Even during a down period for the markets, Novanta has gone against the grain, climbing to $118.13. Its shares have yielded a 17.2% return over the last six months, beating the S&P 500 by 22.6%. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Novanta, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Novanta Not Exciting?

Despite the momentum, we don't have much confidence in Novanta. Here are three reasons you should be careful with NOVT and a stock we'd rather own.

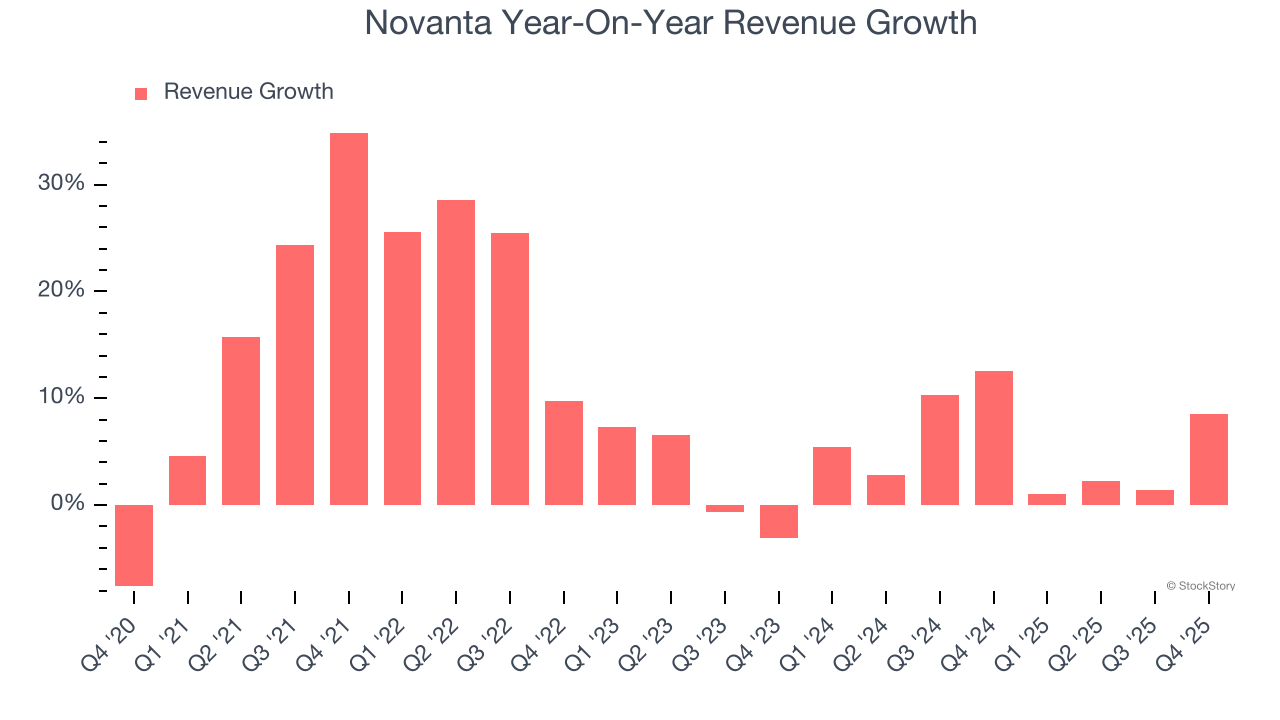

1. Lackluster Revenue Growth

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Novanta’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 5.5% over the last two years was well below its five-year trend.

