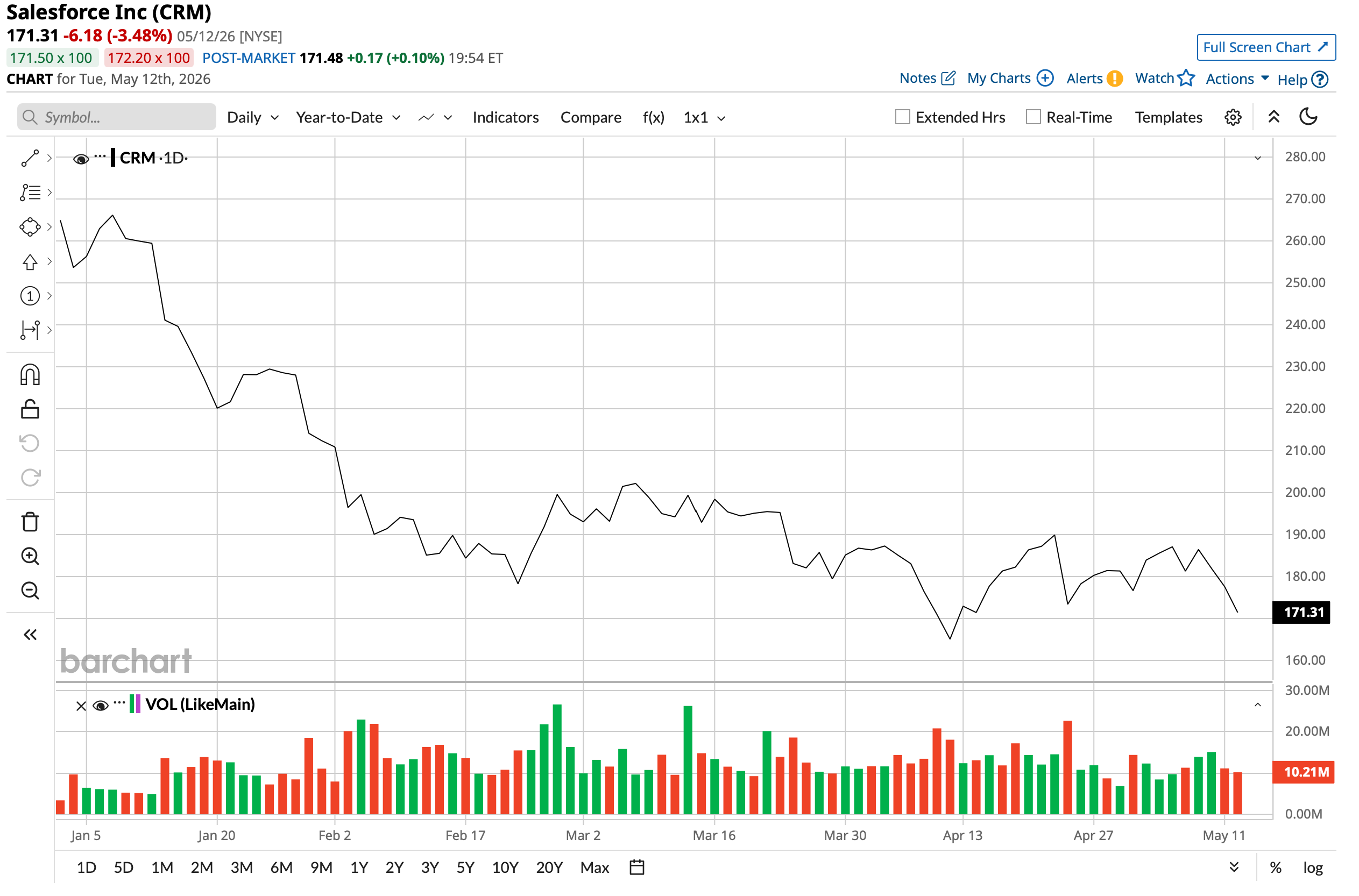

One of the biggest casualties of the “SaaSpocalypse” trend has undoubtedly been Marc Benioff-led Salesforce (CRM). Perceived to be rendered irrelevant by the likes of Claude Code and OpenAI's Codex, shares of Salesforce have been on a downward spiral ever since. Benioff's impassioned defense has not been able to salvage the company from the rout in the markets as well.

Thus, the Q1 fiscal year 2027 results on May 27 could not come at a better time. The company has been consistently outperforming Street expectations, and with its pivot toward becoming an agentic AI enterprise, will the good times finally roll in for Salesforce? Let's find out.

Q4 Double Beat

Naysayers of Salesforce may have to change their opinions if they happen to pore over the company's financials, which have never been at a better place. And Q4 2026 was a stark reminder of that.

