Over the past six months, Marsh’s shares (currently trading at $176.36) have posted a disappointing 5.9% loss, well below the S&P 500’s 8.4% gain. This may have investors wondering how to approach the situation.

Given the weaker price action, is this a buying opportunity for MRSH? Find out in our full research report, it’s free.

Why Are We Positive on MRSH?

With roots dating back to 1871 and a presence in over 130 countries, Marsh (NYSE: MRSH) is a global professional services firm that helps organizations manage risk, strategy, and workforce challenges through its four specialized businesses.

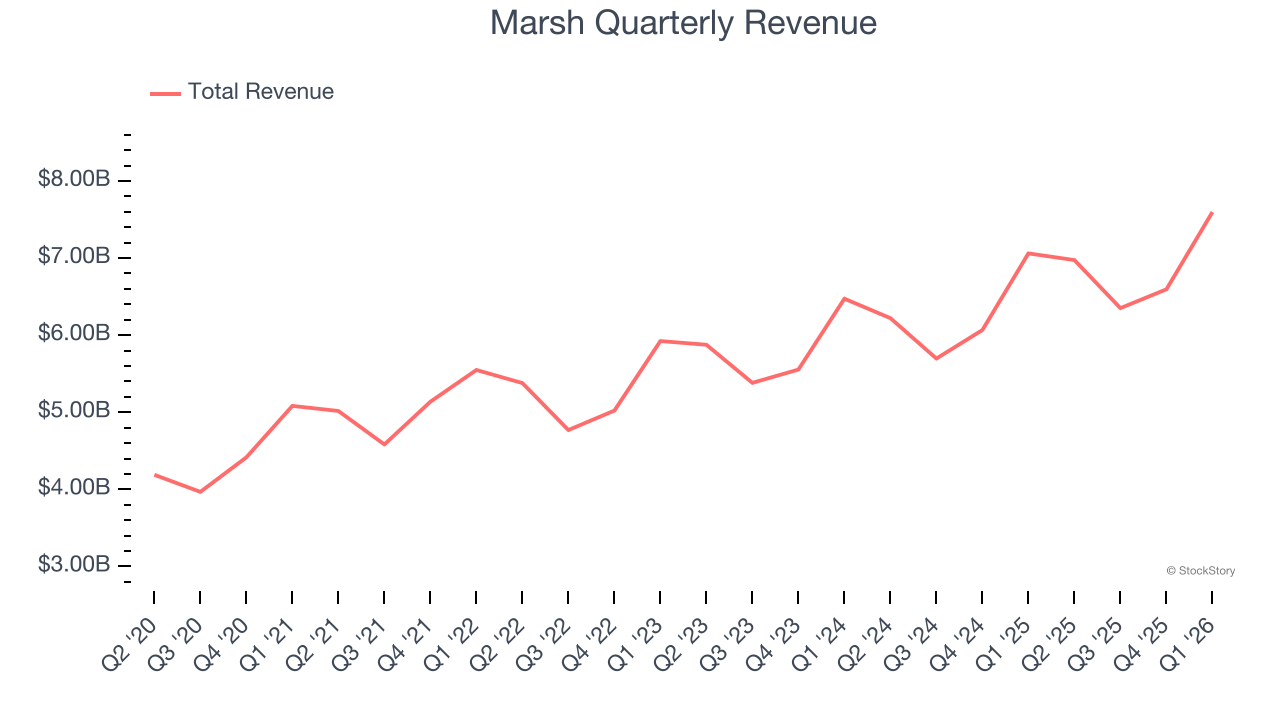

1. Skyrocketing Revenue Shows Strong Momentum

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Marsh’s sales grew at an impressive 9.3% compounded annual growth rate over the last five years. Its growth beat the average business services company and shows its offerings resonate with customers.

2. Economies of Scale Give It Negotiating Leverage with Suppliers

With $27.52 billion in revenue over the past 12 months, Marsh is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices.

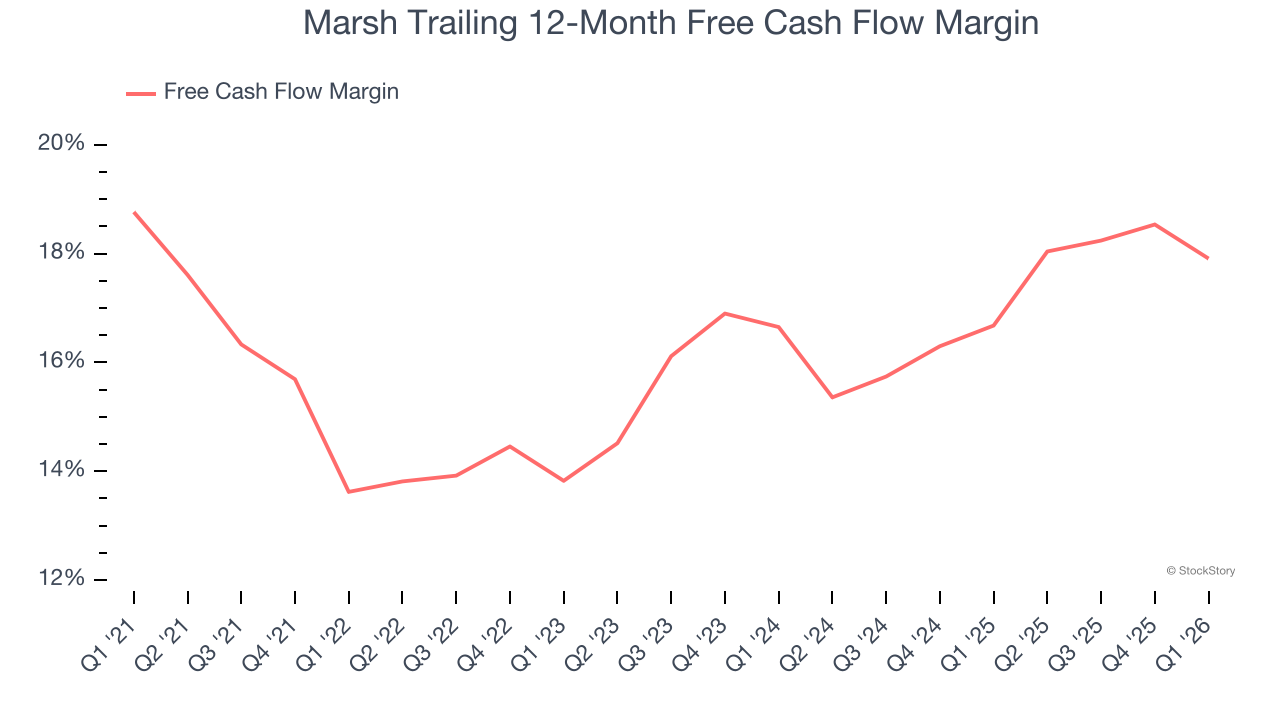

3. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Marsh has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the business services sector, averaging 15.9% over the last five years.

Final Judgment

These are just a few reasons why we think Marsh is a high-quality business. With the recent decline, the stock trades at 16.2× forward P/E (or $176.36 per share). Is now a good time to initiate a position? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.