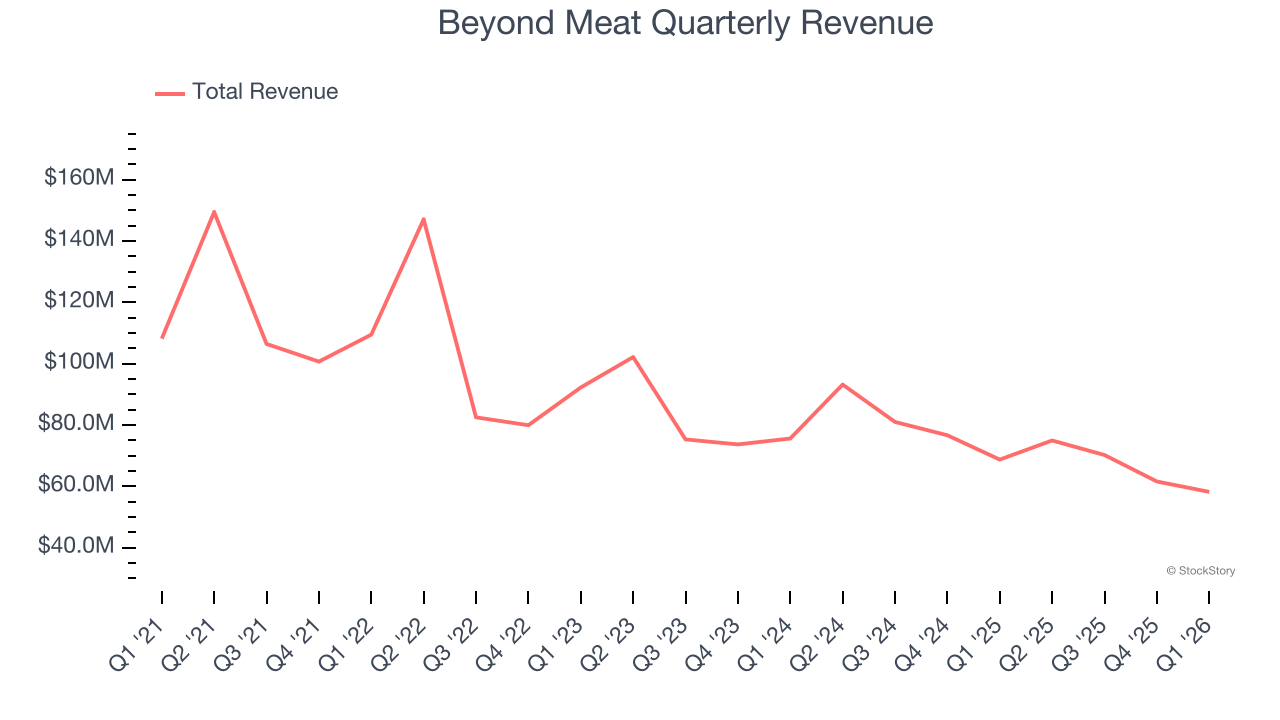

Plant-based protein company Beyond Meat (NASDAQ: BYND) missed Wall Street’s revenue expectations in Q1 CY2026, with sales falling 15.3% year on year to $58.21 million. Next quarter’s revenue guidance of $62.5 million underwhelmed, coming in 4.6% below analysts’ estimates. Its non-GAAP loss of $0.10 per share was in line with analysts’ consensus estimates.

Is now the time to buy Beyond Meat? Find out by accessing our full research report, it’s free.

Beyond Meat (BYND) Q1 CY2026 Highlights:

- Revenue: $58.21 million vs analyst estimates of $59.56 million (15.3% year-on-year decline, 2.3% miss)

- Adjusted EPS: -$0.10 vs analyst estimates of -$0.11 (in line)

- Adjusted EBITDA: -$27.78 million (-47.7% margin, 34.4% year-on-year growth)

- Revenue Guidance for Q2 CY2026 is $62.5 million at the midpoint, below analyst estimates of $65.5 million

- Operating Margin: -70.6%, up from -93.7% in the same quarter last year

- Free Cash Flow was -$7.56 million compared to -$30.63 million in the same quarter last year

