As the craze of earnings season draws to a close, here’s a look back at some of the most exciting (and some less so) results from Q1. Today, we are looking at drug development inputs & services stocks, starting with Medpace (NASDAQ: MEDP).

Companies specializing in drug development inputs and services play a crucial role in the pharmaceutical and biotechnology value chain. Essential support for drug discovery, preclinical testing, and manufacturing means stable demand, as pharmaceutical companies often outsource non-core functions with medium to long-term contracts. However, the business model faces high capital requirements, customer concentration, and vulnerability to shifts in biopharma R&D budgets or regulatory frameworks. Looking ahead, the industry will likely enjoy tailwinds such as increasing investment in biologics, cell and gene therapies, and advancements in precision medicine, which drive demand for sophisticated tools and services. There is a growing trend of outsourcing in drug development for nimbleness and cost efficiency, which benefits the industry. On the flip side, potential headwinds include pricing pressures as efforts to contain healthcare costs are always top of mind. An evolving regulatory backdrop could also slow innovation or client activity.

The 8 drug development inputs & services stocks we track reported a satisfactory Q1. As a group, revenues beat analysts’ consensus estimates by 1.6% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady as they are up 1.3% on average since the latest earnings results.

Medpace (NASDAQ: MEDP)

Founded in 1992 as a scientifically-driven alternative to traditional contract research organizations, Medpace (NASDAQ: MEDP) provides outsourced clinical trial management and research services to help pharmaceutical, biotechnology, and medical device companies develop new treatments.

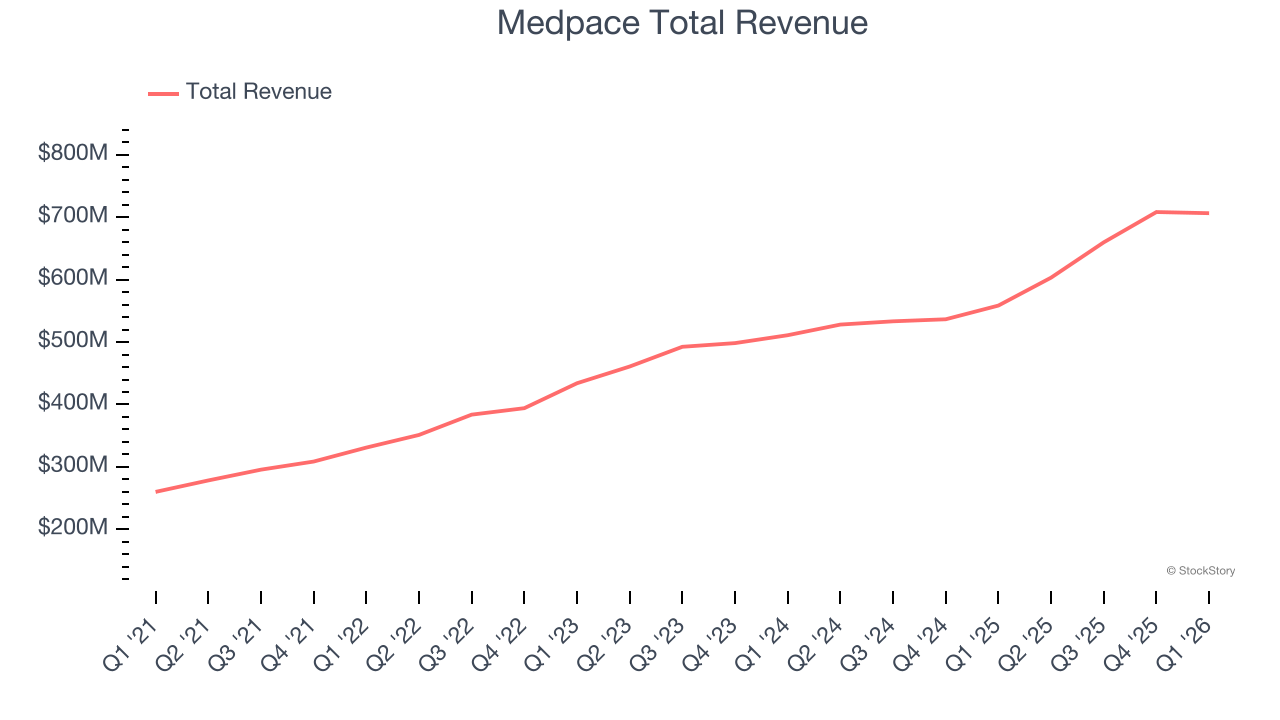

Medpace reported revenues of $706.6 million, up 26.5% year on year. This print exceeded analysts’ expectations by 1.5%. Overall, it was a satisfactory quarter for the company with a beat of analysts’ EPS estimates but full-year EPS guidance in line with analysts’ estimates.

Medpace achieved the fastest revenue growth and highest full-year guidance raise of the whole group. Even though it had a relatively good quarter, the market seems discontent with the results. The stock is down 16.6% since reporting and currently trades at $413.94.

Is now the time to buy Medpace? Access our full analysis of the earnings results here, it’s free.

Best Q1: West Pharmaceutical Services (NYSE: WST)

Founded in 1923 and serving as a critical link in the pharmaceutical supply chain, West Pharmaceutical Services (NYSE: WST) manufactures specialized packaging, containment systems, and delivery devices for injectable drugs and healthcare products.

