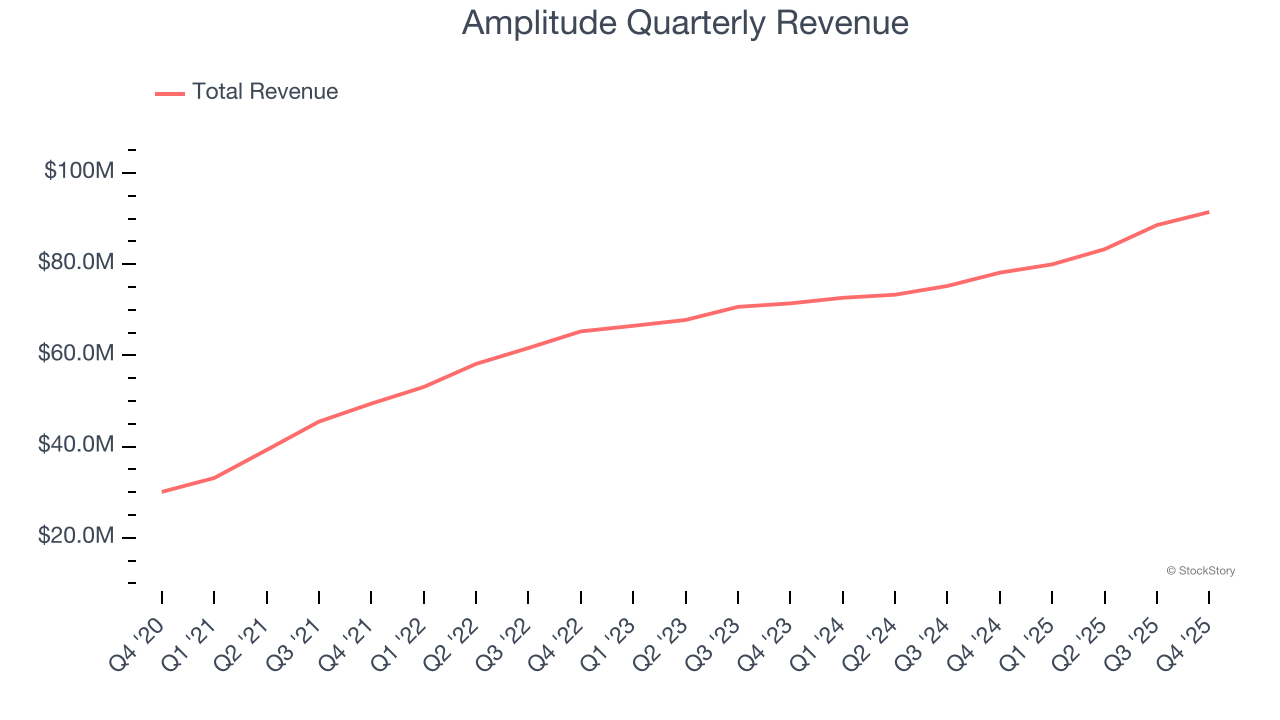

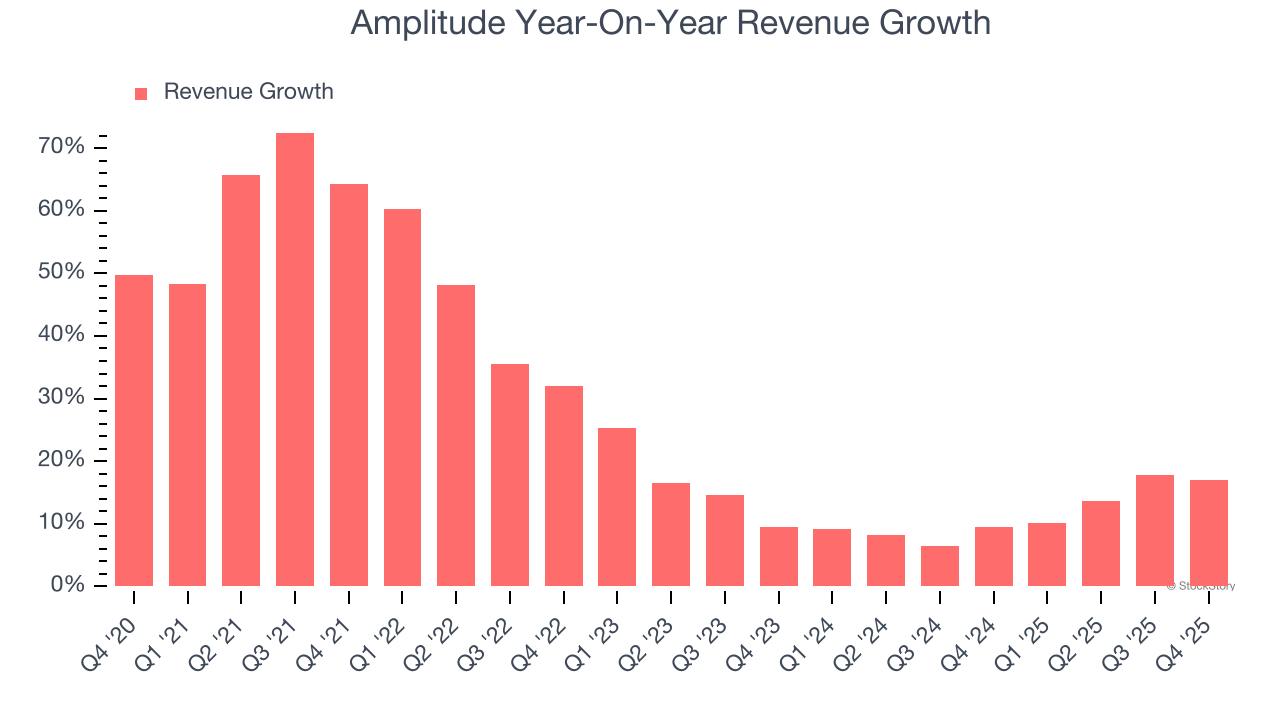

Digital analytics platform Amplitude (NASDAQ: AMPL) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 17% year on year to $91.43 million. Guidance for next quarter’s revenue was better than expected at $92.7 million at the midpoint, 0.6% above analysts’ estimates. Its non-GAAP profit of $0.04 per share was in line with analysts’ consensus estimates.

Is now the time to buy Amplitude? Find out by accessing our full research report, it’s free.

Amplitude (AMPL) Q4 CY2025 Highlights:

- Revenue: $91.43 million vs analyst estimates of $90.35 million (17% year-on-year growth, 1.2% beat)

- Adjusted EPS: $0.04 vs analyst estimates of $0.05 (in line)

- Adjusted Operating Income: $4.18 million vs analyst estimates of $4.59 million (4.6% margin, relatively in line)

- Revenue Guidance for Q1 CY2026 is $92.7 million at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for the upcoming financial year 2026 is $0.11 at the midpoint, missing analyst estimates by 9.8%

