Timeshare vacation company Hilton Grand Vacations (NYSE: HGV) missed Wall Street’s revenue expectations in Q2 CY2025 as sales rose 2.5% year on year to $1.27 billion. Its GAAP profit of $0.25 per share was 65.7% below analysts’ consensus estimates.

Is now the time to buy Hilton Grand Vacations? Find out by accessing our full research report, it’s free.

Hilton Grand Vacations (HGV) Q2 CY2025 Highlights:

- Revenue: $1.27 billion vs analyst estimates of $1.38 billion (2.5% year-on-year growth, 8.1% miss)

- EPS (GAAP): $0.25 vs analyst expectations of $0.73 (65.7% miss)

- Adjusted EBITDA: $180 million vs analyst estimates of $275.9 million (14.2% margin, 34.8% miss)

- Operating Margin: 34.1%, up from 7.6% in the same quarter last year

- Free Cash Flow Margin: 2.2%, down from 30% in the same quarter last year

- Market Capitalization: $4.65 billion

Company Overview

Spun off from Hilton Worldwide in 2017, Hilton Grand Vacations (NYSE: HGV) is a global timeshare company that provides travel experiences for its customers through its timeshare resorts and club membership programs.

Revenue Growth

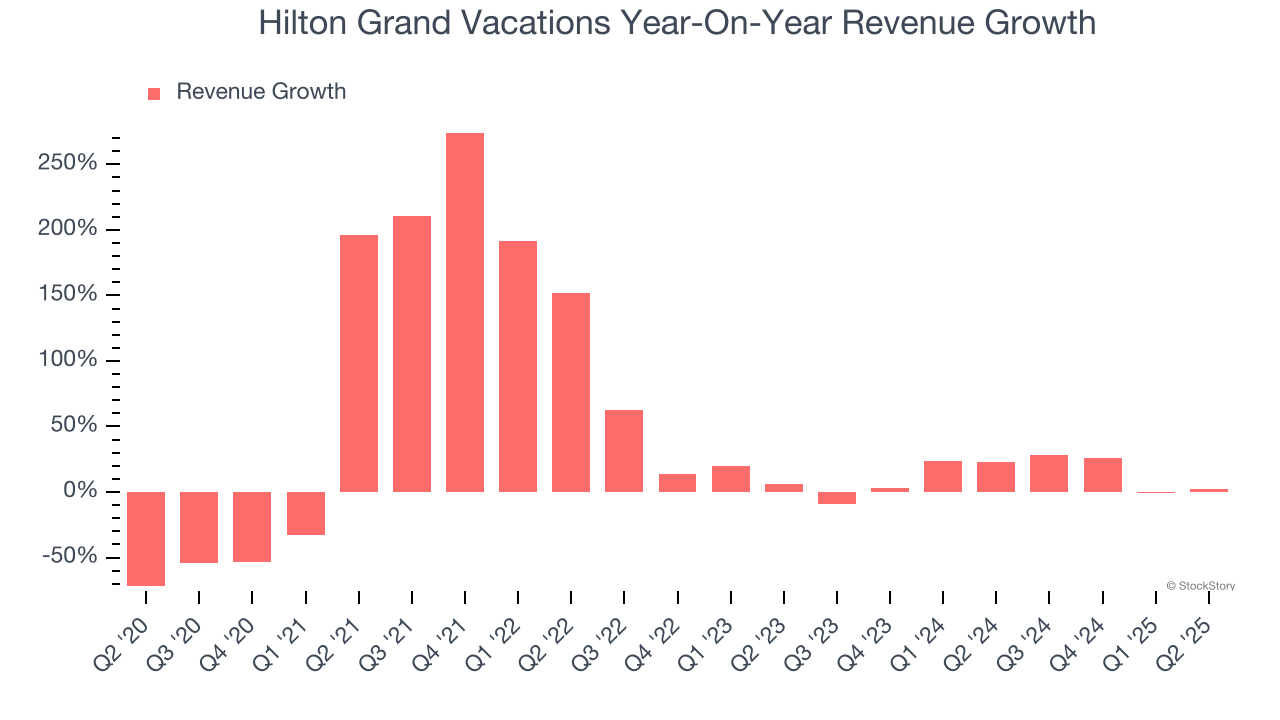

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Hilton Grand Vacations’s 27.1% annualized revenue growth over the last five years was exceptional. Its growth beat the average consumer discretionary company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or trend. Hilton Grand Vacations’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 11.2% over the last two years was well below its five-year trend.