Total revenue for the quarter increased by 12.1% from the previous year to $11.2 billion, headlined by a 13.2% rise in subscription revenues to $10.7 billion. The growth in overall revenue was accompanied by a healthy uptick in both current remaining performance obligations (RPO) and total RPO. While the former is an indicator of demand in the short term, the latter gives us an idea about the demand for the longer term.

Notably, current RPO was up 16% on a YoY basis to $35.1 billion, and total RPO increased by 14% in the same period to $72.4 billion.

Subsequently, this flowed into the bottom line as the company reported an EPS of $3.81 in Q4 2026, up 37.1% from the prior year. This was comfortably above the consensus estimate of $3.05 per share. Notably, this was the fifth consecutive quarter of earnings beat from the company. Yet, the stock is still down 35.3% on a YTD basis.

For Q1 fiscal 2027, the Street is expecting Salesforce to report revenue and earnings of $11.06 billion and $3.12 per share. Meanwhile, the company's forecasts for the same in Q1 2027 are between $11.03 billion and $11.08 billion for revenues and between $3.11 and $3.13 per share for earnings.

Net cash from operating activities for the quarter grew to $5.5 billion from about $4 billion in the year-ago period. Overall, Salesforce closed Q4 2026 with a cash balance of $7.3 billion, which was higher than its short-term debt levels of $4 billion.

Further, in terms of shareholder activities, the company not only authorized a $50 billion share repurchase program, it also increased its dividend by 5.8% from the prior year to $0.44 per share.

Additionally, CRM stock is trading at undervalued levels as well. Its forward P/E, P/S, and P/CF of 13.44x, 3.15x, and 9.98x are all below the sector medians of 24.85x, 3.39x, and 18.77x, respectively.

Where Is CRM Really?

Salesforce's financials and order book signals that it remains a meaningful player in the current AI revolution. The question is for how long and what is it doing to stay there?

Well, to that end, Salesforce has thrown its full weight behind an AI-driven transformation of its core business, with Agentforce and Data 360 sitting at the center of that effort. The results are beginning to show up in the numbers, with the company posting $2.9 billion in annual recurring revenue from these initiatives, a figure that represents 200% growth on a year-over-year basis. Alongside this, the company has been deliberately repositioning its commercial model away from pure subscription arrangements and toward a hybrid structure that blends subscription with consumption-based pricing, a shift designed to meet the demands of an AI native competitive landscape.

Notably, Agentforce deserves particular attention within this story. The platform gives customers the ability to construct and deploy a workforce of digital agents capable of operating continuously without the constraints that apply to human labor, serving both employees and end customers across a wide range of productivity use cases. Within the service context specifically, Agentforce brings customer onboarding, employee support, IT management, and field service operations onto a single AI-powered platform, enabling organizations to deliver tailored support experiences at a scale that would otherwise be operationally prohibitive.

Data 360 complements this by functioning as a universal integration layer. Regardless of where an organization's data currently resides, it can be pulled into Data 360 and harmonized into a coherent whole. That capability raises switching costs, because the effort required to replicate that integration elsewhere grows with every data source added. Further, the company's decision to pivot toward agentic AI as early as 2024 also gave it a head start that competitors are still working to close, allowing existing customers to transition into the agentic paradigm without leaving the Salesforce ecosystem.

The market position underpinning all of this is formidable. Salesforce commands roughly 21% of the global CRM market, a share that is more than four times that of its closest rival. Close to half of the Fortune 100 are already running both its AI and Data Cloud products, giving it a structural advantage.

Then, rounding out the platform's enterprise credibility is the Trust Layer, a governance and data isolation framework that allows large organizations to deploy generative AI capabilities without the risk of their proprietary information finding its way into external model training pipelines. For regulated industries and enterprises, that assurance is critical.

On the acquisition front, Salesforce has added meaningful depth to this picture. The $8 billion purchase of Informatica, completed in November 2025, brought an AI-powered enterprise cloud data management platform into the fold, giving customers the ability to break down data silos and funnel consolidated information into Agentforce's Data 360 engine while preserving compliance and security standards.

Meanwhile, Salesforce is also moving with urgency to deepen its vertical cloud offerings, with life sciences, public sector, and financial services drawing the most concentrated attention. The appeal of these segments lies in their unit economics, where contract values tend to run higher, customer retention rates are more favorable, and the overall profile is considerably more attractive than what general-purpose CRM typically delivers.

That said, the competitive environment Salesforce is operating in carries real risks. Beyond the pressure coming from newer AI native entrants, including Anthropic's Claude, the company faces an established and deeply entrenched challenger in Microsoft (MSFT). Its Dynamics 365 and the broader Copilot ecosystem carry a built-in advantage in any account where Office 365 is already woven into daily operations, because technology buyers frequently prefer deepening a relationship with a known vendor over introducing an additional one. Microsoft's adoption of Copilot faced its own friction points during 2025, but the distribution infrastructure and existing customer trust that Microsoft brings to bear represent a competitive force that Salesforce cannot afford to treat lightly.

