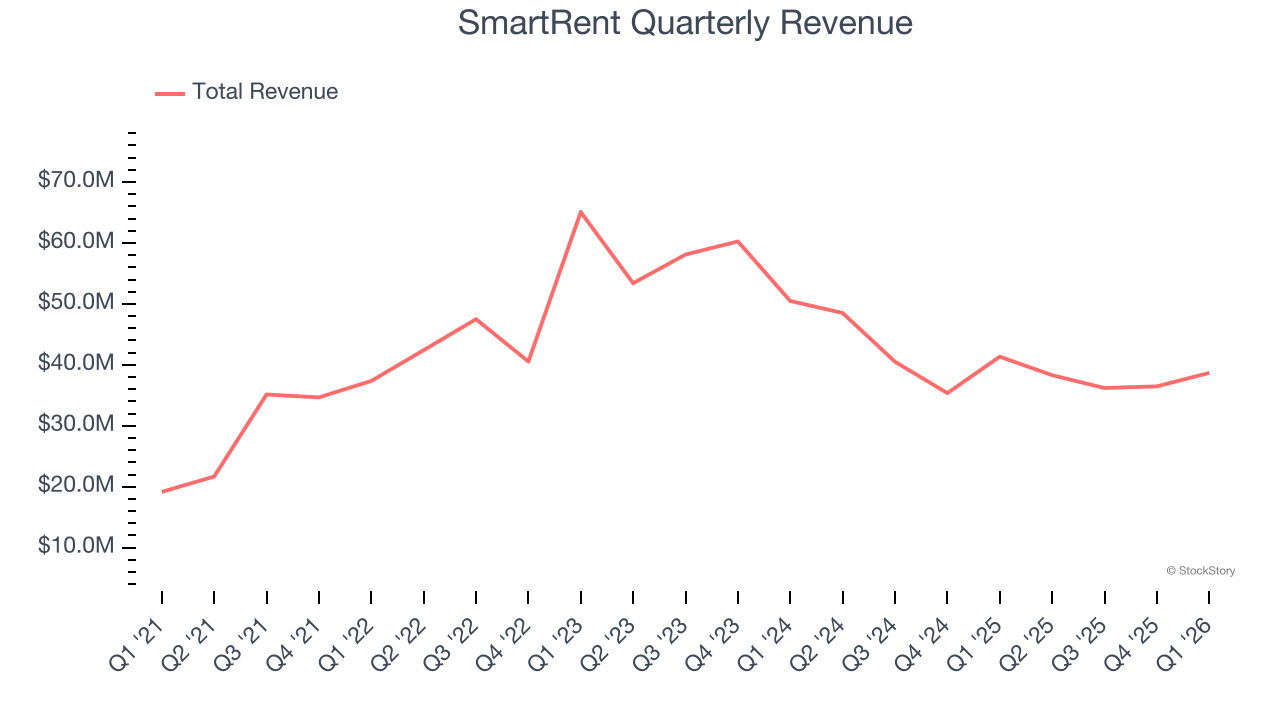

Smart home company SmartRent (NYSE: SMRT) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, but sales fell by 6.4% year on year to $38.68 million. Its GAAP loss of $0.02 per share was in line with analysts’ consensus estimates.

Is now the time to buy SmartRent? Find out by accessing our full research report, it’s free.

SmartRent (SMRT) Q1 CY2026 Highlights:

- Revenue: $38.68 million vs analyst estimates of $38.15 million (6.4% year-on-year decline, 1.4% beat)

- EPS (GAAP): -$0.02 vs analyst estimates of -$0.02 (in line)

- Adjusted EBITDA: $374,000 vs analyst estimates of $875,500 (1% margin, relatively in line)

