Uniform rental provider Vestis Corporation (NYSE: VSTS) reported Q1 CY2026 results beating Wall Street’s revenue expectations, but sales were flat year on year at $659.4 million. Its GAAP profit of $0.02 per share was in line with analysts’ consensus estimates.

Is now the time to buy Vestis? Find out by accessing our full research report, it’s free.

Vestis (VSTS) Q1 CY2026 Highlights:

- Turnaround plan: "The Company previously estimated approximately $40 million of in-year benefit to fiscal 2026 from the Plan, but the Company now estimates approximately $50 million of in-year benefit to fiscal 2026, with

roughly $15 million already realized" - Revenue: $659.4 million vs analyst estimates of $654.9 million (flat year on year, 0.7% beat)

- EPS (GAAP): $0.02 vs analyst estimates of $0.02 (in line)

- Adjusted EBITDA: $74.5 million vs analyst estimates of $72.95 million (11.3% margin, 2.1% beat)

- EBITDA guidance for the full year is $310 million at the midpoint, above analyst estimates of $299.6 million

- Operating Margin: 4.1%, up from -1.3% in the same quarter last year

- Free Cash Flow was $45.56 million, up from -$6.85 million in the same quarter last year

- Market Capitalization: $1.23 billion

“During the second quarter, Vestis continued to advance its strategic transformation through targeted initiatives aimed at enhancing operating leverage* and profitability,” said Jim Barber, President and CEO.

Company Overview

Operating a network of more than 350 facilities with 3,300 delivery routes serving customers weekly, Vestis (NYSE: VSTS) provides uniform rentals, workplace supplies, and facility services to over 300,000 business locations across the United States and Canada.

