With the war in the Middle East and oil prices climbing, it looks less likely that the Fed will cut rates anytime soon. But it’s not always going to be like this forever. Once tensions ease and the balance of risks shifts from inflation to something a little more “normal”, rate cuts may become more likely.

If and when that shift happens, borrowing becomes easier, and money cycles out of some sectors into others. One of the biggest beneficiaries of that kind of change is real estate, and REITs look more attractive.

However, there are over 225 REITs that are traded publicly in the United States. Some of them are better than others, for reasons that may not be as obvious. Two of the most well-known in investing circles are Realty Income and VICI Properties.

But which one’s better as a long-term bet? Let’s find out.

What are REITs?

Real estate investment trusts, or REITs, are companies that own and manage income-producing properties. They generate revenue mainly from rent and are required to distribute at least 90% of their taxable income to shareholders as dividends. That’s why they tend to attract dividend investors. The combination of reliably consistent cash flow and high yields makes them great additions to long-term portfolios.

Company profiles

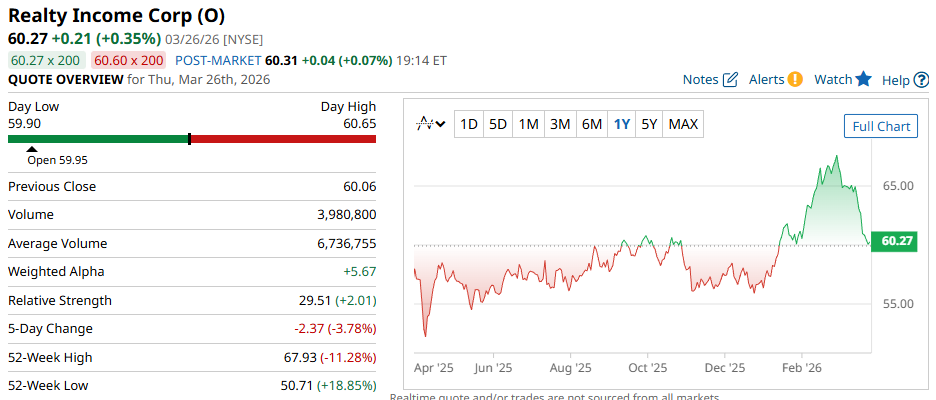

First up is Realty Income, or better known as the “monthly dividend company.”

The REIT focuses on leasing to retail and commercial clients, and its portfolio comprises grocery and convenience stores, home improvement centers, dollar stores, fast-food chains, drug stores, restaurants, and general merchandise stores.

As of its Q4 ‘25 filing on February 24, 2026, the REIT “owns or holds interests in 15,511 properties, leased to 1,761 clients across 92 industries.”

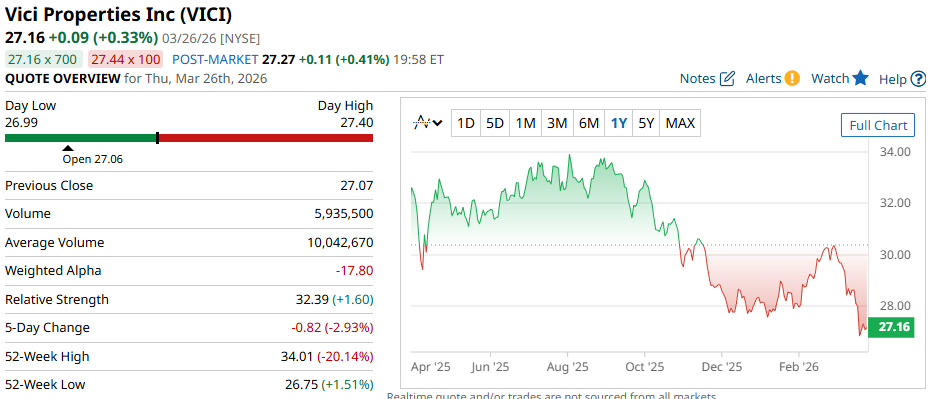

On the other hand, VICI Properties is an “experiential” REIT that focuses on sports and gaming facilities, resorts, restaurants, and other similar properties.

Some of its properties include Caesars Palace, The Venetian Resort, the MGM Grand, and the Chelsea Piers.

As of its Q4 financials, VICI owns “93 experiential assets, made up of 54 gaming properties and 39 other experiential properties across the U.S. and Canada.”

Based on that alone, Realty Income has a more diversified portfolio of properties. Also, its tenants tend to operate in more resilient, “staple” sectors that aren’t overly sensitive to major economic cycles.

