Independent Bank trades at $84.21 and has moved in lockstep with the market. Its shares have returned 12.9% over the last six months while the S&P 500 has gained 8.4%.

Is now the time to buy Independent Bank, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Independent Bank Not Exciting?

We’re swiping left on Independent Bank for now. Here are three reasons why there are better opportunities than INDB, plus one stock we’d rather own.

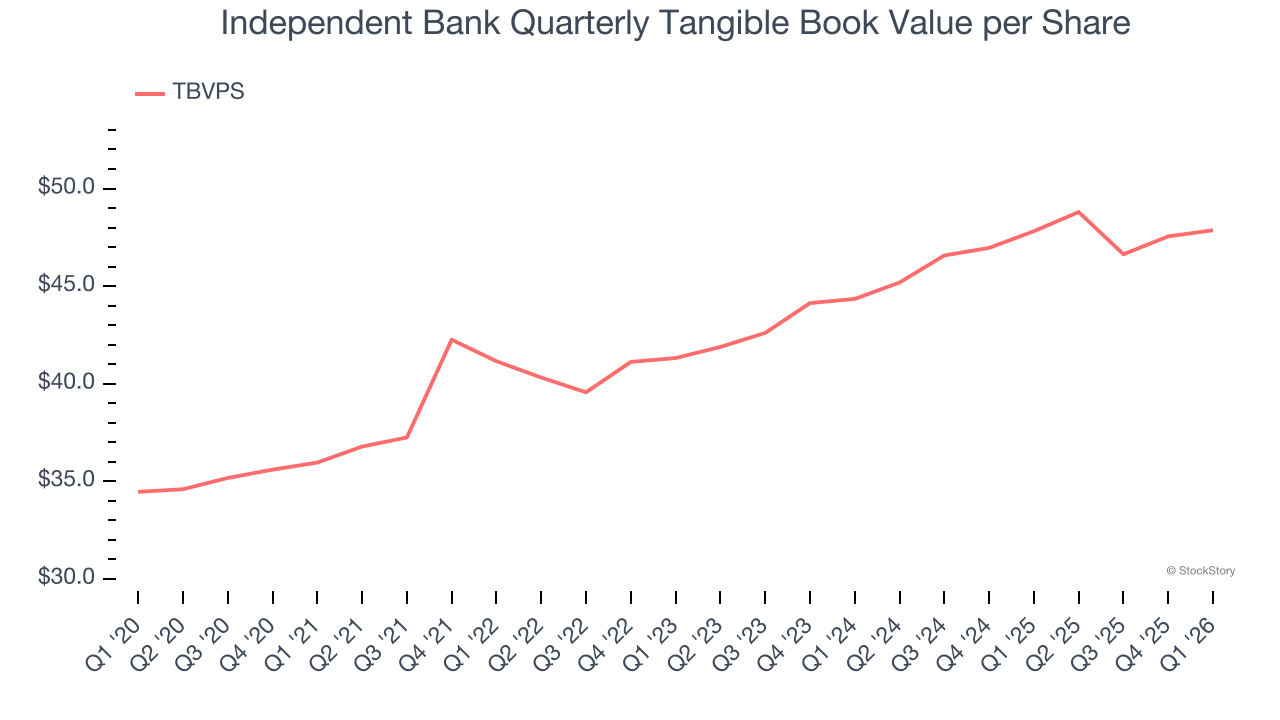

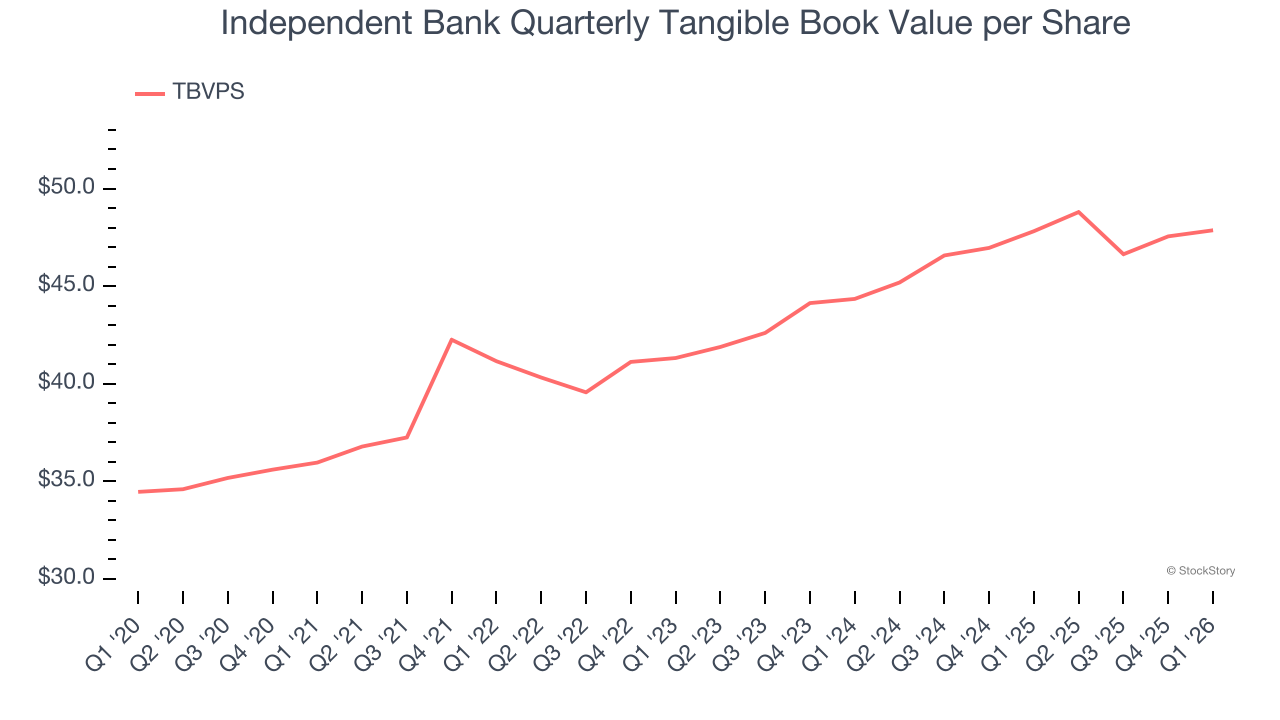

1. Substandard TBVPS Growth Indicates Limited Asset Expansion

For banks, tangible book value per share (TBVPS) is a crucial metric that measures the actual value of shareholders’ equity, stripping out goodwill and other intangible assets that may not be recoverable in a worst-case scenario.

Although Independent Bank’s TBVPS increased by 5.9% annually over the last five years, growth has recently decelerated a bit to a sluggish 3.9% over the past two years (from $44.34 to $47.86 per share).

2. Projected TBVPS Growth Is Slim