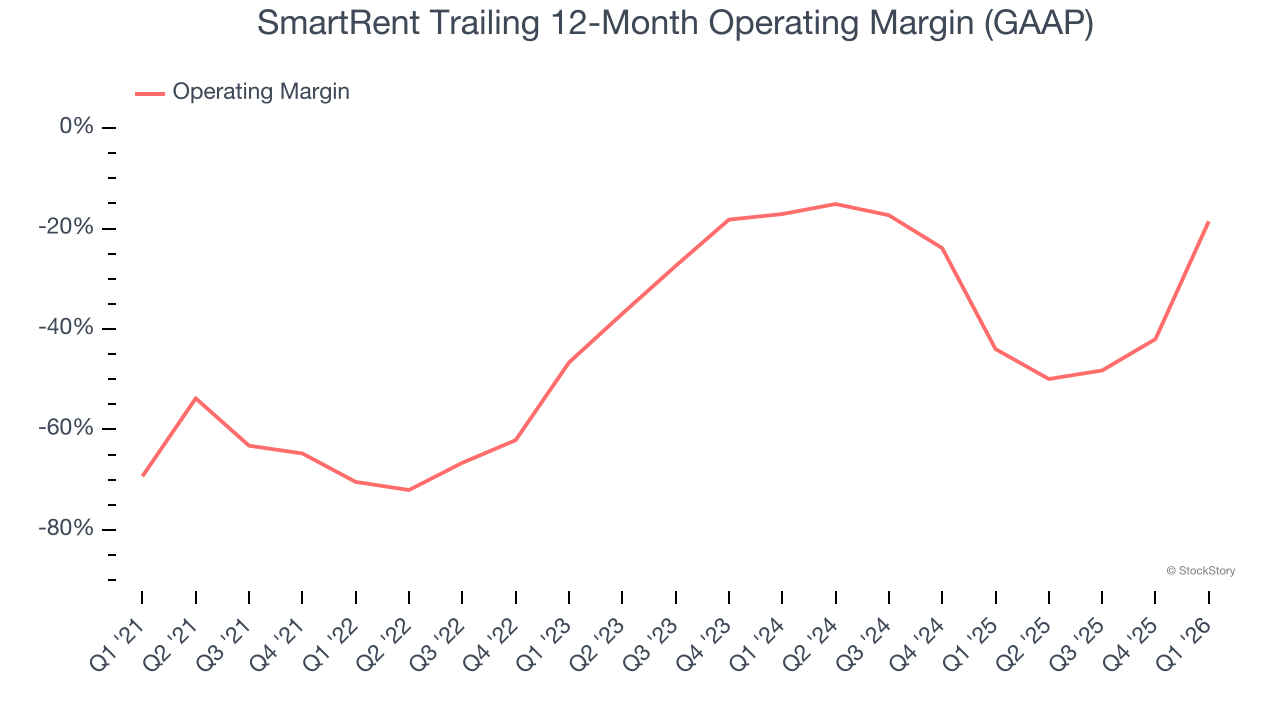

- Operating Margin: -13.2%, up from -99.9% in the same quarter last year

- Free Cash Flow was -$5.63 million compared to -$14.35 million in the same quarter last year