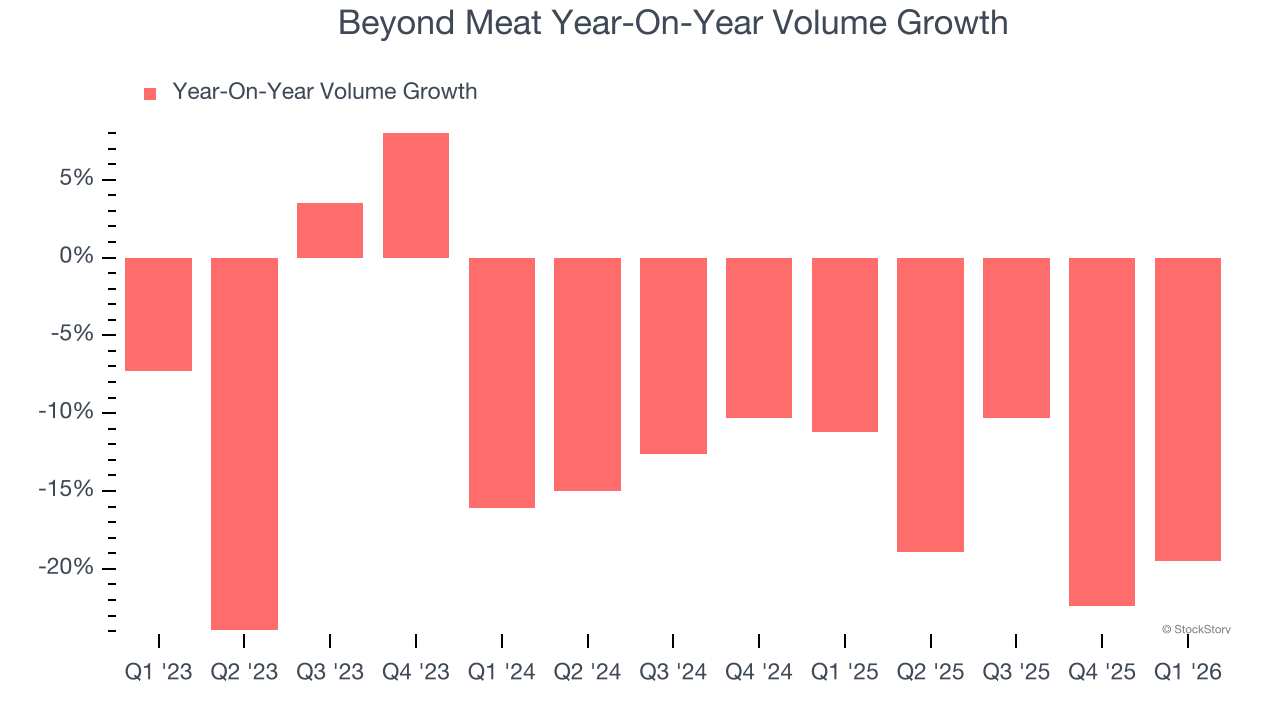

- Sales Volumes fell 19.5% year on year (-11.2% in the same quarter last year)

- Market Capitalization: $425.8 million

Beyond Meat President and CEO Ethan Brown commented, “This quarter marked a decisive broadening of our Company aperture to include the rapidly growing functional food and beverage category. Even as we apply our brand, expertise and technology to adjacent markets, we remain highly focused on the performance of our core business, which we believe will deliver substantial long-term value. To this end, we are pleased to report significant operating expense improvement and our lowest quarterly cash use in over two years.”

Company Overview

A pioneer at the forefront of the plant-based protein revolution, Beyond Meat (NASDAQ: BYND) is a food company specializing in alternatives to traditional meat products.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $265 million in revenue over the past 12 months, Beyond Meat is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Beyond Meat’s demand was weak over the last three years. Its sales fell by 13% annually as consumers bought less of its products.

This quarter, Beyond Meat missed Wall Street’s estimates and reported a rather uninspiring 15.3% year-on-year revenue decline, generating $58.21 million of revenue. Company management is currently guiding for a 16.6% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 7.3% over the next 12 months. it’s tough to feel optimistic about a company facing demand difficulties.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Beyond Meat’s average quarterly sales volumes have shrunk by 15% over the last two years. This decrease isn’t ideal because the quantity demanded for consumer staples products is typically stable.

In Beyond Meat’s Q1 2026, sales volumes dropped 19.5% year on year. This result represents a further deceleration from its historical levels, showing the business is struggling to move its products.

Key Takeaways from Beyond Meat’s Q1 Results

It was encouraging to see Beyond Meat meet analysts’ EPS expectations this quarter. On the other hand, its EBITDA missed and its gross margin fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 9.4% to $0.93 immediately following the results.

The latest quarter from Beyond Meat’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).