As the Q3 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the testing & diagnostics services industry, including RadNet (NASDAQ: RDNT) and its peers.

The testing and diagnostics services industry plays a crucial role in disease detection, monitoring, and prevention, serving hospitals, clinics, and individual consumers. This sector benefits from stable demand, driven by an aging population, increased prevalence of chronic diseases, and growing awareness of preventive healthcare. Recurring revenue streams come from routine screenings, lab tests, and diagnostic imaging, with reimbursement from Medicare, Medicaid, private insurance, and out-of-pocket payments. However, the industry faces challenges such as pricing pressures, regulatory compliance, and the need for continuous investment in new testing technologies. Looking ahead, industry tailwinds include the expansion of personalized medicine, increased adoption of at-home and rapid diagnostic tests, and advancements in AI-driven diagnostics that enhance accuracy and efficiency. However, headwinds such as reimbursement uncertainties, competition from decentralized testing solutions, and regulatory scrutiny over test validity and cost-effectiveness may impact profitability. Adapting to evolving healthcare models and integrating automation will be key for sustaining growth and maintaining operational efficiency.

The 5 testing & diagnostics services stocks we track reported a very strong Q3. As a group, revenues beat analysts’ consensus estimates by 4.9%.

Thankfully, share prices of the companies have been resilient as they are up 8.8% on average since the latest earnings results.

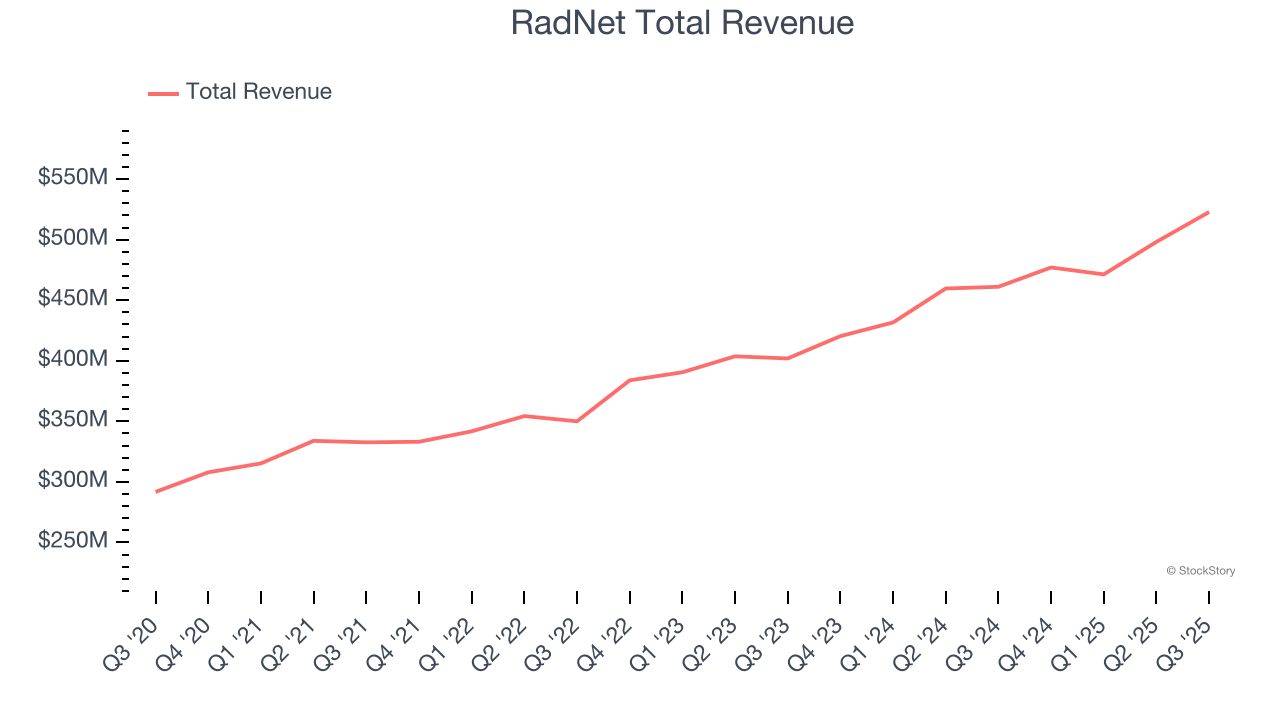

RadNet (NASDAQ: RDNT)