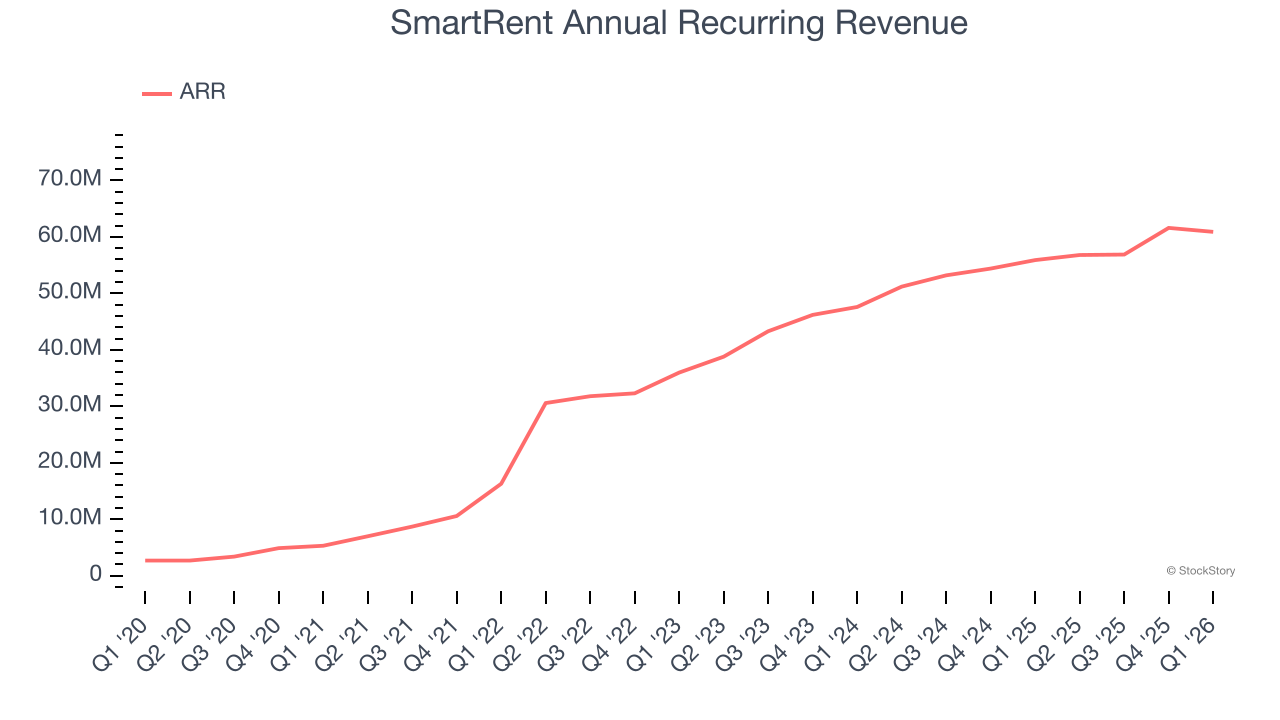

- Annual Recurring Revenue: $60.9 million vs analyst estimates of $62.97 million (8.9% year-on-year growth, miss)

- Market Capitalization: $274.9 million

Company Overview

Founded by an employee at a real estate rental company, SmartRent (NYSE: SMRT) provides smart home devices and software for multifamily residential properties, single-family rental homes, and student housing communities.

Revenue Growth

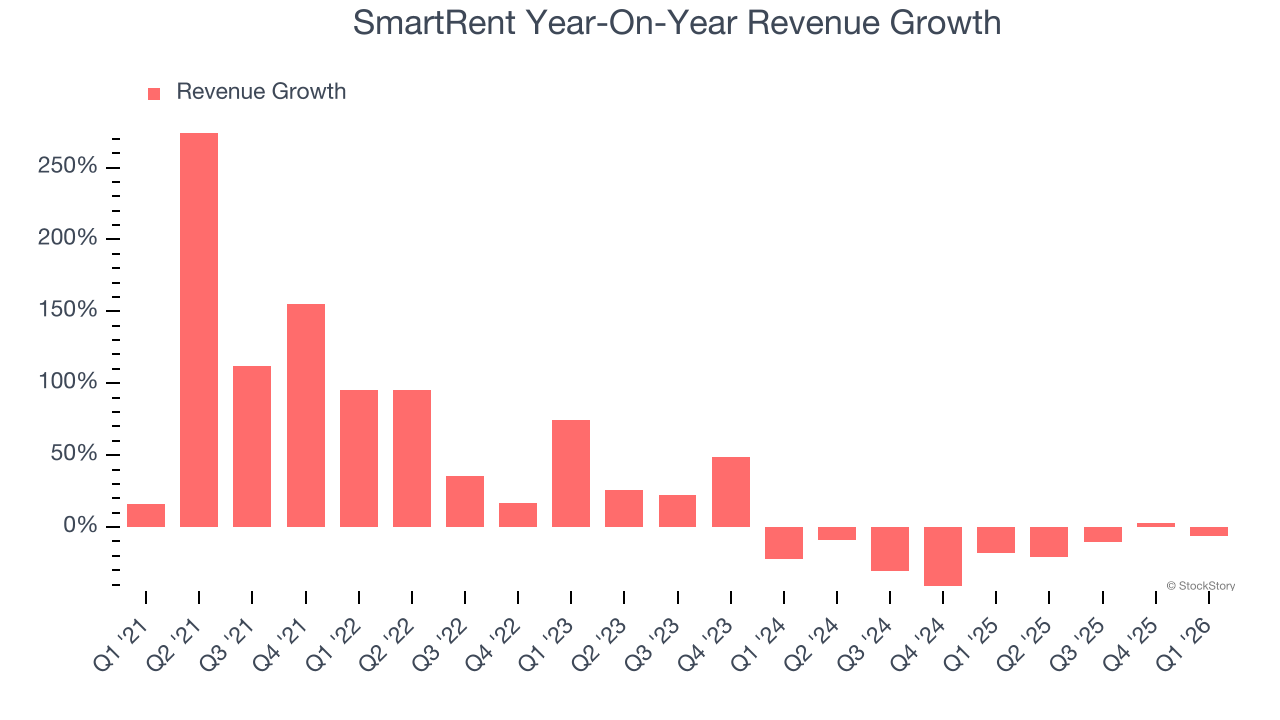

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, SmartRent’s sales grew at an incredible 22.1% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. SmartRent’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 17.9% over the last two years.

