As the Q1 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the business services & supplies industry, including Copart (NASDAQ: CPRT) and its peers.

This is a sector that encompasses many types of business, and so it follows that a number of trends will impact the space. For industrial and environmental services companies, for example, trends around environmental compliance and increasing corporate ESG commitments matter while for safety and security services companies, the intersection of physical security, cybersecurity, and workplace safety regulations are the topics du jour. Broadly, AI and automation could be tailwinds for companies in the space that invest wisely. On the other hand, shifting regulatory frameworks could force continual changes in go-to-market and costly investments.

The 19 business services & supplies stocks we track reported a strong Q1. As a group, revenues beat analysts’ consensus estimates by 2.5% while next quarter’s revenue guidance was in line.

Thankfully, share prices of the companies have been resilient as they are up 5% on average since the latest earnings results.

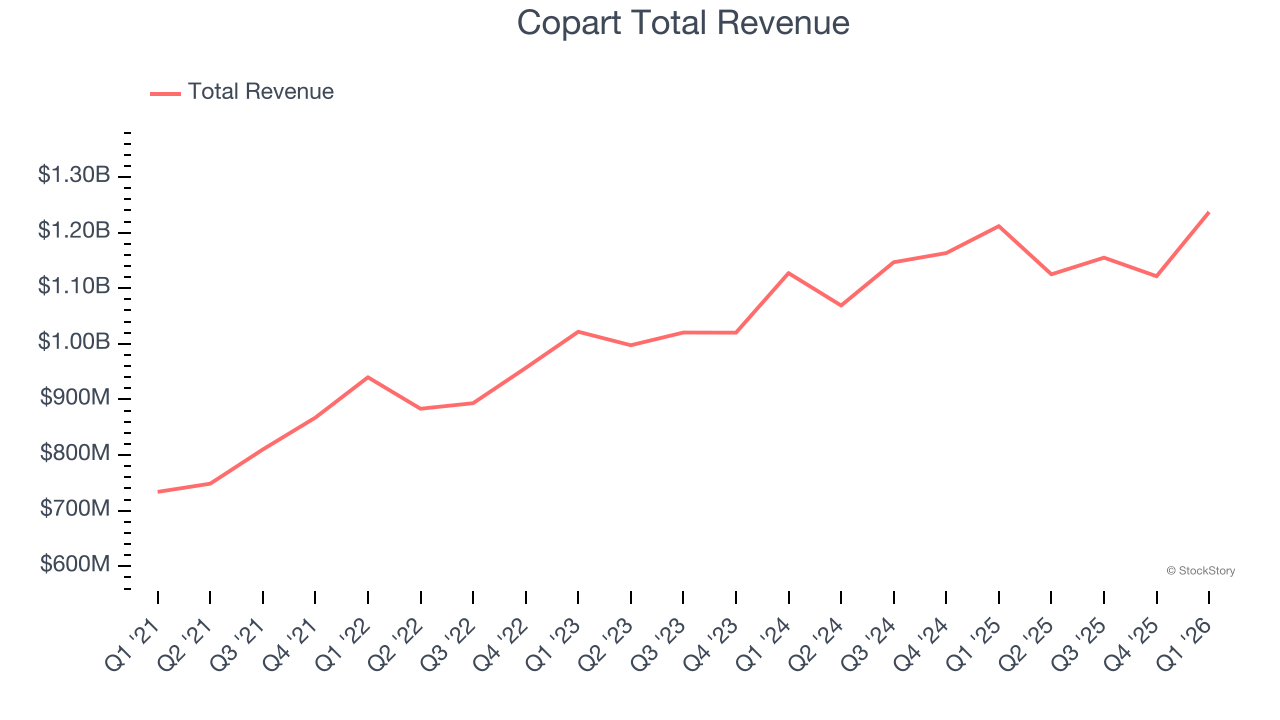

Copart (NASDAQ: CPRT)

Starting as a single salvage yard in California in 1982, Copart (NASDAQ: CPRT) operates an online auction platform that connects sellers of damaged and salvage vehicles with buyers ranging from dismantlers and rebuilders to used car dealers and exporters.

Copart reported revenues of $1.24 billion, up 2.1% year on year. This print exceeded analysts’ expectations by 4.2%. Overall, it was a very strong quarter for the company with an impressive beat of analysts’ revenue and EPS estimates.

Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 10.2% since reporting and currently trades at $30.91.

We think Copart is a good business, but is it a buy today? Read our full report here, it’s free.