Analyst Opinion on CRM Stock

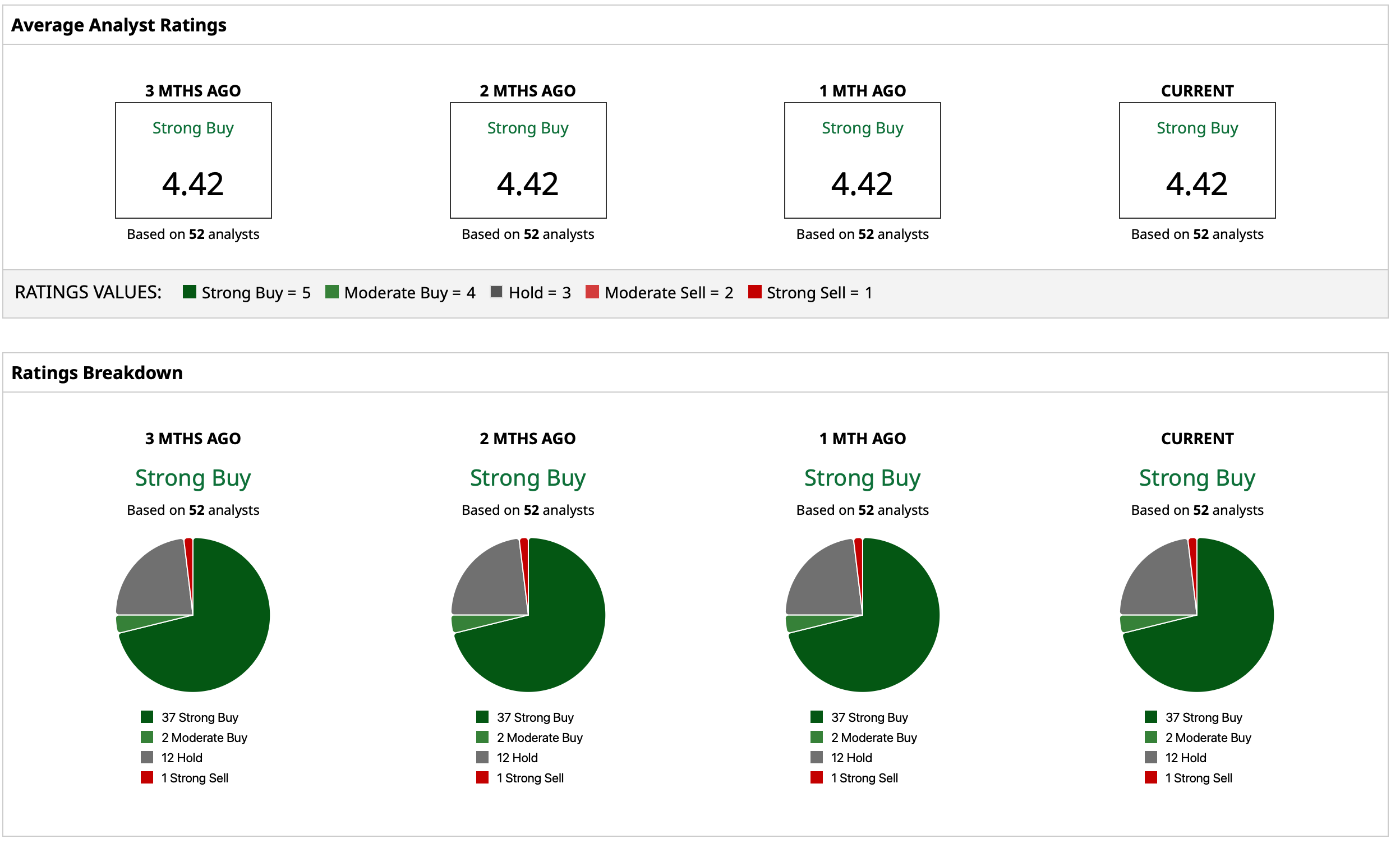

Thus, analysts have attributed to CRM stock an overall rating of “Strong Buy,” with a mean target price of $276.43, which indicates an upside potential of about 61.4% from recent levels. Out of 52 analysts covering the stock, 37 have a “Strong Buy” rating, two have a “Moderate Buy” rating, 12 have a “Hold” rating, and one has a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Cisco (CSCO) Stock Just Hit a Record High Amid Layoffs Announcement

- Ukraine Will Leverage Palantir’s AI Capabilities In Its War With Russia. This Helps Prove PLTR Stock Will Never Be Irrelevant.

- 2 Reasons Quantum Cyber Has More Than Doubled Today

- BA Stock Watch: Boeing May Get a Big Boost From Trump-Xi Summit