Meanwhile, VICI’s more concentrated property ownership puts it more at odds with economic cycles tied to tourism and discretionary spending.

On the surface, VICI appears to be the riskier REIT.

But is it, really?

Business model comparison

VICI Properties primarily operates as a REIT providing triple-net leases (NNN). It's important because the tenants pay for property taxes, building insurance, and maintenance and repairs- things that landlords usually cover. The result? Lease payments are received net of taxes, insurance, and maintenance. Hence, the triple net lease.

With this structure, rent income is more predictable, and there are fewer unexpected expenses, such as sudden, massive repairs. However, triple-net leases also deepen VICI’s dependence on the client’s business health. If a client experiences financial distress, VICI may face rent renegotiations, depending on how ironclad its contracts are. Worst comes to worst, sector-wide issues may hit multiple tenants at once.

Now, Realty Income operates much in the same way and faces the same risks. But the difference is is that Realty Income has a far more diversified portfolio, so industry-wide setbacks won’t likely affect it as much.

Financial comparison

So, how are these two businesses doing? Let’s look at quick financial metrics for the full year of 2025.

| Metric | Realty Income (O) | VICI Properties (VICI) |

| Revenue | $5.75 B | $4.0 B |

| Net income | $1.06 B | $2.8 B |

| FFO per share | $4.25 | $2.61 |

| AFFO per share | $4.28 | $2.38 |

By revenue, Realty Income is larger, and based on net income, VICI Properties is more profitable.

However, REITs don’t operate the same way as other companies. Standard accounting practices always involve depreciation of property. And when your business is purely property leasing, reported earnings can look lower than the cash the properties are actually generating,

That’s why, when considering them for dividend portfolios, funds from operations, or FFO, is a good place to start.

Funds from operations, or FFO, is a metric that helps investors evaluate a company’s underlying operating performance. That said, FFO isn’t a measure of cash flow, which is why many investors focus more closely on adjusted FFO when assessing dividend sustainability. Higher AFFO can generally suggest higher dividends in the future.

And here, we can see that Realty Income earns over 60% more AFFO than VICI Properties.

Dividend comparison

So let’s see how the differing AFFO numbers affect their dividends. I’ll be using last year’s dividend data, since REIT payouts can fluctuate.

Over the last 12 months, Realty Income paid $3.23 per share in dividends, yielding around 5.36%. It’s also been a member of the Dividend Aristocrat list since 2020 and has increased its payouts for 31 straight years. And finally, Realty Income's dividend payouts have grown 25% in the last five years.

Meanwhile, VICI Properties paid $1.78 per share last year, translating to a 6.59% yield. VICI also increased its dividends for 7 straight years, and its payouts have grown by 40% over the last 5 years.