We can better understand the company’s sales dynamics by analyzing its annual recurring revenue (ARR), or the predictable, normalized yearly income from subscriptions and contracts. SmartRent’s ARR reached $60.9 million in the latest quarter and averaged 16.3% year-on-year growth over the last two years. Because this number is better than its normal revenue growth, we can see the company’s proportion of recurring revenue from long-term contracts and subscriptions has increased. This implies more stability in its business model and revenue streams.

This quarter, SmartRent’s revenue fell by 6.4% year on year to $38.68 million but beat Wall Street’s estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to grow 13.2% over the next 12 months, an improvement versus the last two years. This projection is noteworthy and suggests its newer products and services will catalyze better top-line performance.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Operating Margin

SmartRent’s high expenses have contributed to an average operating margin of negative 37.2% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, SmartRent’s operating margin rose by 51.9 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

In Q1, SmartRent generated a negative 13.2% operating margin.

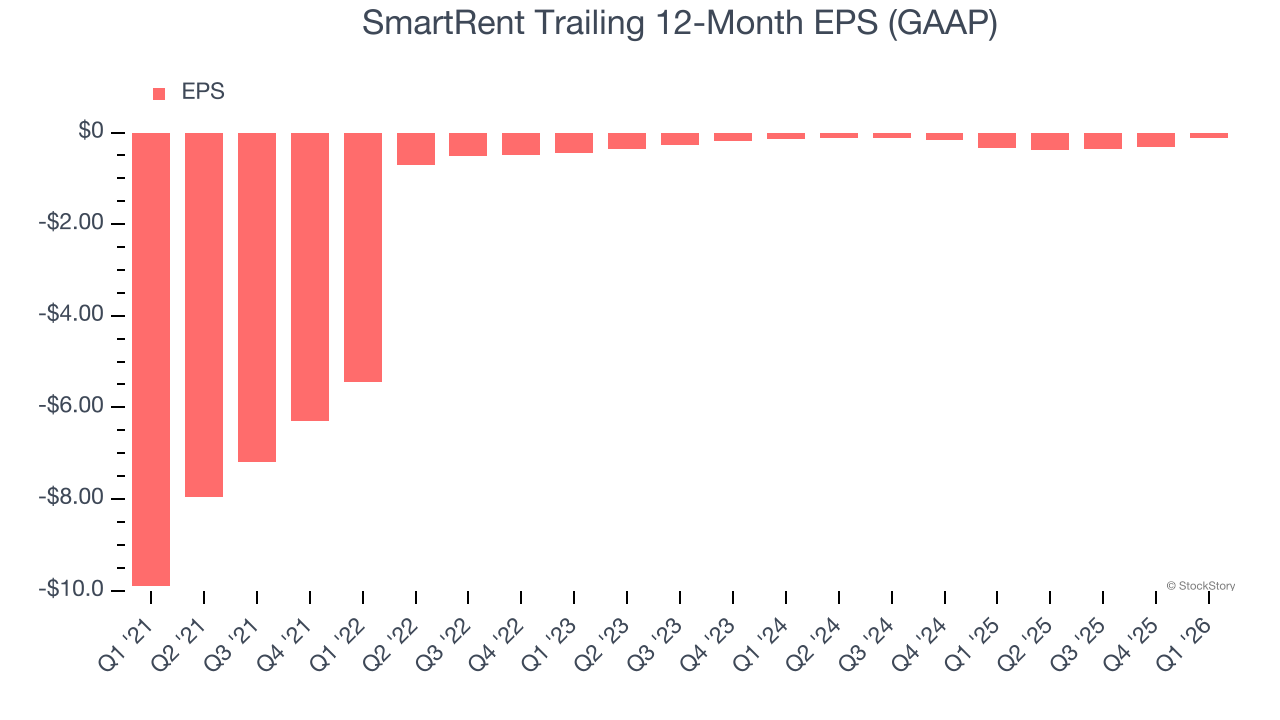

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although SmartRent’s full-year earnings are still negative, it reduced its losses and improved its EPS by 58.1% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For SmartRent, its two-year annual EPS growth of 5.8% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q1, SmartRent reported EPS of negative $0.02, up from negative $0.21 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from SmartRent’s Q1 Results

We were impressed by how significantly SmartRent blew past analysts’ adjusted operating income expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its EBITDA missed and its EPS was in line with Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 8.2% to $1.29 immediately after reporting.

The latest quarter from SmartRent’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).