Seagate has been on fire lately. In the past six months alone, the company’s stock price has rocketed 220%, reaching $901.50 per share. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now still a good time to buy STX? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

Why Are We Positive on STX?

One of two remaining major hard drive manufacturers after decades of industry consolidation, Seagate (NASDAQ: STX) manufactures hard disk drives and solid state drives that store data in data centers, cloud systems, and consumer devices.

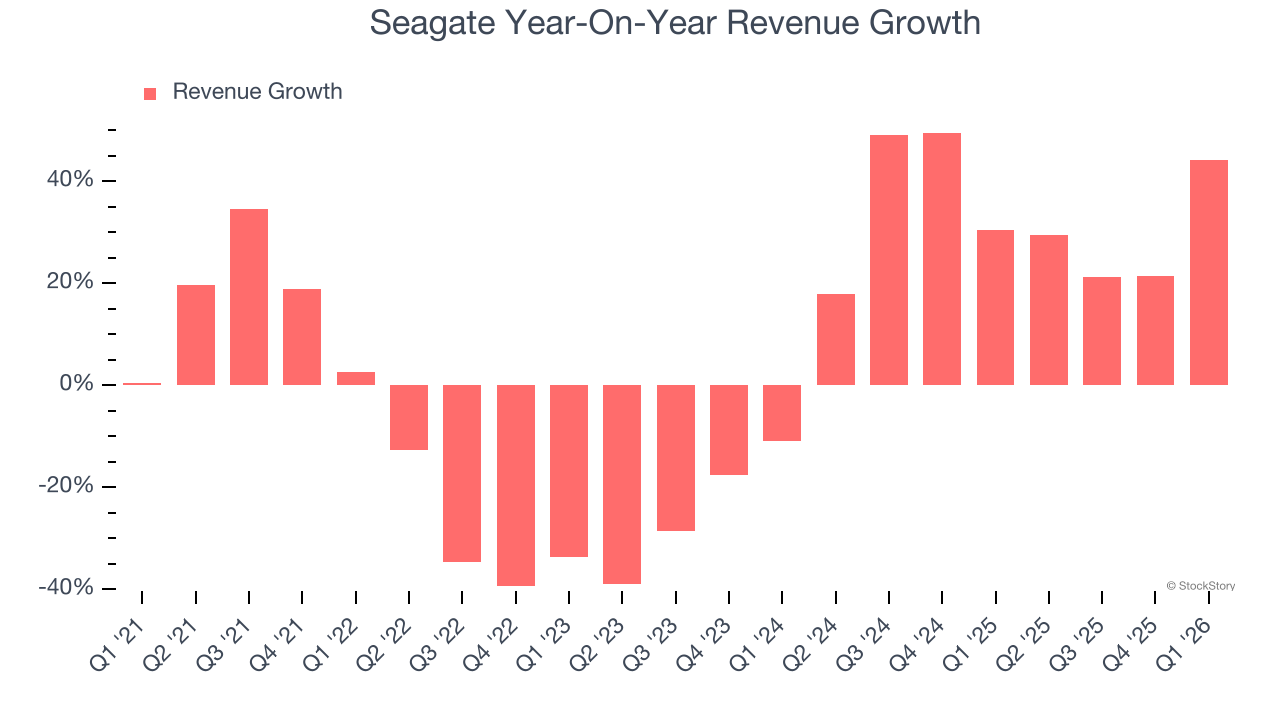

1. Skyrocketing Revenue Shows Strong Momentum

We at StockStory place the most emphasis on long-term growth, but within semiconductors, a stretched historical view may miss new demand cycles or industry trends like AI. Seagate’s annualized revenue growth of 32.6% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

