Earnings results often indicate what direction a company will take in the months ahead. With Q2 behind us, let’s have a look at BWX (NYSE: BWXT) and its peers.

Defense contractors typically require technical expertise and government clearance. Companies in this sector can also enjoy long-term contracts with government bodies, leading to more predictable revenues. Combined, these factors create high barriers to entry and can lead to limited competition. Lately, geopolitical tensions–whether it be Russia’s invasion of Ukraine or China’s aggression towards Taiwan–highlight the need for defense spending. On the other hand, demand for these products can ebb and flow with defense budgets and even who is president, as different administrations can have vastly different ideas of how to allocate federal funds.

The 13 defense contractors stocks we track reported a strong Q2. As a group, revenues beat analysts’ consensus estimates by 3.4% while next quarter’s revenue guidance was 0.6% below.

Thankfully, share prices of the companies have been resilient as they are up 7% on average since the latest earnings results.

BWX (NYSE: BWXT)

Contributing components and materials to the famous Manhattan Project in the 1940s, BWX (NYSE: BWXT) is a manufacturer and service provider of nuclear components and fuel for government and commercial industries.

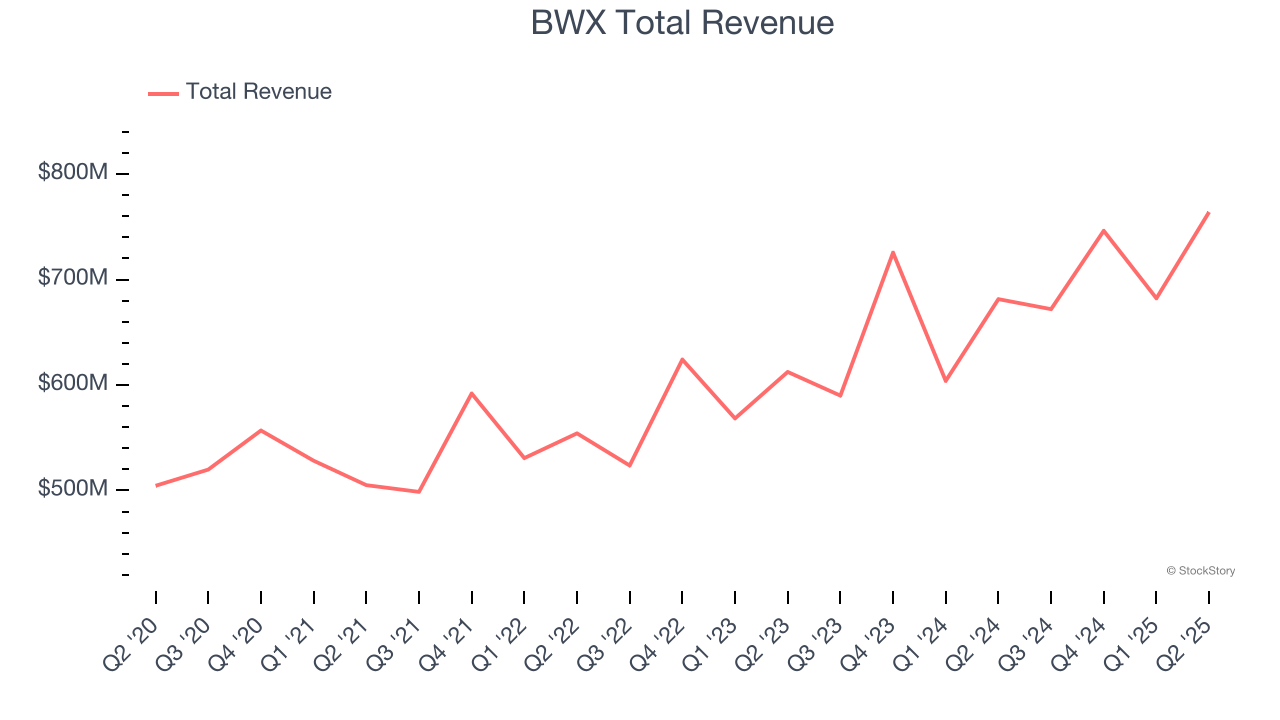

BWX reported revenues of $764 million, up 12.1% year on year. This print exceeded analysts’ expectations by 7.2%. Overall, it was a stunning quarter for the company with a beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

“We had exceptionally strong second quarter 2025 financial results driven by solid operational performance and pacing of work, particularly in Government Operations, which was complemented by robust bookings in both segments, leading to record backlog,” said Rex D. Geveden, president and chief executive officer.

BWX achieved the highest full-year guidance raise of the whole group. Unsurprisingly, the stock is up 16.2% since reporting and currently trades at $179.54.

Is now the time to buy BWX? Access our full analysis of the earnings results here, it’s free.

Best Q2: Mercury Systems (NASDAQ: MRCY)

Founded in 1981, Mercury Systems (NASDAQ: MRCY) specializes in providing processing subsystems and components for primarily defense applications.

