Since December 2025, EchoStar has been in a holding pattern, posting a small loss of 1.5% while floating around $104. The stock also fell short of the S&P 500’s 6.2% gain during that period.

Is there a buying opportunity in EchoStar, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think EchoStar Will Underperform?

We’re swiping left on EchoStar for now. Here are three reasons you should be careful with SATS, plus one stock we’d rather own.

1. Revenue Tumbling Downwards

Long-term growth is the most important, but within business services, a stretched historical view may miss new innovations or demand cycles. EchoStar’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 6.1% over the last two years.

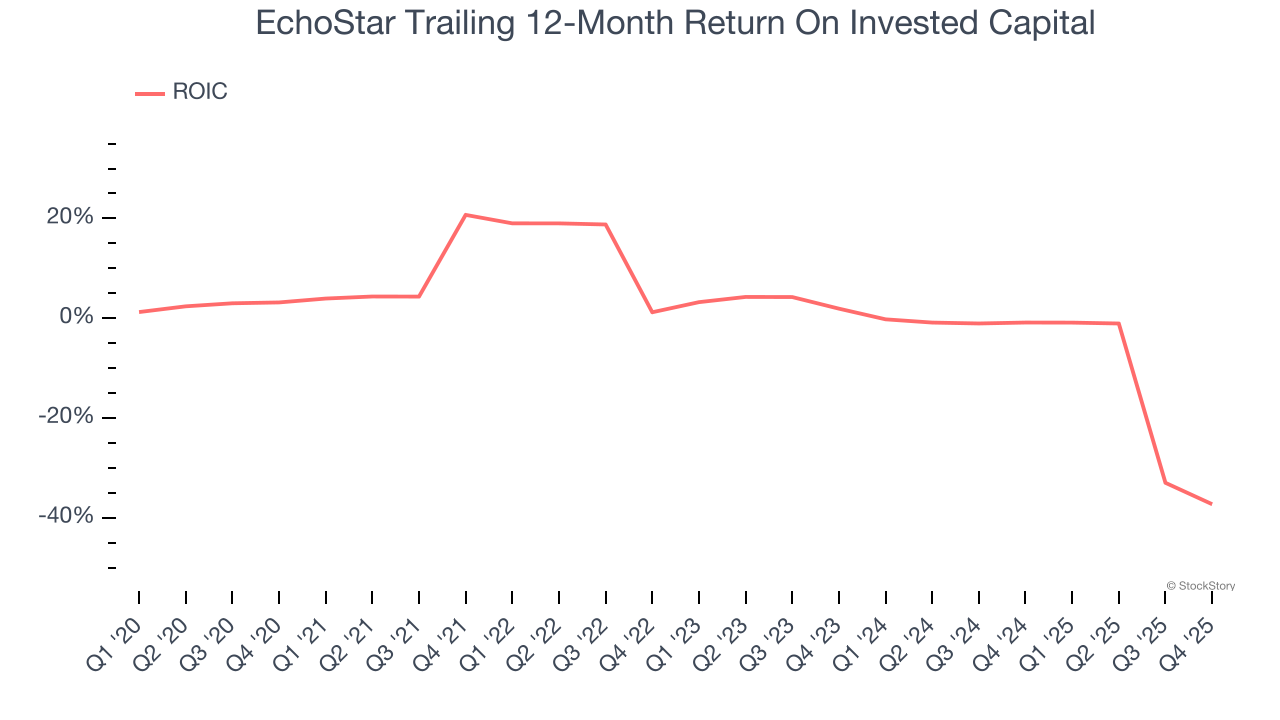

2. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Over the last few years, EchoStar’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

3. Restricted Access to Capital Increases Risk

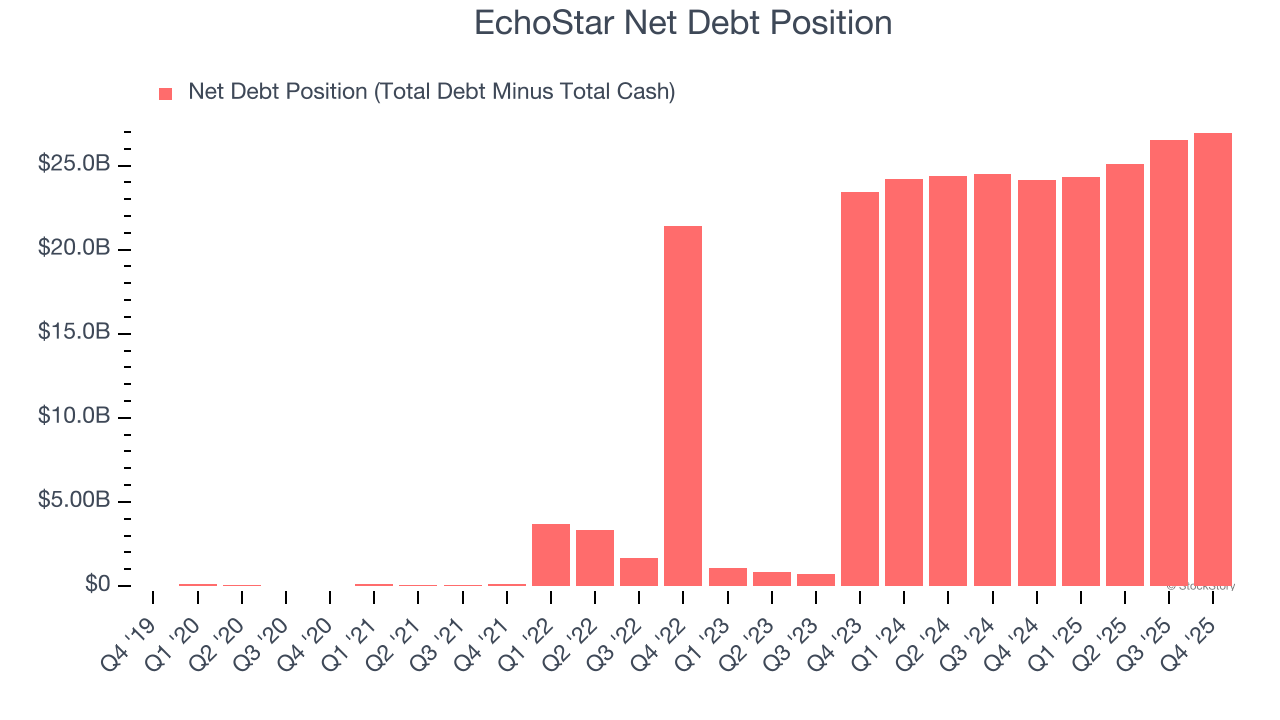

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

EchoStar posted negative $16.14 billion of EBITDA over the last 12 months, and its $30.12 billion of debt exceeds the $3.16 billion of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

We implore our readers to tread carefully because credit agencies could downgrade EchoStar if its unprofitable ways continue, making incremental borrowing more expensive and restricting growth prospects. The company could also be backed into a corner if the market turns unexpectedly. We hope EchoStar can improve its profitability and remain cautious until then.

Final Judgment

We cheer for all companies making their customers lives easier, but in the case of EchoStar, we’ll be cheering from the sidelines. With its shares lagging the market recently, the stock trades at 24.6× forward EV-to-EBITDA (or $104 per share). At this valuation, there’s a lot of good news priced in - you can find more timely opportunities elsewhere. Let us point you toward one of our top software and edge computing picks.

Stocks We Would Buy Instead of EchoStar

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.