With over 350 imaging facilities across seven states and a growing artificial intelligence division, RadNet (NASDAQ: RDNT) operates a network of outpatient diagnostic imaging centers across the United States, offering services like MRI, CT scans, PET scans, mammography, and X-rays.

RadNet reported revenues of $522.9 million, up 13.4% year on year. This print exceeded analysts’ expectations by 6.3%. Overall, it was a strong quarter for the company with a solid beat of analysts’ same-store sales estimates and an impressive beat of analysts’ revenue estimates.

Dr. Howard Berger, President and Chief Executive Officer of RadNet, commented, “The business continues to demonstrate strong growth and record results in each of the Imaging Center and Digital Health reportable operating segments. Total Company Revenue grew 13.4% and Adjusted EBITDA(1) grew 15.2% as compared with last year’s third quarter, resulting in Adjusted EBITDA(1) margin expansion of 26 basis points. Contributing to the achievement of these results were the continued focus on creating capacity at existing centers, new center openings, ongoing business mix shift towards advanced imaging, tuck-in acquisitions, increased reimbursement from commercial and capitated payors, the expansion of health system joint ventures and an acceleration of Digital Health Revenue growth.”

The market was likely pricing in the results, and the stock is flat since reporting. It currently trades at $78.54.

Is now the time to buy RadNet? Access our full analysis of the earnings results here, it’s free for active Edge members.

