Let’s dig into the relative performance of Meritage Homes (NYSE: MTH) and its peers as we unravel the now-completed Q1 home builders earnings season.

Traditionally, homebuilders have built competitive advantages with economies of scale that lead to advantaged purchasing and brand recognition among consumers. Aesthetic trends have always been important in the space, but more recently, energy efficiency and conservation are driving innovation. However, these companies are still at the whim of the macro, specifically interest rates that heavily impact new and existing home sales. In fact, homebuilders are one of the most cyclical subsectors within industrials.

The 11 home builders stocks we track reported a slower Q1. As a group, revenues missed analysts’ consensus estimates by 1.7%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 10.1% since the latest earnings results.

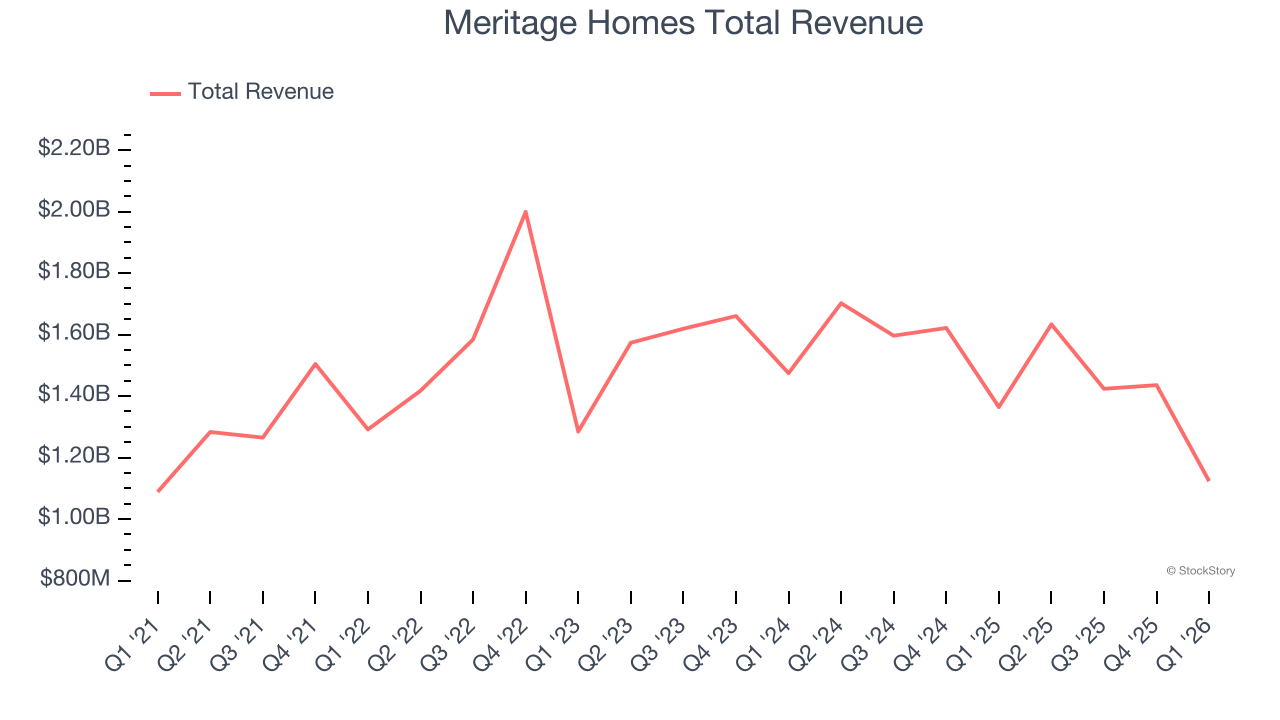

Meritage Homes (NYSE: MTH)

Originally founded in 1985 in Arizona as Monterey Homes, Meritage Homes (NYSE: MTH) is a homebuilder specializing in designing and constructing energy-efficient and single-family homes in the US.

Meritage Homes reported revenues of $1.12 billion, down 17.7% year on year. This print fell short of analysts’ expectations by 3.8%. Overall, it was a disappointing quarter for the company with a significant miss of analysts’ revenue and EBITDA estimates.

"With the spring selling season commencing this quarter, we experienced some improved demand, achieving an absorption rate of 3.6 net sales per month and sales orders of 3,664 homes. However, these results were below our expectations as 2026 began with a severe winter storm in January and then transitioned into military operations in Iran midway through the quarter, which negatively impacted consumer sentiment and mortgage rates," said Steven J. Hilton, executive chairman of Meritage Homes.

The stock is down 10% since reporting and currently trades at $61.84.

Read our full report on Meritage Homes here, it’s free.

