As the craze of earnings season draws to a close, here’s a look back at some of the most exciting (and some less so) results from Q1. Today, we are looking at consumer discretionary - specialized consumer services stocks, starting with Pool (NASDAQ: POOL).

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare. Some consumer discretionary companies don’t fall neatly into a category because their products or services are unique. Although their offerings may be niche, these companies have often found more efficient or technology-enabled ways of doing or selling something that has existed for a while. Technology can be a double-edged sword, though, as it may lower the barriers to entry for new competitors and allow them to do serve customers better.

The 11 consumer discretionary - specialized consumer services stocks we track reported a mixed Q1. As a group, revenues beat analysts’ consensus estimates by 1.4% while next quarter’s revenue guidance was in line.

While some consumer discretionary - specialized consumer services stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 4.2% since the latest earnings results.

Pool (NASDAQ: POOL)

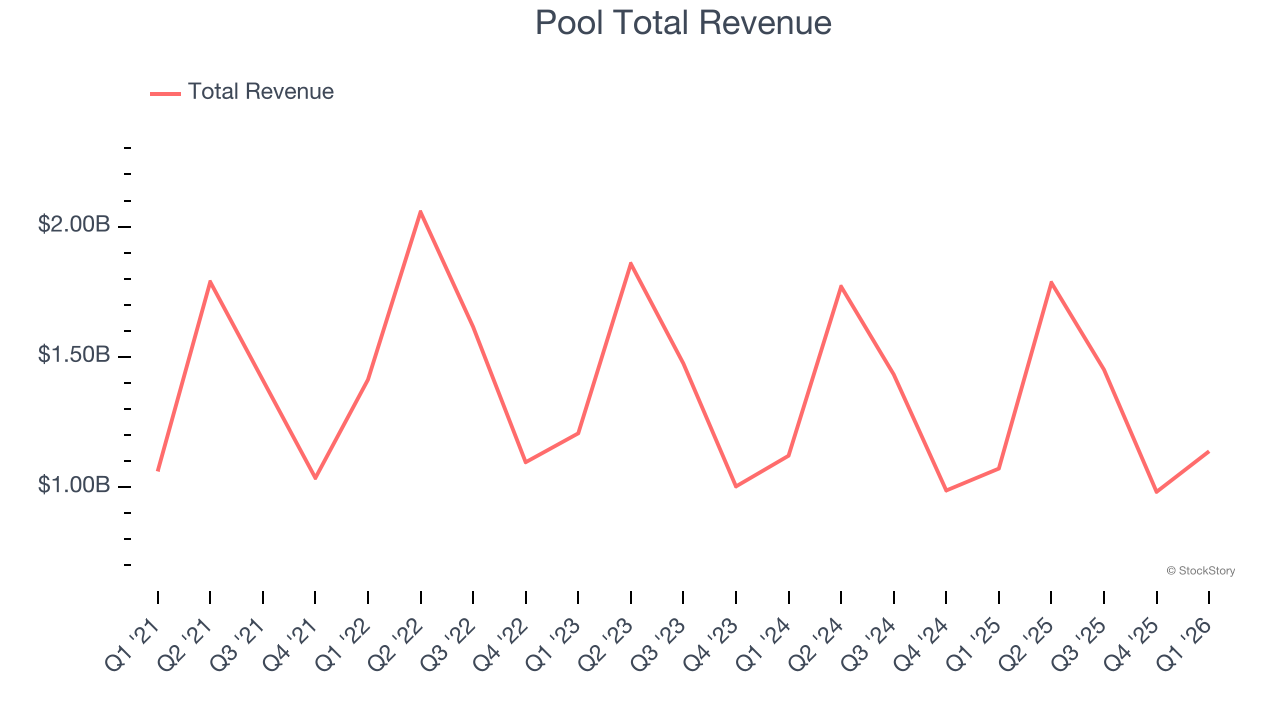

Founded in 1993 and headquartered in Louisiana, Pool (NASDAQ: POOL) is one of the largest wholesale distributors of swimming pool supplies, equipment, and related leisure products.

Pool reported revenues of $1.14 billion, up 6.2% year on year. This print exceeded analysts’ expectations by 3.8%. Overall, it was a satisfactory quarter for the company with an impressive beat of analysts’ revenue estimates but full-year EPS guidance meeting analysts’ expectations.

“We are off to a solid start in 2026, with net sales up 6% and operating income growing 7% year-over-year. Maintenance demand remained resilient, and we saw continued, though still gradual, recovery in discretionary categories. Gross margin reflected the typical first quarter seasonal mix, with strong equipment and customer early buy sales partially offset by our pricing and supply chain initiatives. Our greenfield investments are contributing to growth, and we are beginning to see operating expense leverage as those locations mature. We remain confident in our strategy and our ability to drive profitable growth,” said Peter D. Arvan, president and CEO.

The stock is down 24.4% since reporting and currently trades at $177.17.

Is now the time to buy Pool? Access our full analysis of the earnings results here, it’s free.