A bank’s tangible book value per share (TBVPS) increases when it generates higher net interest margins and keeps credit losses low, allowing it to compound shareholder value over time.

Over the next 12 months, Consensus estimates call for Independent Bank’s TBVPS to grow by 9% to $52.15, paltry growth rate.

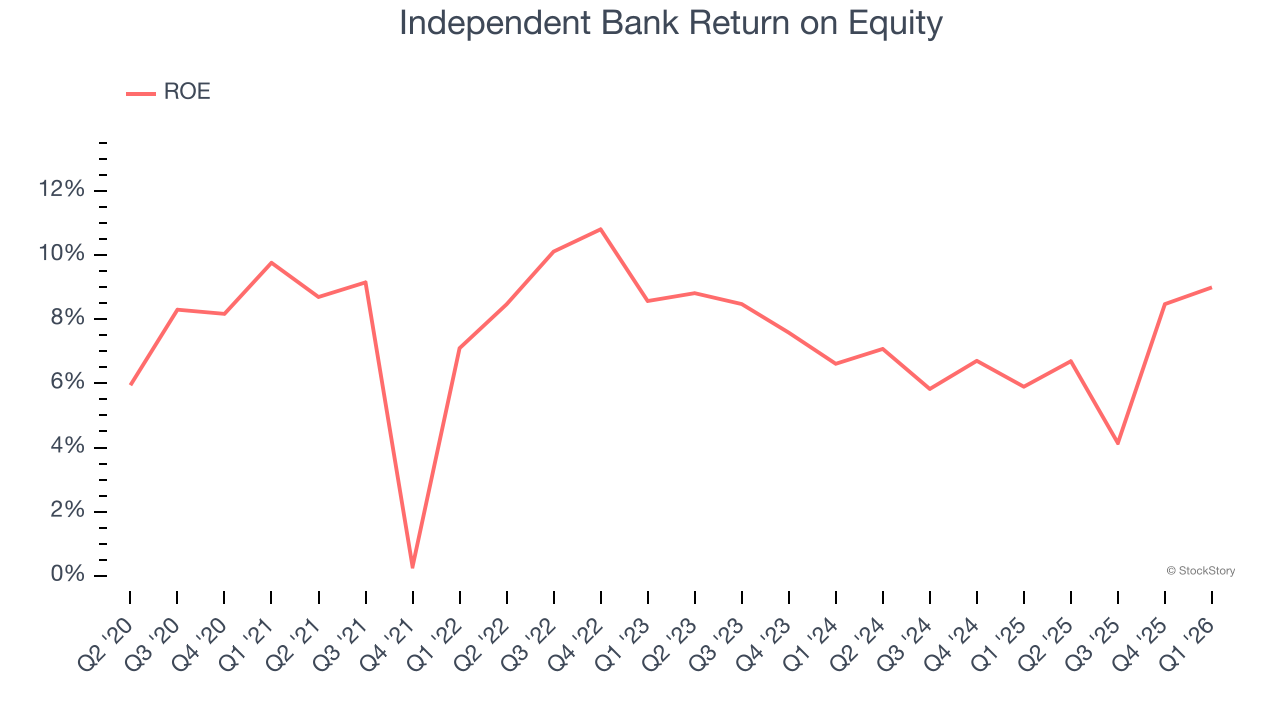

3. Previous Growth Initiatives Haven’t Impressed

Return on equity (ROE) reveals the profit generated per dollar of shareholder equity, which represents a key source of bank funding. Banks maintaining elevated ROE levels tend to accelerate wealth creation for shareholders via earnings retention, buybacks, and distributions.

Over the last five years, Independent Bank has averaged an ROE of 7.4%, uninspiring for a company operating in a sector where the average shakes out around 7.5%.

Final Judgment

Independent Bank isn’t a terrible business, but it doesn’t pass our bar. That said, the stock currently trades at 1.1× forward P/B (or $84.21 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We’re pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.