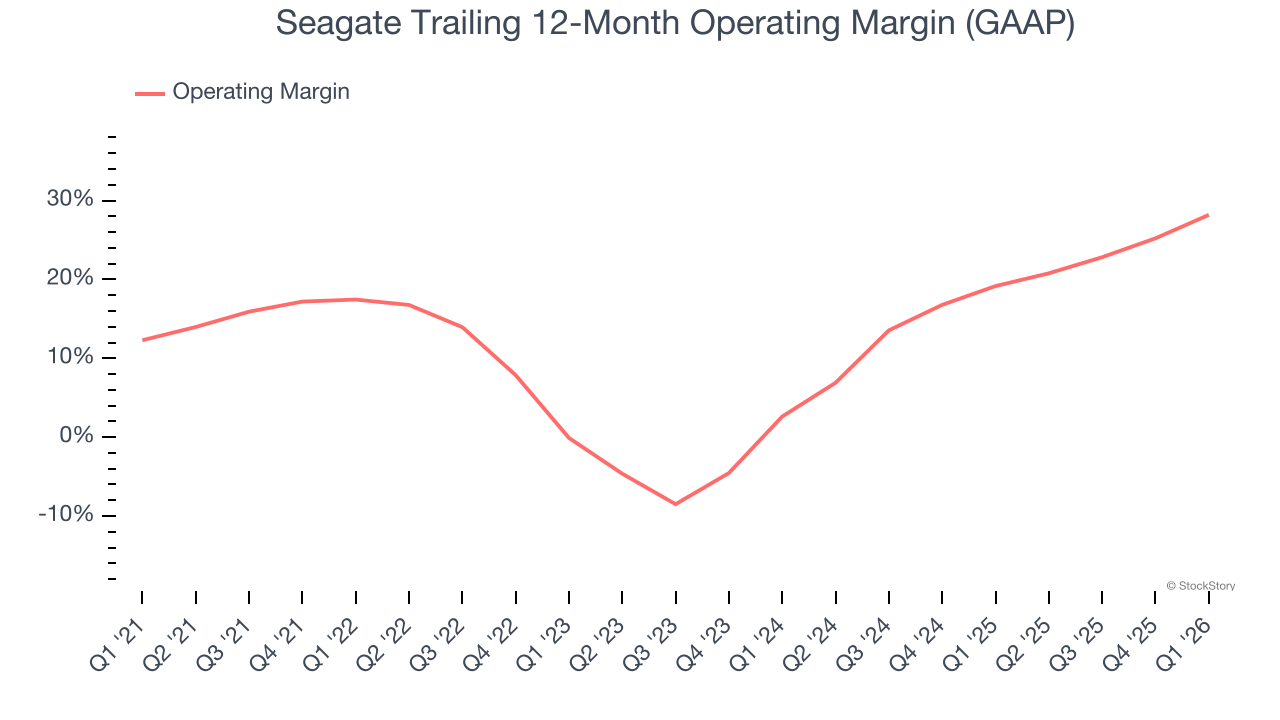

2. Operating Margin Rising, Profits Up

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Analyzing the trend in its profitability, Seagate’s operating margin rose by 10.7 percentage points over the last five years, as its sales growth gave it operating leverage. Its operating margin for the trailing 12 months was 28.2%.

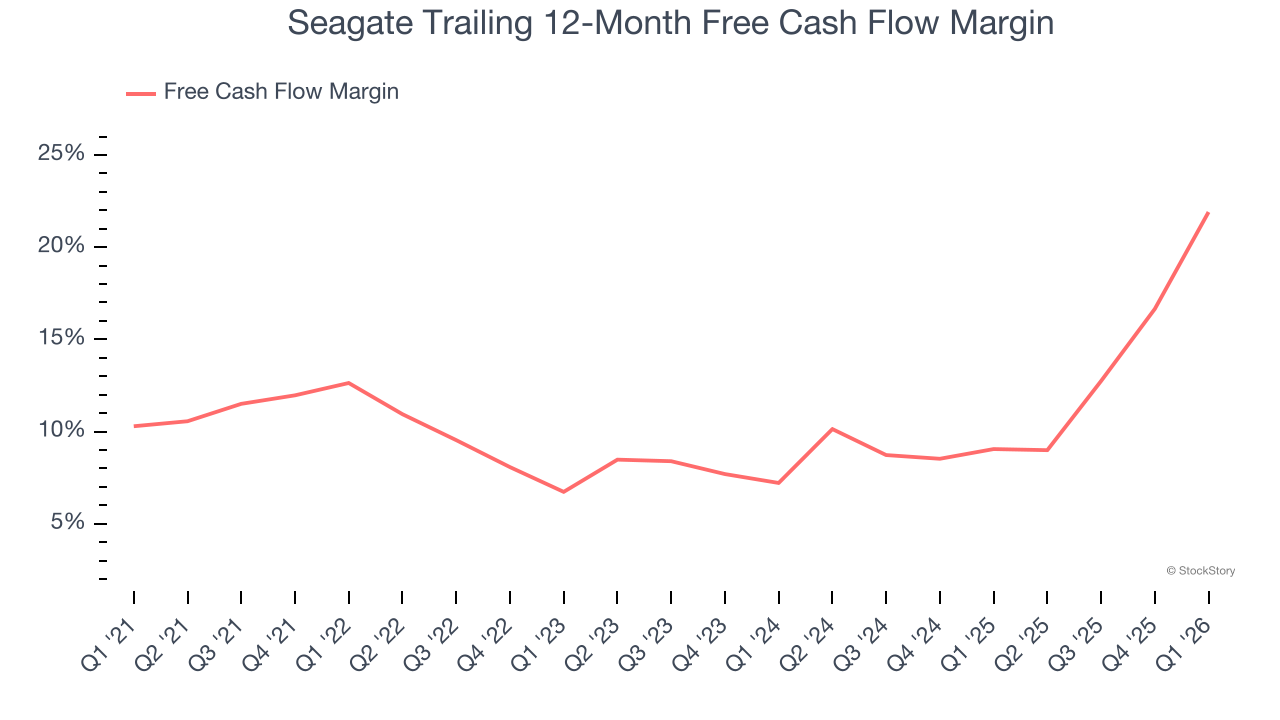

3. Increasing Free Cash Flow Margin Juices Financials

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Seagate’s margin expanded by 9.3 percentage points over the last five years. We have no doubt shareholders would like to continue seeing its cash conversion rise as it gives the company more optionality. Seagate’s free cash flow margin for the trailing 12 months was 21.9%.

Final Judgment

These are just a few reasons why Seagate ranks highly on our list, and after the recent rally, the stock trades at 42.5× forward P/E (or $901.50 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.