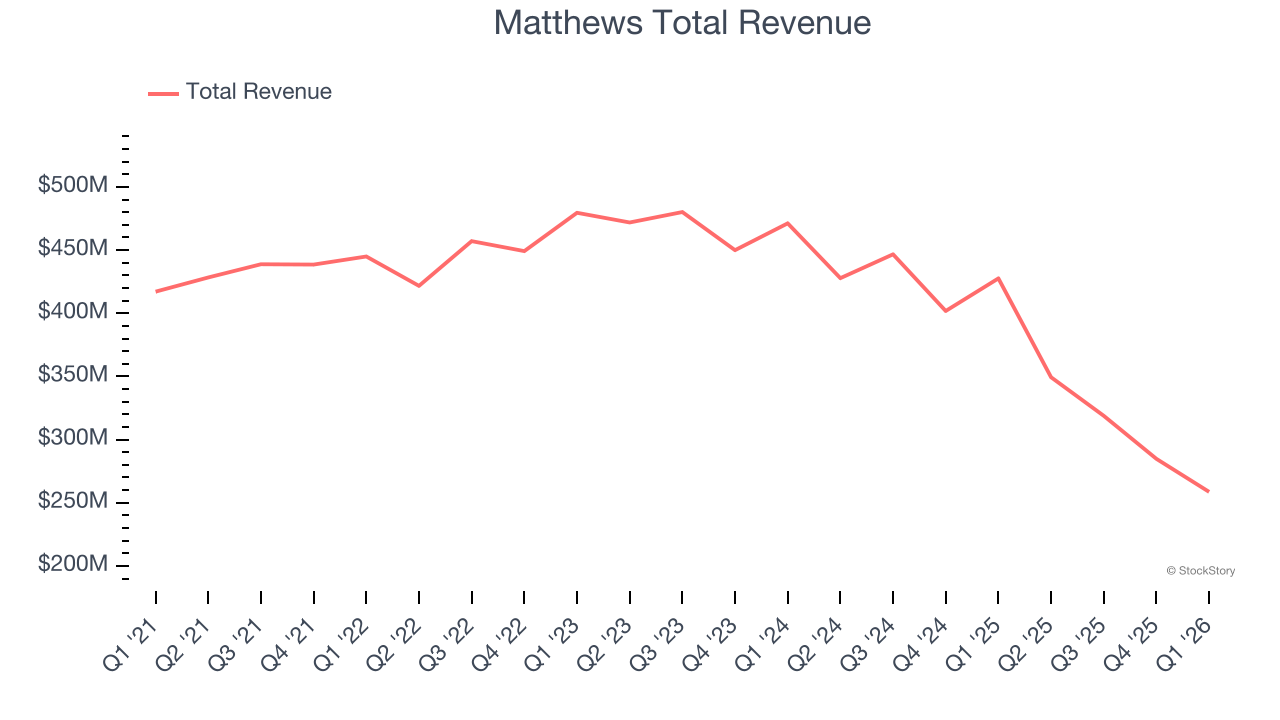

Best Q1: Matthews (NASDAQ: MATW)

Originally a death care company, Matthews International (NASDAQ: MATW) is a diversified company offering ceremonial services, brand solutions and industrial technologies.

Matthews reported revenues of $258.6 million, down 39.5% year on year, outperforming analysts’ expectations by 2%. The business had a very strong quarter with a beat of analysts’ EPS and adjusted operating income estimates.

Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 2.6% since reporting. It currently trades at $27.79.

Is now the time to buy Matthews? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: WeightWatchers (NASDAQ: WW)

Known by many for its old cable television commercials, WeightWatchers (NASDAQ: WW) is a wellness company offering a range of products and services promoting weight loss and healthy habits.

WeightWatchers reported revenues of $168.3 million, down 9.8% year on year, exceeding analysts’ expectations by 6.1%. Still, it was a slower quarter as it posted a significant miss of analysts’ EBITDA estimates and a significant miss of analysts’ EPS estimates.

WeightWatchers delivered the biggest analyst estimates beat but had the weakest full-year guidance update in the group. As expected, the stock is down 17.3% since the results and currently trades at $9.75.

Read our full analysis of WeightWatchers’s results here.

Frontdoor (NASDAQ: FTDR)

Established in 2018 as a spin-off from ServiceMaster Global Holdings, Frontdoor (NASDAQ: FTDR) is a provider of home warranty and service plans.

Frontdoor reported revenues of $451 million, up 5.9% year on year. This print surpassed analysts’ expectations by 1.9%. Zooming out, it was a mixed quarter as it also recorded a beat of analysts’ EPS estimates but EBITDA guidance for next quarter slightly missing analysts’ expectations.

The stock is up 3.4% since reporting and currently trades at $62.64.

Read our full, actionable report on Frontdoor here, it’s free.

1-800-FLOWERS (NASDAQ: FLWS)

Founded in 1976, 1-800-FLOWERS (NASDAQ: FLWS) is an online retailer of flowers, gifts, and gourmet foods, serving customers globally.

1-800-FLOWERS reported revenues of $293 million, down 11.6% year on year. This result was in line with analysts’ expectations. However, it was a slower quarter as it produced a significant miss of analysts’ EPS estimates and revenue in line with analysts’ estimates.

The stock is up 6.1% since reporting and currently trades at $4.17.

Read our full, actionable report on 1-800-FLOWERS here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.