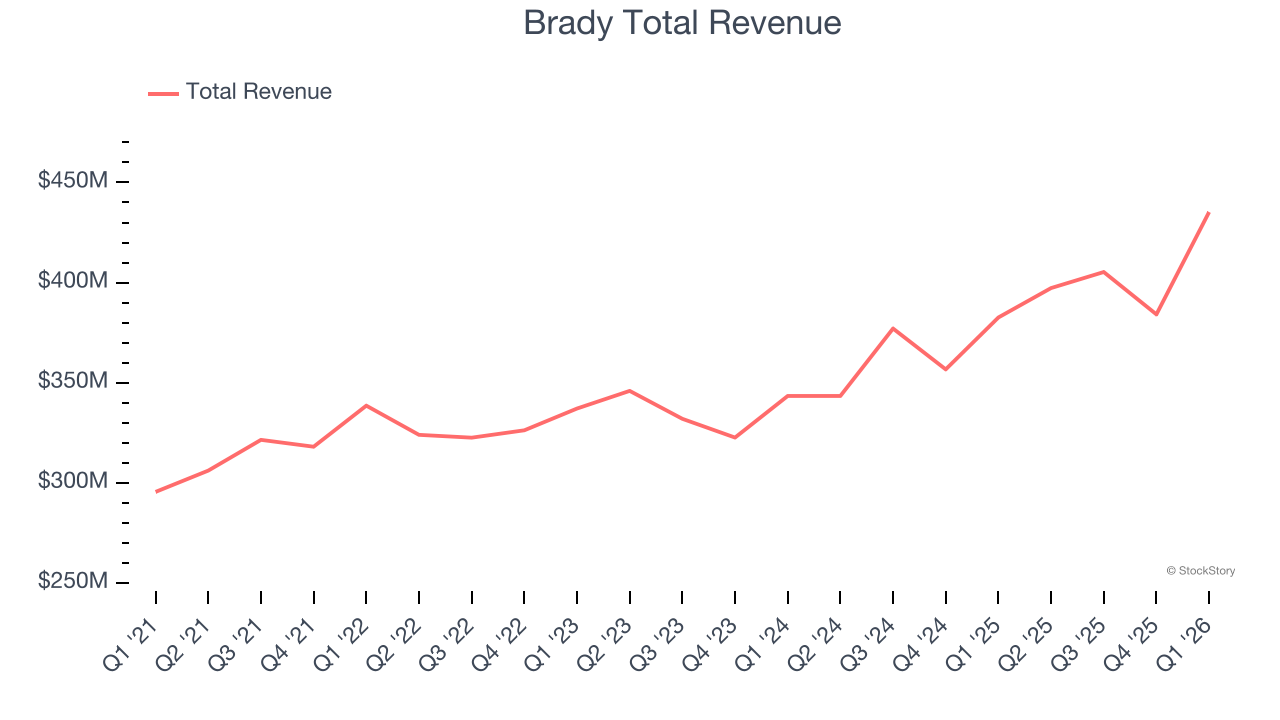

Best Q1: Brady (NYSE: BRC)

Founded in 1914 and evolving through more than a century of industrial innovation, Brady (NYSE: BRC) manufactures and supplies identification solutions and workplace safety products that help companies identify and protect their premises, products, and people.

Brady reported revenues of $435.2 million, up 13.8% year on year, outperforming analysts’ expectations by 7.2%. The business had a stunning quarter with an impressive beat of analysts’ full-year EPS guidance estimates.

The market seems happy with the results as the stock is up 6.8% since reporting. It currently trades at $75.80.

Is now the time to buy Brady? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: MillerKnoll (NASDAQ: MLKN)

Created through the 2021 merger of industry icons Herman Miller and Knoll, MillerKnoll (NASDAQ: MLKN) designs, manufactures, and distributes interior furnishings for offices, healthcare facilities, educational settings, and homes worldwide.

MillerKnoll reported revenues of $926.6 million, up 5.8% year on year, falling short of analysts’ expectations by 1.6%. It was a disappointing quarter as it posted a significant miss of analysts’ EPS estimates.

As expected, the stock is down 24.8% since the results and currently trades at $14.55.

Read our full analysis of MillerKnoll’s results here.

RB Global (NYSE: RBA)

Born from the 1958 founding of Ritchie Bros. Auctioneers and rebranded in 2023, RB Global (NYSE: RBA) operates global marketplaces that connect buyers and sellers of commercial assets, vehicles, and equipment across multiple industries.

RB Global reported revenues of $1.23 billion, up 11.4% year on year. This print surpassed analysts’ expectations by 6.9%. Overall, it was a very strong quarter as it also produced a solid beat of analysts’ revenue and EPS estimates.

The stock is flat since reporting and currently trades at $104.56.

Read our full, actionable report on RB Global here, it’s free.

Vestis (NYSE: VSTS)

Operating a network of more than 350 facilities with 3,300 delivery routes serving customers weekly, Vestis (NYSE: VSTS) provides uniform rentals, workplace supplies, and facility services to over 300,000 business locations across the United States and Canada.

Vestis reported revenues of $659.4 million, flat year on year. This result beat analysts’ expectations by 0.7%. Taking a step back, it was a slower quarter as it logged EPS in line with analysts’ estimates.

The stock is up 34.1% since reporting and currently trades at $12.47.

Read our full, actionable report on Vestis here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.