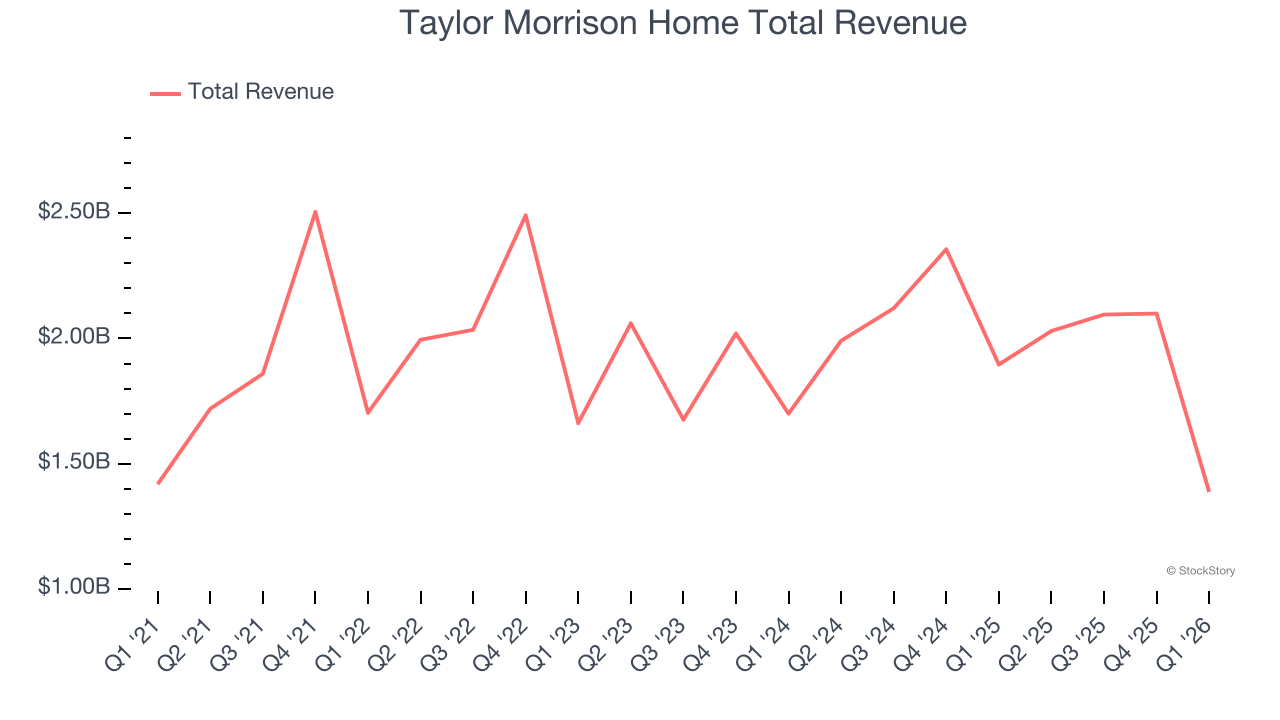

Best Q1: Taylor Morrison Home (NYSE: TMHC)

Named “America’s Most Trusted Home Builder” in 2019, Taylor Morrison Home (NYSE: TMHC) builds single family homes and communities across the United States.

Taylor Morrison Home reported revenues of $1.39 billion, down 26.8% year on year, outperforming analysts’ expectations by 4.1%. The business had an incredible quarter with a beat of analysts’ EPS and adjusted operating income estimates.

Taylor Morrison Home pulled off the biggest analyst estimates beat among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 8.1% since reporting. It currently trades at $56.95.

Is now the time to buy Taylor Morrison Home? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: NVR (NYSE: NVR)

Known for its unique land acquisition strategy, NVR (NYSE: NVR) is a respected homebuilder and mortgage company in the United States.

NVR reported revenues of $1.88 billion, down 21.7% year on year, falling short of analysts’ expectations by 7.8%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue and adjusted operating income estimates.

NVR delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 18% since the results and currently trades at $5,686.

Read our full analysis of NVR’s results here.

TopBuild (NYSE: BLD)

Established in 2015 following a spinoff from Masco Corporation, TopBuild (NYSE: BLD) is a distributor and installer of insulation and other building products.

TopBuild reported revenues of $1.45 billion, up 17.2% year on year. This result beat analysts’ expectations by 2.5%. It was a strong quarter as it also produced a solid beat of analysts’ revenue and adjusted operating income estimates.

TopBuild delivered the fastest revenue growth among its peers. The stock is down 3.9% since reporting and currently trades at $413.64.

Read our full, actionable report on TopBuild here, it’s free.

Installed Building Products (NYSE: IBP)

Founded in 1977, Installed Building Products (NYSE: IBP) is a company specializing in the installation of insulation, waterproofing, and other complementary building products for residential and commercial construction.

Installed Building Products reported revenues of $660.5 million, down 3.5% year on year. This number came in 1.3% below analysts' expectations. It was a softer quarter as it also recorded a significant miss of analysts’ EBITDA estimates and a significant miss of analysts’ EPS estimates.

The stock is down 27.5% since reporting and currently trades at $217.23.

Read our full, actionable report on Installed Building Products here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.