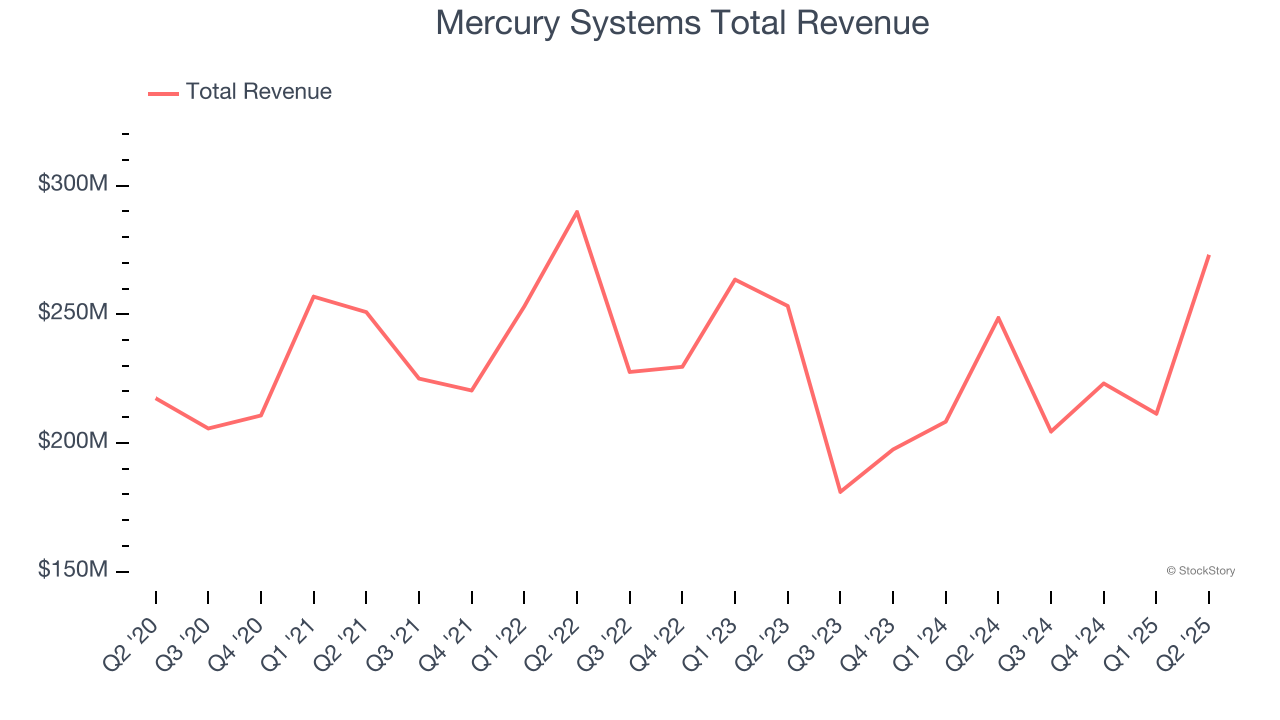

Mercury Systems reported revenues of $273.1 million, up 9.9% year on year, outperforming analysts’ expectations by 11.9%. The business had an incredible quarter with an impressive beat of analysts’ organic revenue estimates and a beat of analysts’ EPS estimates.

The market seems happy with the results as the stock is up 26.6% since reporting. It currently trades at $68.

Is now the time to buy Mercury Systems? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: Lockheed Martin (NYSE: LMT)

Headquartered in Maryland, Famous for the F-35 aircraft, Lockheed Martin (NYSE: LMT) specializes in defense, space, homeland security, and information technology products.

Lockheed Martin reported revenues of $18.16 billion, flat year on year, falling short of analysts’ expectations by 2.3%. It was a softer quarter as it posted full-year EPS guidance missing analysts’ expectations significantly and a significant miss of analysts’ adjusted operating income estimates.

As expected, the stock is down 6.6% since the results and currently trades at $431.

Read our full analysis of Lockheed Martin’s results here.

General Dynamics (NYSE: GD)

Creator of the famous M1 Abrahms tank, General Dynamics (NYSE: GD) develops aerospace, marine systems, combat systems, and information technology products.

General Dynamics reported revenues of $13.04 billion, up 8.9% year on year. This result surpassed analysts’ expectations by 5.7%. It was an exceptional quarter as it also logged a solid beat of analysts’ backlog estimates and a solid beat of analysts’ adjusted operating income estimates.

The stock is up 5.7% since reporting and currently trades at $314.17.

Read our full, actionable report on General Dynamics here, it’s free.

Parsons (NYSE: PSN)

Delivering aerospace technology during the Cold War-era, Parsons (NYSE: PSN) offers engineering, construction, and cybersecurity solutions for the infrastructure and defense sectors.

Parsons reported revenues of $1.58 billion, down 5.2% year on year. This print lagged analysts' expectations by 0.9%. Aside from that, it was a mixed quarter as it also produced an impressive beat of analysts’ adjusted operating income estimates but a slight miss of analysts’ backlog estimates.

Parsons had the slowest revenue growth among its peers. The stock is up 3.9% since reporting and currently trades at $80.01.

Read our full, actionable report on Parsons here, it’s free.

Market Update

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.