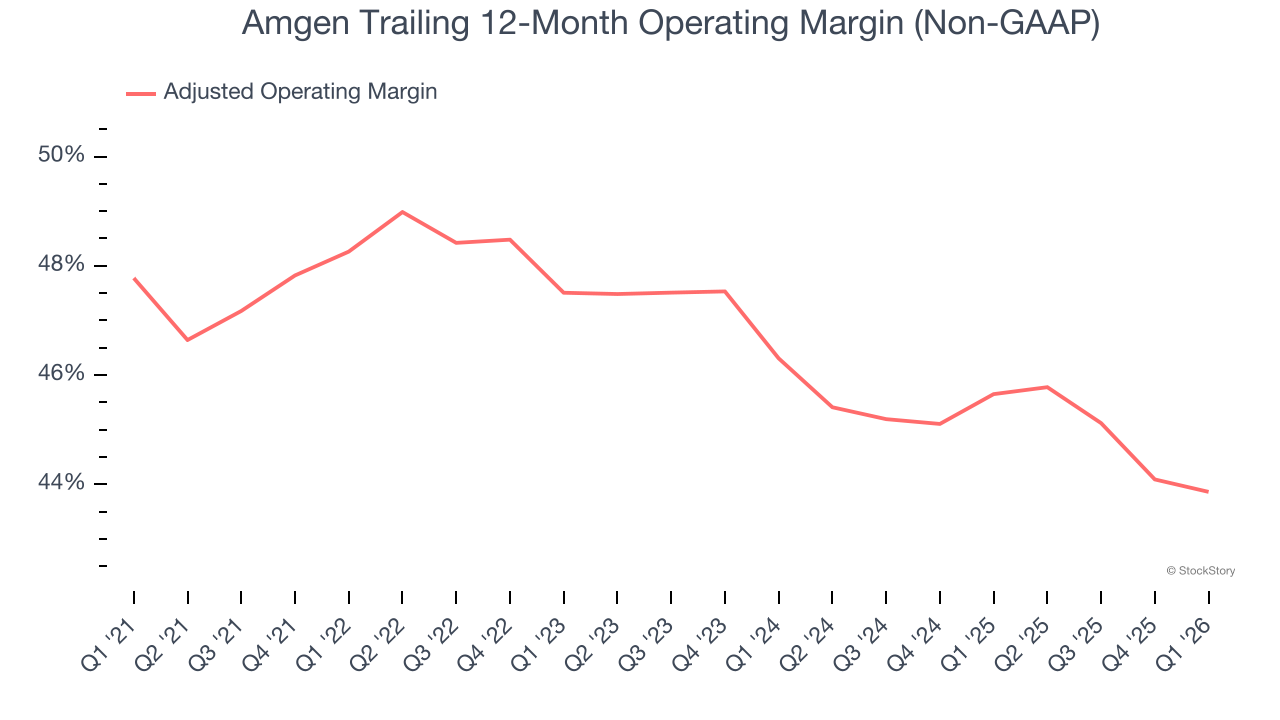

Amgen has been a well-oiled machine over the last five years. It demonstrated elite profitability for a healthcare business, boasting an average adjusted operating margin of 46.1%.

Looking at the trend in its profitability, Amgen’s adjusted operating margin decreased by 4.4 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 2.4 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q1, Amgen generated an adjusted operating margin profit margin of 43.2%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Amgen’s decent 6.5% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q1, Amgen reported adjusted EPS of $5.15, up from $4.90 in the same quarter last year. This print beat analysts’ estimates by 8%. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Amgen’s Q1 Results

It was good to see Amgen beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. Overall, this print had some key positives. The market seemed to be hoping for more, and the stock traded down 2.5% to $338.00 immediately after reporting.

So do we think Amgen is an attractive buy at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).