If you’ve got a big international payment coming up, there is no doubt that the exchange rate will be playing a big part of the decision, both emotionally and financially.

This is even more prevalent in today’s climate.

For big transfers, the real question isn’t “where’s the rate going next?” - it’s “what’s the smartest way to convert this amount, given what I know now?”

Why "waiting for a better rate" usually loses

Waiting around for a better rate rarely works.

But currency markets move both ways, and short-term changes are basically random. If you’re timing a single transfer, you’re guessing. Even professionals can’t predict the movements with much accuracy.

Loss aversion makes waiting feel safer than it is. If the rate moves 2% against you, that loss stings. If it moves 2% in your favor, you might assume you could’ve done even better by waiting. This psychological loop can keep you stuck, always hoping for a rate that might never show up.

The real risk? Opportunity cost. While you wait, you’re exposed to the risk of the rate moving against you. Here’s what that can look like on a $100,000 transfer:

- 1% adverse move: $1,000 loss

- 3% adverse move: $3,000 loss

- 5% adverse move: $5,000 loss

These aren’t just numbers - they’re real costs if the market turns the wrong way. If you have to make the transfer eventually, every day you wait is a gamble.

The four main options for converting

If you’re moving a large sum across currencies, you basically have four main choices.

Banks are the obvious route. You can convert through your bank, usually online or over the phone. It’s easy, but banks often add a 3-5% markup to the mid-market rate, and their fees don’t always tell the whole story.

Currency brokers focus on foreign exchange and usually offer better rates than banks, especially for transfers over $20,000. They’ll assign you a dealer to help with timing and execution. Most brokers also let you lock in rates for future transfers with forward contracts.

Online transfer platforms like Wise, OFX, or CurrencyFair are somewhere in the middle. They charge less than banks and show you exactly what you’ll pay. These are great for straightforward transfers if you don’t need phone support or fancy hedging tools.

Currency exchange bureaus mostly handle cash. For big transfers, they’re not really relevant since those almost always happen electronically. Their rates are usually worse, and you’ll run into limits on how much you can convert in a visit.

Your best option depends on how much you’re moving, how fast you need it, and whether you want risk management tools like forwards or limit orders. For anything over $50,000, brokers usually give you the best mix of rate and service.

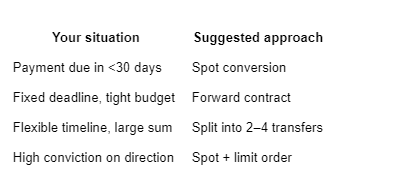

A simple framework for deciding

Three questions can help you pick the right approach for your transfer.

When do you need the money? If you need to pay within days or weeks, just do a spot transaction at the current rate and move on. If you’ve got 2–6 months, forward contracts are worth a look. With more time, you might split your conversion into a few chunks to even out volatility.

How much rate movement can you handle? This one matters more than most people think. If a 5% swing would blow up your plans - say, you’re buying a property right at your budget limit - locking in a rate is probably smarter than hoping for upside. Forward contracts are designed for this exact scenario.

Do you actually have a view on direction, or are you just guessing? Be real with yourself. If you’re guessing, structure will always beat timing.

Forward contracts and market orders used to be for big companies, but now most specialist providers offering currency exchange for businesses make these tools available to individuals moving large sums, often with no minimums.

Here’s a simple decision matrix:

Honestly, the tools for structuring a smart conversion are more accessible than most people think. It’s just a matter of matching the right tool to your own needs and comfort with risk.

The most common mistake

The single biggest mistake? People default to their bank for a large transfer without comparing rates or thinking about how to structure the transaction.

Most folks just assume their bank is the obvious choice. It's familiar, feels secure, and the process seems easy enough. But that convenience can get really expensive.

Why this is expensive:

- Banks usually set exchange rates for big FX transactions 2–4% off the mid-market rate.

- Retail banking customers rarely get access to forward contracts or limit orders.

- You end up paying more and missing out on tools to manage timing and volatility.

Just for context: a 3% markup on a $100,000 transfer means you lose $3,000 to the spread - before you even see any wire fees.

The simple fix:

If you're planning to shift a significant amount (anything above $20k, usually) it makes sense to speak to a currency provider first.

No need to commit. Just know what you're giving up if you don't at least ask.