Super Micro Computer (SMCI) reported superb fiscal third-quarter financial results on May 5, at least on the surface. Digging deeper, SMCI stock is still well below its 52-week and all-time highs. By far the biggest reason for the shares' inability to come close to regaining its former status is the company's multiple scandals and alleged accounting violations.

These incidents make SMCI stock uninvestable because it's impossible to know when another scandal, accounting irregularity, or probe of the firm will materialize, which could cause SMCI stock to suddenly tumble tremendously. Additionally, it's difficult to rely fully on the accuracy of its financial results.

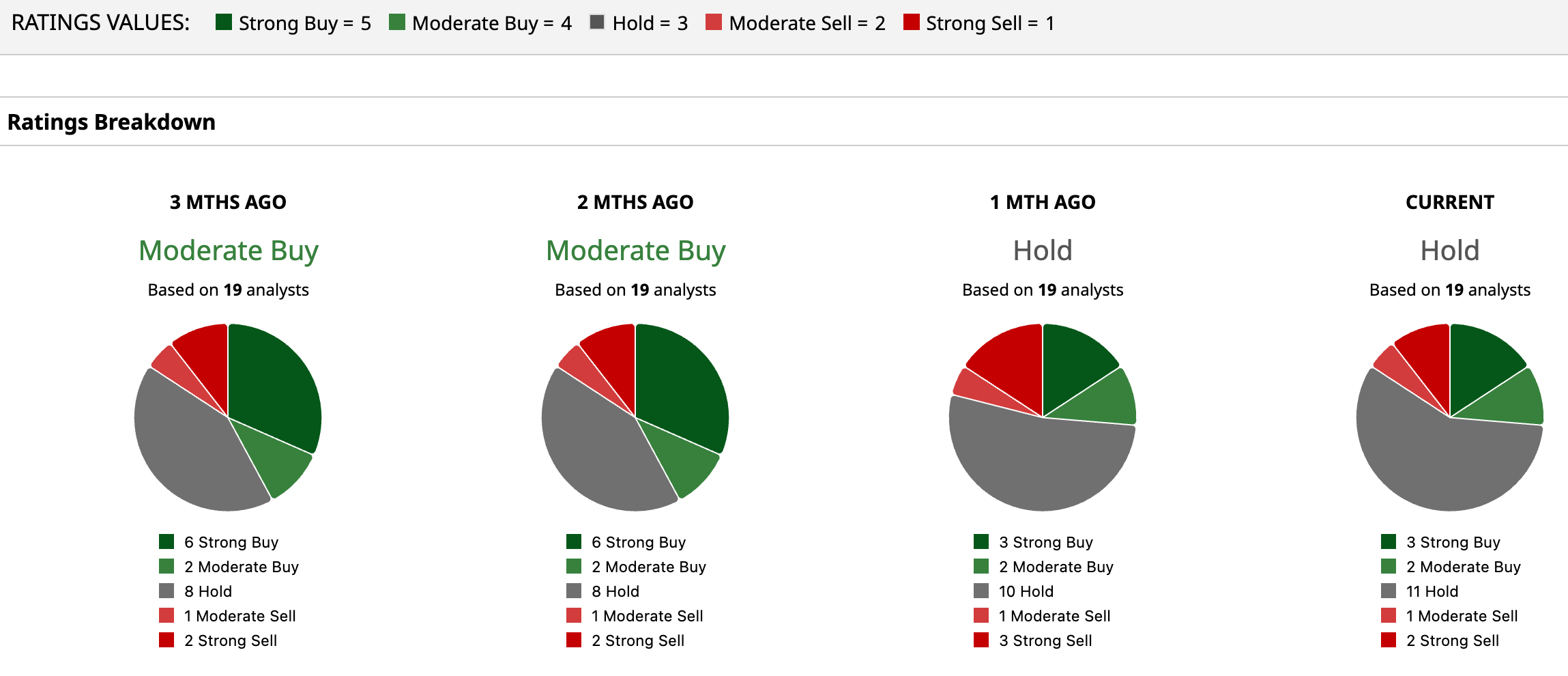

Indeed, multiple Wall Street analysts cite the company's “corporate governance” issues as a reason to avoid buying the name.

In light of these points, investors should not ownSMCI stock.

About Super Micro Computer

Based in California, Super Micro develops server and storage products, including those used in many data centers. It carries a market capitalization of $20.76 billion and a trailing price-to-earnings ratio of 15.38 times.

SMCI's Fiscal Q3 Results and the Stock's Performance

The company's revenue jumped to $10.24 billion in Q3, far above the $4.6 billion of sales that it generated during the same period a year earlier. Further, its earnings per share soared to $0.81 versus $0.18 year-over-year (YOY).

In the wake of the results, which were released on May 5 after market close, the shares jumped 24.54% to $34.66 on May 6. However, the name remains 46% below its 52-week high of $62.36 and much further below its all-time, split-adjusted high of $120.90, set in March 2024. Moreover, the shares have risen just 2.06% in the last 12 months.

Examples of SMCI's “Governance” Problems and Analysts' View of the Issue

In March, one of SMCI's executives and two other company employees were indicted for smuggling AI-related products to China in violation of U.S. rules related to the export of such products to the Asian country. SMCI's board is probing export-rule violations by its former employees. SMCI's accounting practices were reportedly investigated by the U.S. Department of Justice after a whistleblower accused it of accounting irregularities. Its former auditor, Ernst & Young, resigned due to alleged problems with the company's internal controls, and Super Micro was accused by a short-selling firm of accounting improprieties and violations of U.S. export rules. On the day after the March accusations were unveiled, the company announced it would be delayed in issuing its annual 10-K report that is required by the SEC.

JPMorgan's Samik Chatterjee., Wedbush's Matt Bryson, and GF Securities' Evan Lee all kept “Neutral” or “Hold” ratings on the shares in the wake of the company's latest quarterly results, and all cited its compliance issues as one reason for their reluctance to become more constructive on the shares.

Valuation and the Bottom Line on SMCI Stock

Although the shares have a very low forward price-to-earnings ratio of 15.38 times, the company's persistent compliance issues make its shares unattractive for the time being.

On the date of publication, Larry Ramer did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Western Digital Just Increased Its Dividend by 20% but It’s Still Not a Yield Play

- Don’t Trust This Top-Heavy Stock Market, Hedge It. Here’s Your Roadmap.

- CHRN Stock Just Started Trading as Applied Digital Spins Off ChronoScale. How to Play Shares Here.

- If You Are Bullish on Agentic AI, Western Digital Is a Top Stock to Buy