- Operating Margin: -20.8%, up from -45.4% in the same quarter last year

- Free Cash Flow Margin: 12.2%, up from 3.8% in the previous quarter

- Customers: 4,700, up from 4,500 in the previous quarter

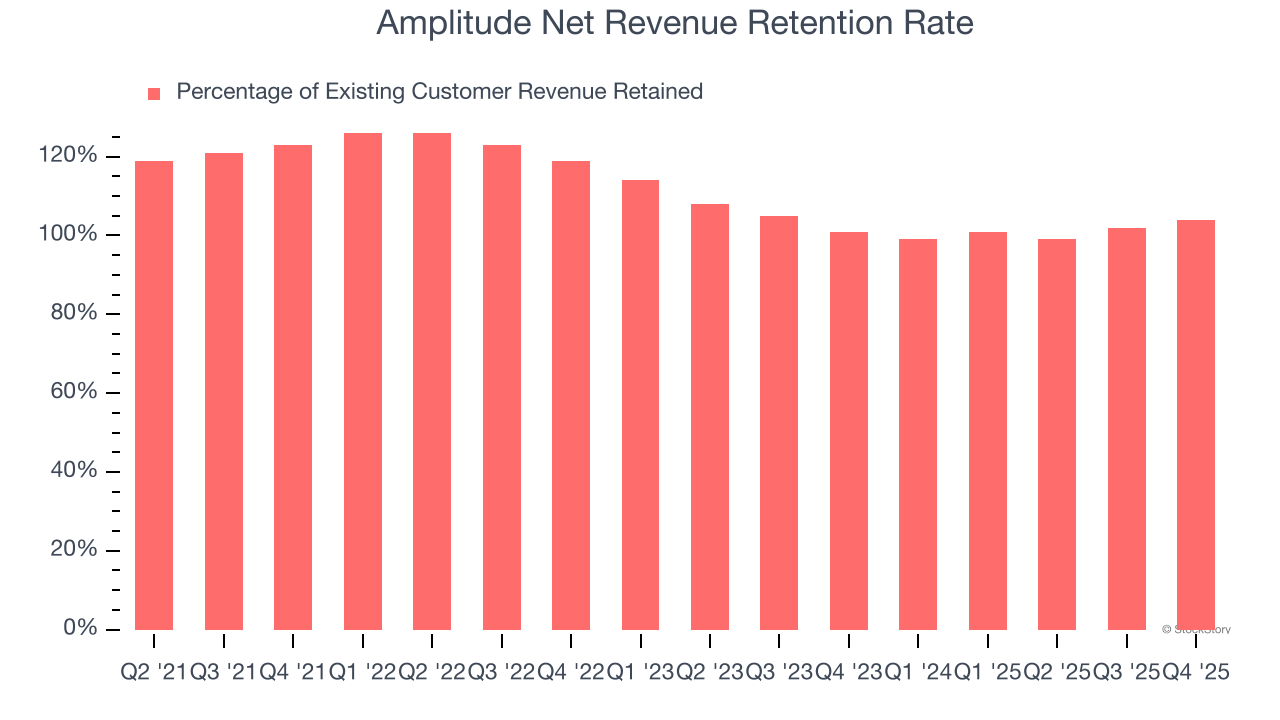

- Net Revenue Retention Rate: 104%, up from 102% in the previous quarter

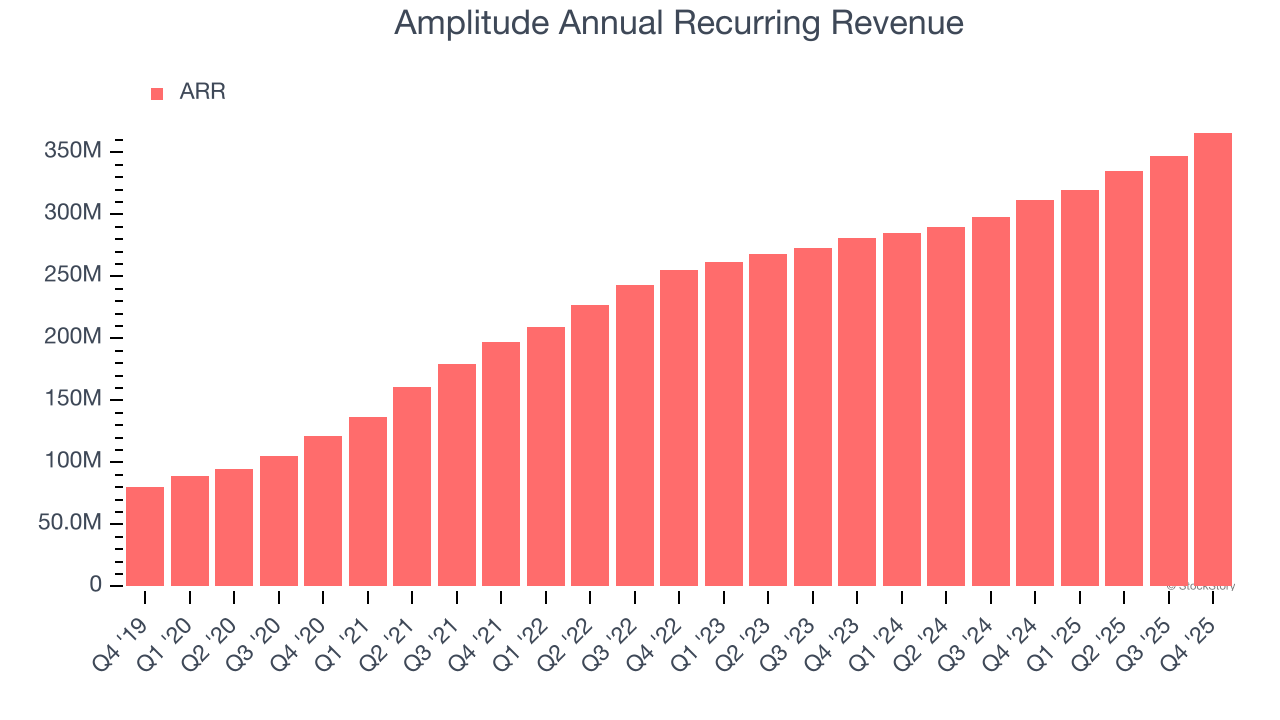

- Annual Recurring Revenue: $366 million (17.3% year-on-year growth, beat)

- Market Capitalization: $847.6 million

Company Overview

Born from the realization that companies were flying blind when it came to understanding user behavior in their digital products, Amplitude (NASDAQ: AMPL) provides a digital analytics platform that helps businesses understand how people use their digital products to improve user experiences and drive revenue growth.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Amplitude’s 27.3% annualized revenue growth over the last five years was impressive. Its growth beat the average software company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Amplitude’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 11.5% over the last two years was well below its five-year trend.

This quarter, Amplitude reported year-on-year revenue growth of 17%, and its $91.43 million of revenue exceeded Wall Street’s estimates by 1.2%. Company management is currently guiding for a 15.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13.7% over the next 12 months. Although this projection implies its newer products and services will catalyze better top-line performance, it is still below the sector average.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Amplitude’s ARR punched in at $366 million in Q4, and over the last four quarters, its growth slightly outpaced the sector as it averaged 15.4% year-on-year increases. This performance aligned with its total sales growth and shows the company is securing longer-term commitments. Its growth also contributes positively to Amplitude’s revenue predictability, a trait long-term investors typically prefer.

Customer Retention

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Amplitude’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 102% in Q4. This means Amplitude would’ve grown its revenue by 1.5% even if it didn’t win any new customers over the last 12 months.

Amplitude has an adequate net retention rate, showing us that it generally keeps customers but lags behind the best SaaS businesses, which routinely post net retention rates of 120%+.

Key Takeaways from Amplitude’s Q4 Results

It was good to see Amplitude expecting revenue growth to continue next year. We were also glad its net revenue retention grew. On the other hand, its full-year EPS guidance missed and its EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded up 2.6% to $7.37 immediately after reporting.

So do we think Amplitude is an attractive buy at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).