This quarter, Hilton Grand Vacations’s revenue grew by 2.5% year on year to $1.27 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 11.3% over the next 12 months, similar to its two-year rate. This projection is underwhelming and implies its newer products and services will not catalyze better top-line performance yet.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

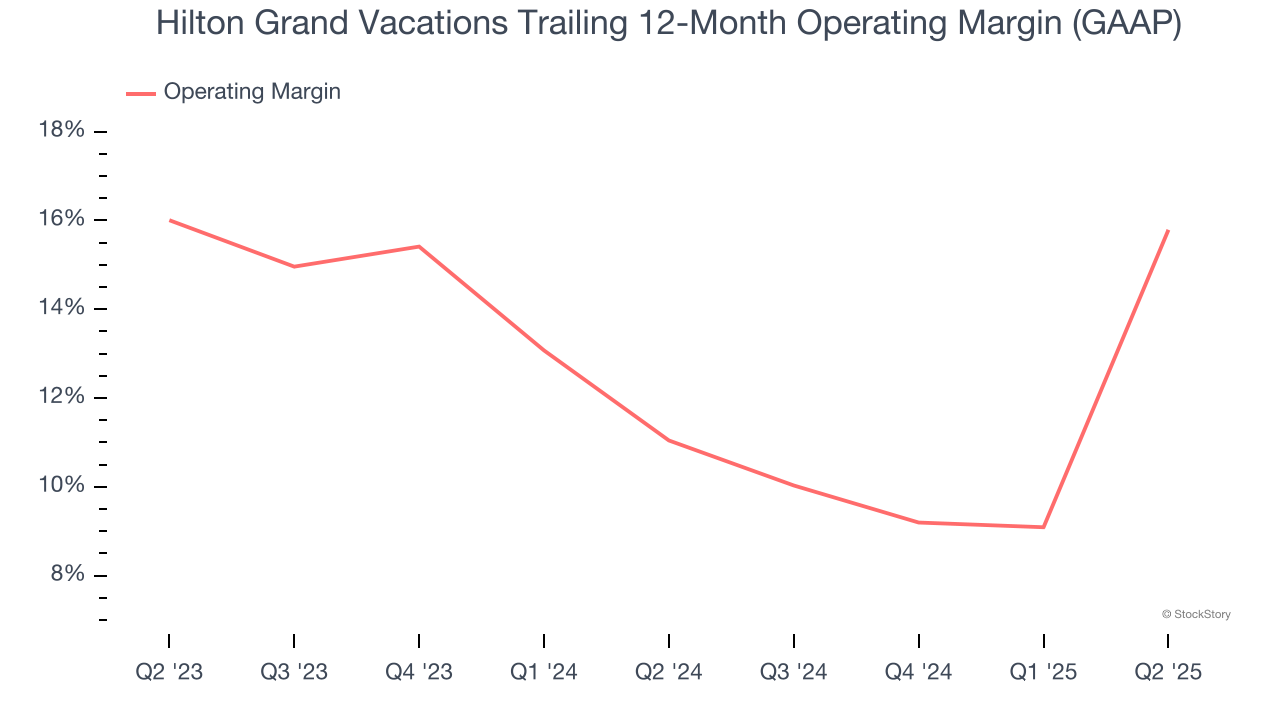

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Hilton Grand Vacations’s operating margin has risen over the last 12 months and averaged 13.6% over the last two years. Its solid profitability for a consumer discretionary business shows it’s an efficient company that manages its expenses effectively.