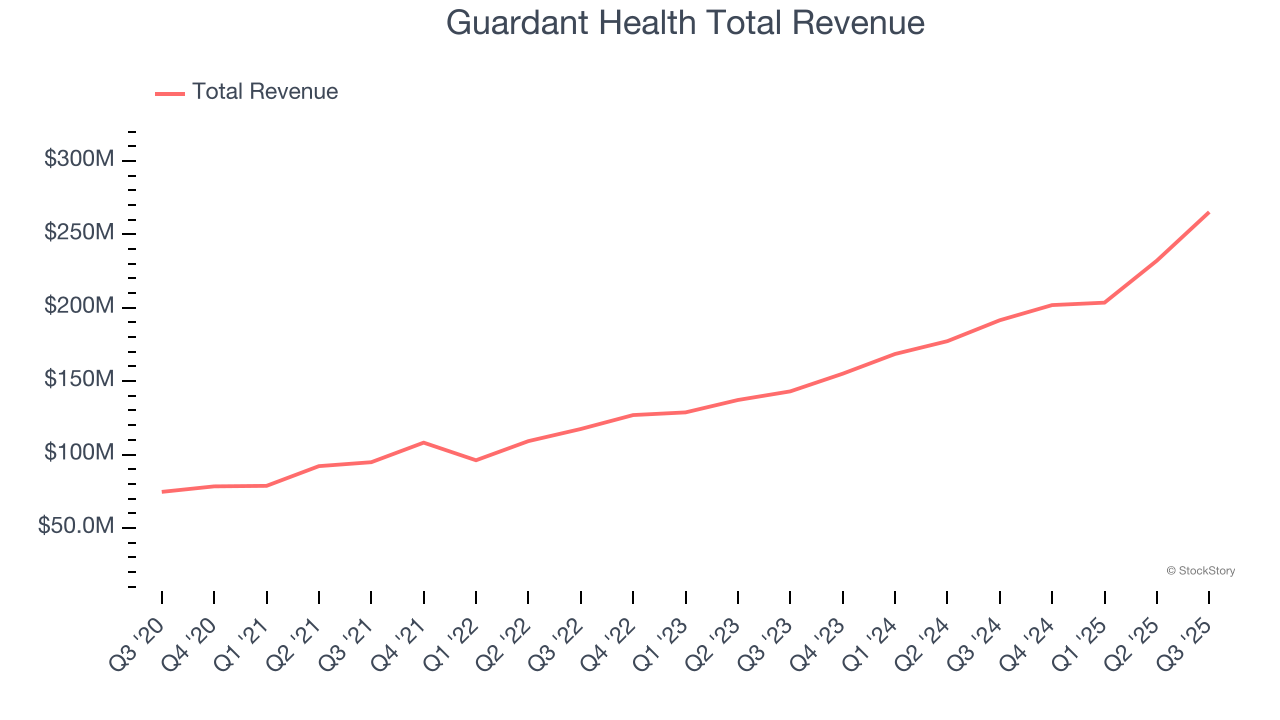

Best Q3: Guardant Health (NASDAQ: GH)

Pioneering the field of "liquid biopsy" with technology that can identify cancer-specific genetic mutations from a simple blood draw, Guardant Health (NASDAQ: GH) develops blood tests that detect and monitor cancer by analyzing tumor DNA in the bloodstream, helping doctors make treatment decisions without invasive biopsies.

Guardant Health reported revenues of $265.2 million, up 38.5% year on year, outperforming analysts’ expectations by 12.6%. The business had an incredible quarter with a solid beat of analysts’ revenue estimates and full-year revenue guidance exceeding analysts’ expectations.

Guardant Health pulled off the biggest analyst estimates beat and fastest revenue growth among its peers. The market seems happy with the results as the stock is up 40.6% since reporting. It currently trades at $101.61.

Is now the time to buy Guardant Health? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: Labcorp (NYSE: LH)

With over 600 million tests performed annually and involvement in 90% of FDA-approved drugs in 2023, Labcorp (NYSE: LH) provides laboratory testing services and drug development solutions to doctors, hospitals, pharmaceutical companies, and patients worldwide.

Labcorp reported revenues of $3.56 billion, up 8.6% year on year, in line with analysts’ expectations. It was a mixed quarter as it posted a narrow beat of analysts’ organic revenue estimates.

Labcorp delivered the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 6.3% since the results and currently trades at $258.38.

Read our full analysis of Labcorp’s results here.

NeoGenomics (NASDAQ: NEO)

Operating a network of CAP-accredited and CLIA-certified laboratories across the United States and United Kingdom, NeoGenomics (NASDAQ: NEO) provides specialized cancer diagnostic testing services, including genetic analysis, molecular testing, and pathology consultation for oncologists and healthcare providers.

NeoGenomics reported revenues of $187.8 million, up 11.9% year on year. This print topped analysts’ expectations by 2.1%. Overall, it was a strong quarter as it also logged EPS in line with analysts’ estimates and an impressive beat of analysts’ revenue estimates.

NeoGenomics had the weakest full-year guidance update among its peers. The stock is up 13.3% since reporting and currently trades at $11.90.

Read our full, actionable report on NeoGenomics here, it’s free for active Edge members.

Quest (NYSE: DGX)

Processing approximately one-third of the adult U.S. population's lab tests annually, Quest Diagnostics (NYSE: DGX) provides laboratory testing and diagnostic information services to patients, physicians, hospitals, and other healthcare providers across the United States.

Quest reported revenues of $2.82 billion, up 13.2% year on year. This result surpassed analysts’ expectations by 3.3%. It was a strong quarter as it also put up an impressive beat of analysts’ revenue estimates and full-year revenue guidance slightly topping analysts’ expectations.

Quest delivered the highest full-year guidance raise among its peers. The stock is down 4.1% since reporting and currently trades at $182.54.

Read our full, actionable report on Quest here, it’s free for active Edge members.

Market Update

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.