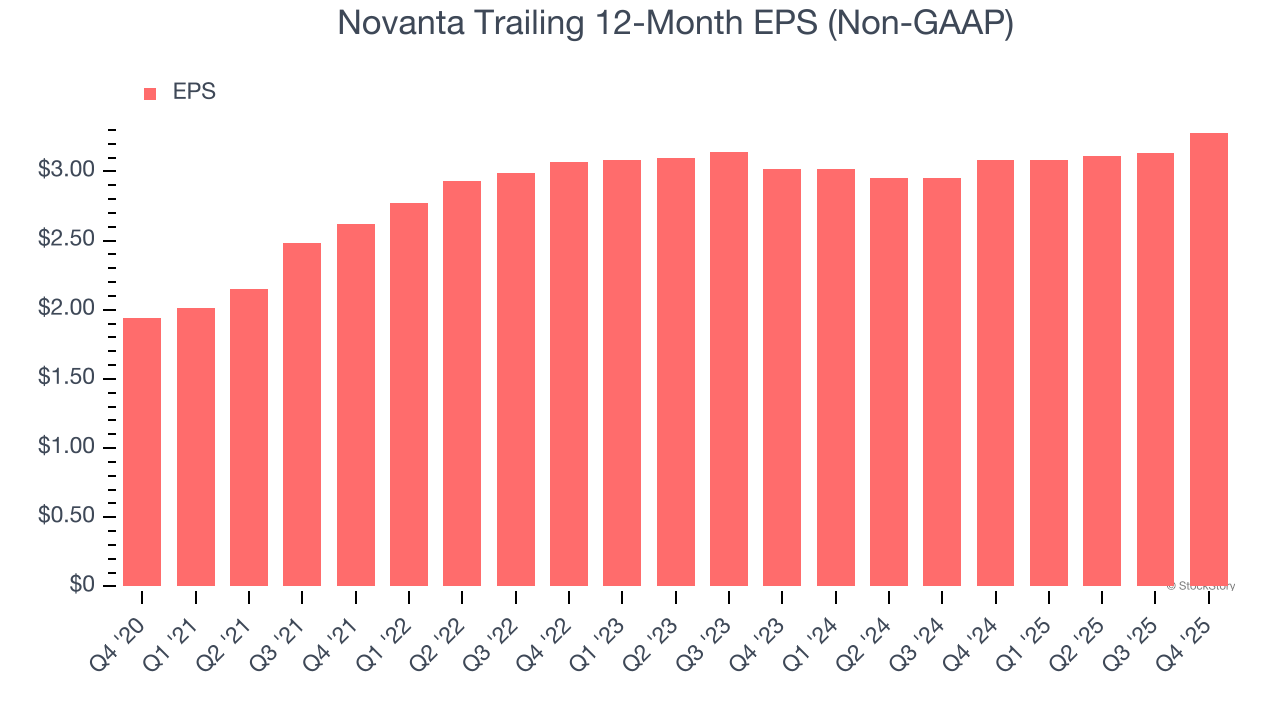

2. Recent EPS Growth Below Our Standards

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Novanta’s unimpressive 4.2% annual EPS growth over the last two years aligns with its revenue trend. This tells us it maintained its per-share profitability as it expanded.

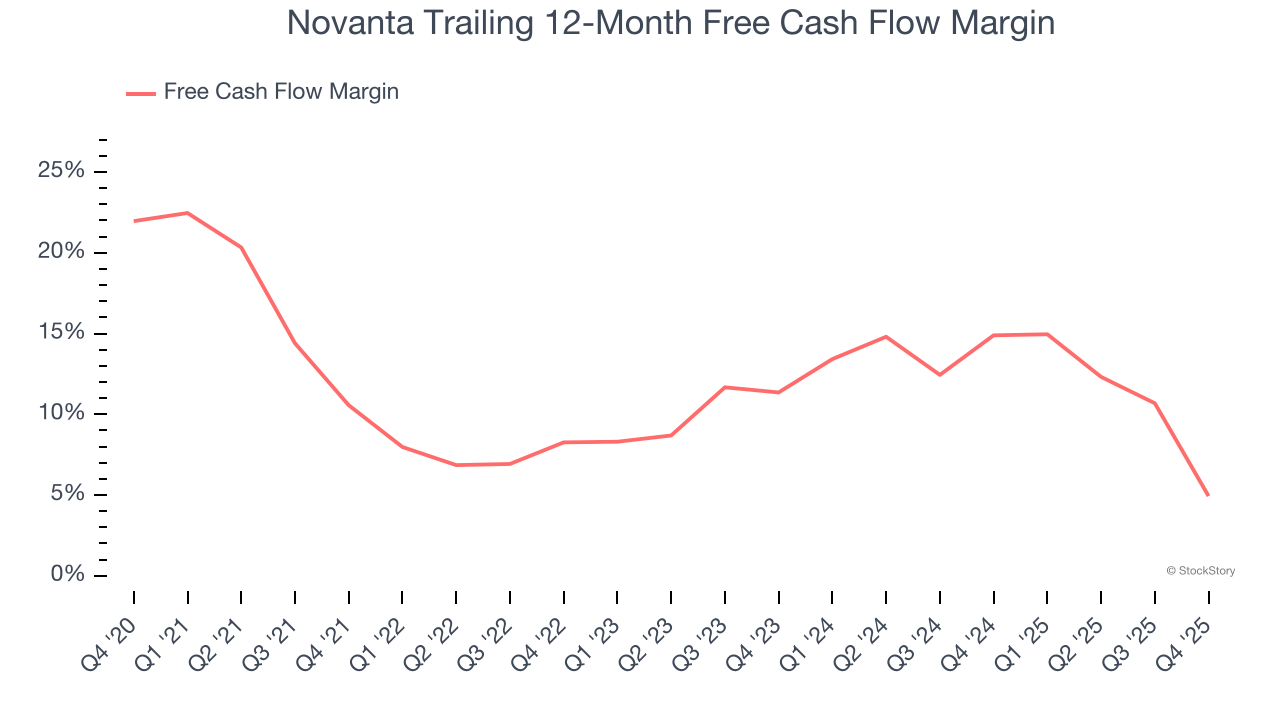

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Novanta’s margin dropped by 5.6 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Novanta’s free cash flow margin for the trailing 12 months was 4.9%.

Final Judgment

Novanta isn’t a terrible business, but it doesn’t pass our bar. With its shares outperforming the market lately, the stock trades at 31.8× forward P/E (or $118.13 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. Let us point you toward a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Would Buy Instead of Novanta

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.