In Q2, Hilton Grand Vacations generated an operating margin profit margin of 34.1%, up 26.5 percentage points year on year. This increase was a welcome development and shows it was more efficient.

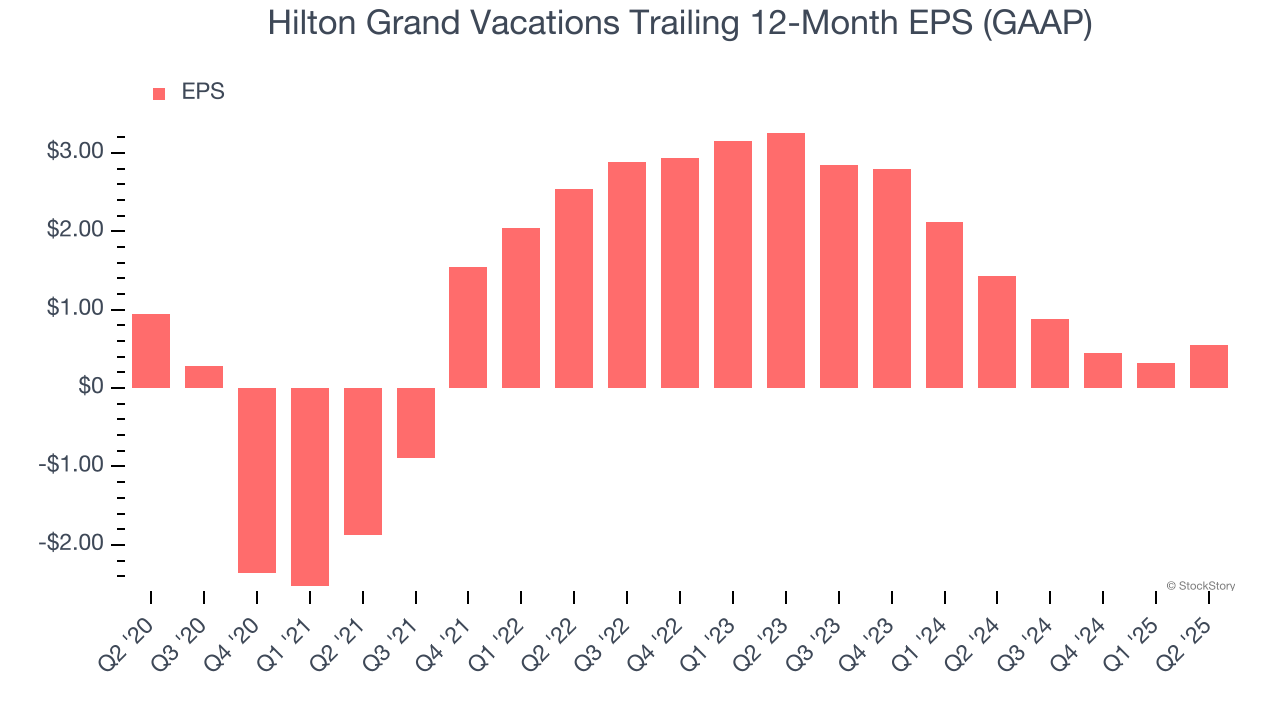

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Hilton Grand Vacations, its EPS declined by 10.4% annually over the last five years while its revenue grew by 27.1%. However, its operating margin actually improved during this time, telling us that non-fundamental factors such as interest expenses and taxes affected its ultimate earnings.

In Q2, Hilton Grand Vacations reported EPS at $0.25, up from $0.02 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Hilton Grand Vacations’s full-year EPS of $0.55 to grow 480%.

Key Takeaways from Hilton Grand Vacations’s Q2 Results

We struggled to find many positives in these results. Its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 3.5% to $49 immediately after reporting.

Hilton Grand Vacations may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.