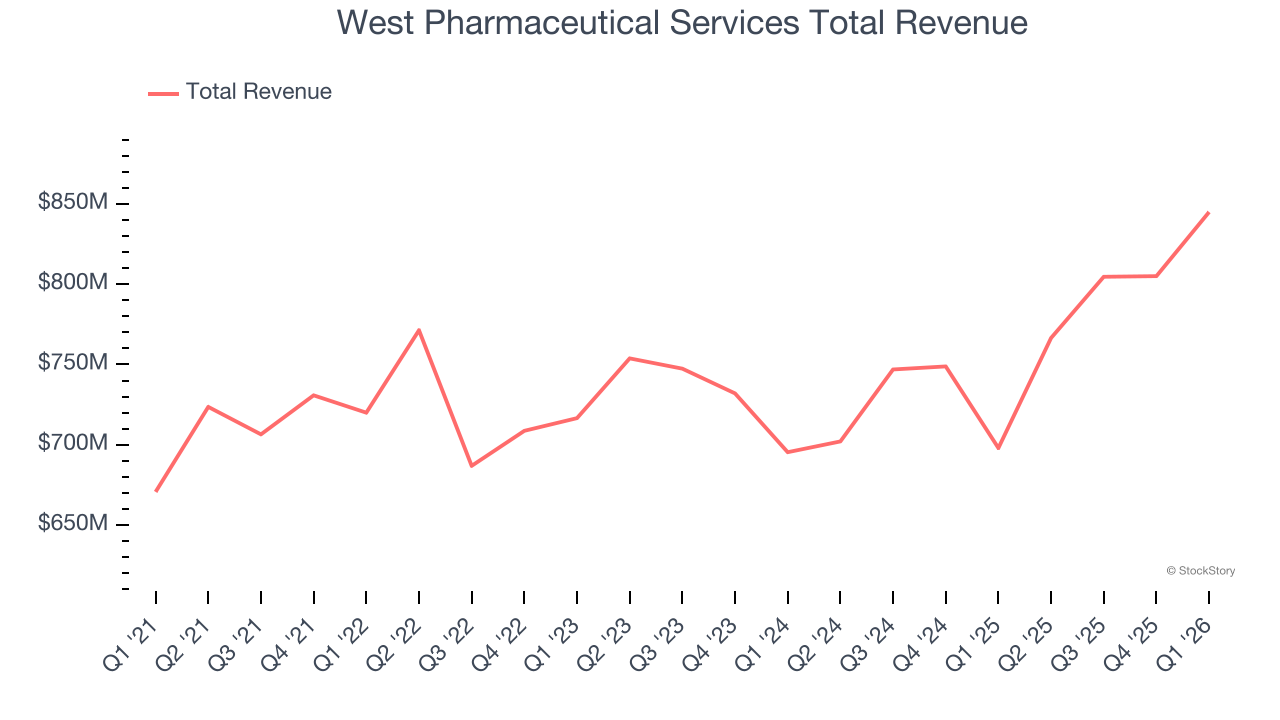

West Pharmaceutical Services reported revenues of $844.9 million, up 21% year on year, outperforming analysts’ expectations by 8.4%. The business had a stunning quarter with a beat of analysts’ EPS and revenue estimates.

West Pharmaceutical Services pulled off the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 16.6% since reporting. It currently trades at $320.00.

Is now the time to buy West Pharmaceutical Services? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Azenta (NASDAQ: AZTA)

Serving as the guardian of some of medicine's most valuable materials, Azenta (NASDAQ: AZTA) provides biological sample management, storage, and genomic services that help pharmaceutical and biotechnology companies preserve and analyze critical research materials.

Azenta reported revenues of $144.8 million, up 1% year on year, falling short of analysts’ expectations by 2.5%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue and EPS estimates.

Azenta delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 26.6% since the results and currently trades at $18.06.

Read our full analysis of Azenta’s results here.

Repligen (NASDAQ: RGEN)

With over 13 strategic acquisitions since 2012 to build its comprehensive bioprocessing portfolio, Repligen (NASDAQ: RGEN) develops and manufactures specialized technologies that improve the efficiency and flexibility of biological drug manufacturing processes.

Repligen reported revenues of $194.3 million, up 14.8% year on year. This number topped analysts’ expectations by 1.3%. It was a strong quarter as it also produced a beat of analysts’ EPS and full-year EPS guidance estimates.

Repligen had the weakest full-year guidance update among its peers. The stock is flat since reporting and currently trades at $118.50.

Read our full, actionable report on Repligen here, it’s free.

Fortrea (NASDAQ: FTRE)

Spun off from Labcorp in 2023 to focus exclusively on clinical research services, Fortrea (NASDAQ: FTRE) is a contract research organization that helps pharmaceutical, biotech, and medical device companies develop and bring their products to market through clinical trials and support services.

Fortrea reported revenues of $636.5 million, down 2.3% year on year. This result beat analysts’ expectations by 1.4%. Overall, it was a strong quarter as it also logged a beat of analysts’ EPS and revenue estimates.

Fortrea had the slowest revenue growth among its peers. The stock is up 22.4% since reporting and currently trades at $14.99.

Read our full, actionable report on Fortrea here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.