Verdict

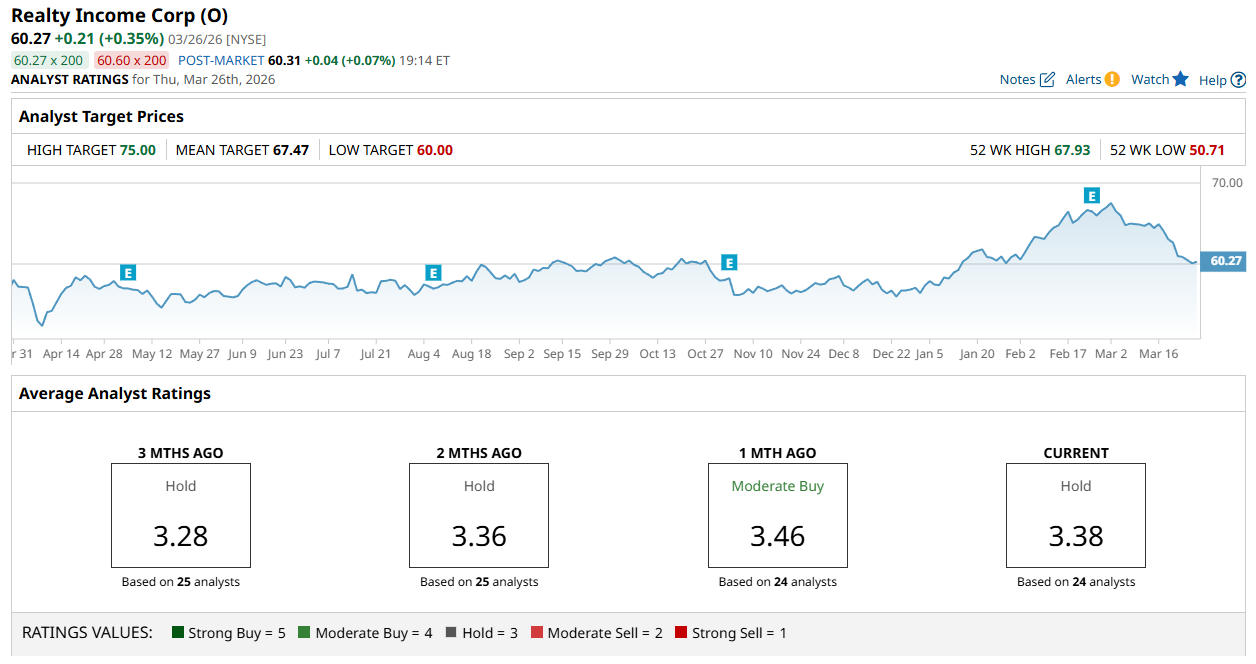

Today, a consensus among 24 Wall Street analysts rate Realty Income a Hold, with an average score of 3.38 out of five. The mean price target is $67.47, and the high price target is $75, suggesting as much as 24% upside over the next year.

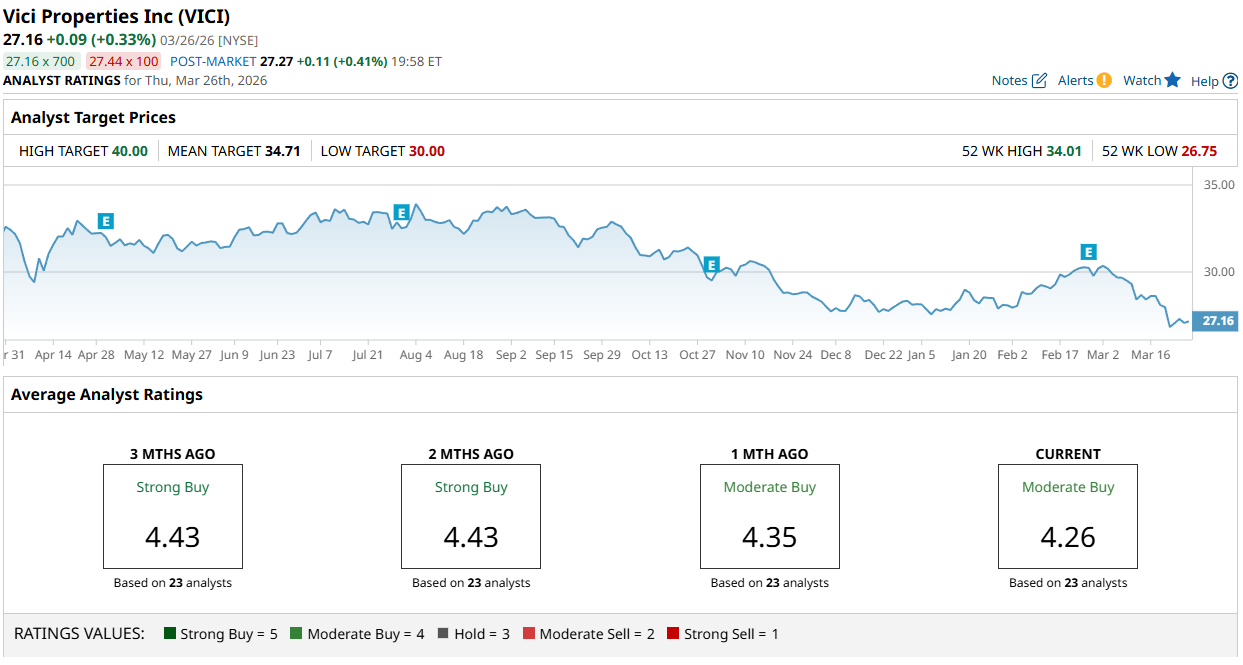

Meanwhile, a consensus among 23 analysts rate VICI Property a Moderate Buy with an average score of 4.26. The mean price target is $34.71, while the high price target is $40, suggesting VICI stock could surge as much as 47% over the next year.

Overall, VICI looks more attractive based on analyst sentiment, yield, and five-year growth. That said, Realty Income has a longer history of dividend growth and could prove more resilient in a rate-cut environment, as its larger scale and broader diversification may make it a steadier beneficiary of lower rates.

On the date of publication, Rick Orford did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Only 1 of These Top 2 REITs Is Built to Pay You for Generations

- Exxon Mobil Is Now More Expensive Than Nvidia Stock. What Gives, and How Should You Play XOM Here?

- 1 Dividend Stock to Buy Now to Bet on AI Data Centers

- The General Mills Dividend Yields 6.53%. Is That Enough to Make Up for an Oil Price Shock?