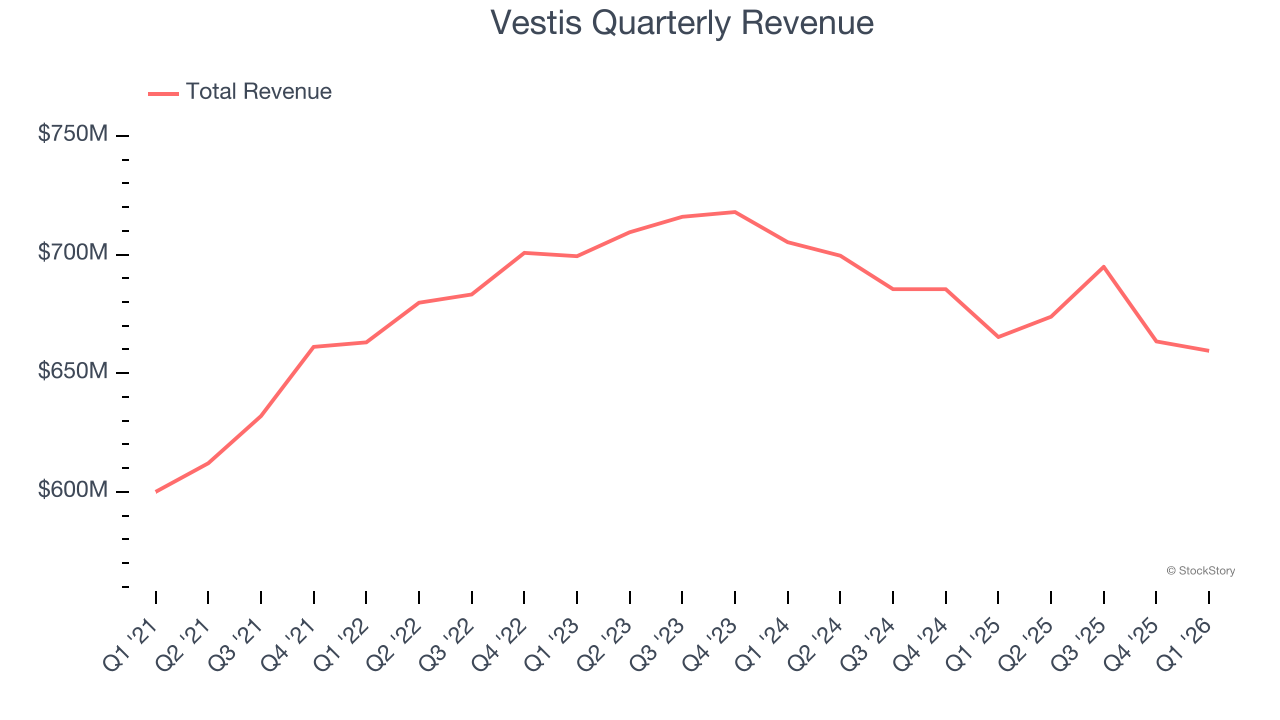

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $2.69 billion in revenue over the past 12 months, Vestis is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Vestis’s sales grew at a sluggish 1.8% compounded annual growth rate over the last five years. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Vestis’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 2.8% annually.

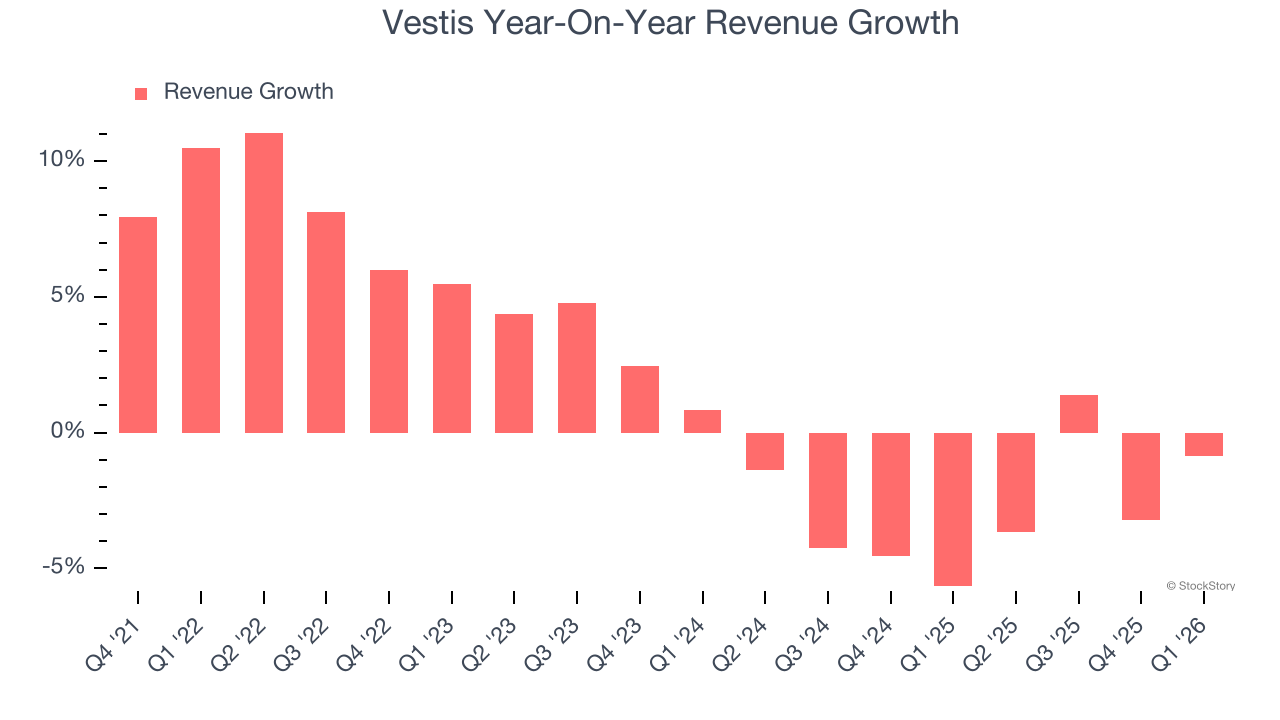

This quarter, Vestis’s $659.4 million of revenue was flat year on year but beat Wall Street’s estimates by 0.7%.

Looking ahead, sell-side analysts expect revenue to decline by 1.3% over the next 12 months, similar to its two-year rate. Although this projection is better than its two-year trend, it’s hard to get excited about a company that is struggling with demand.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

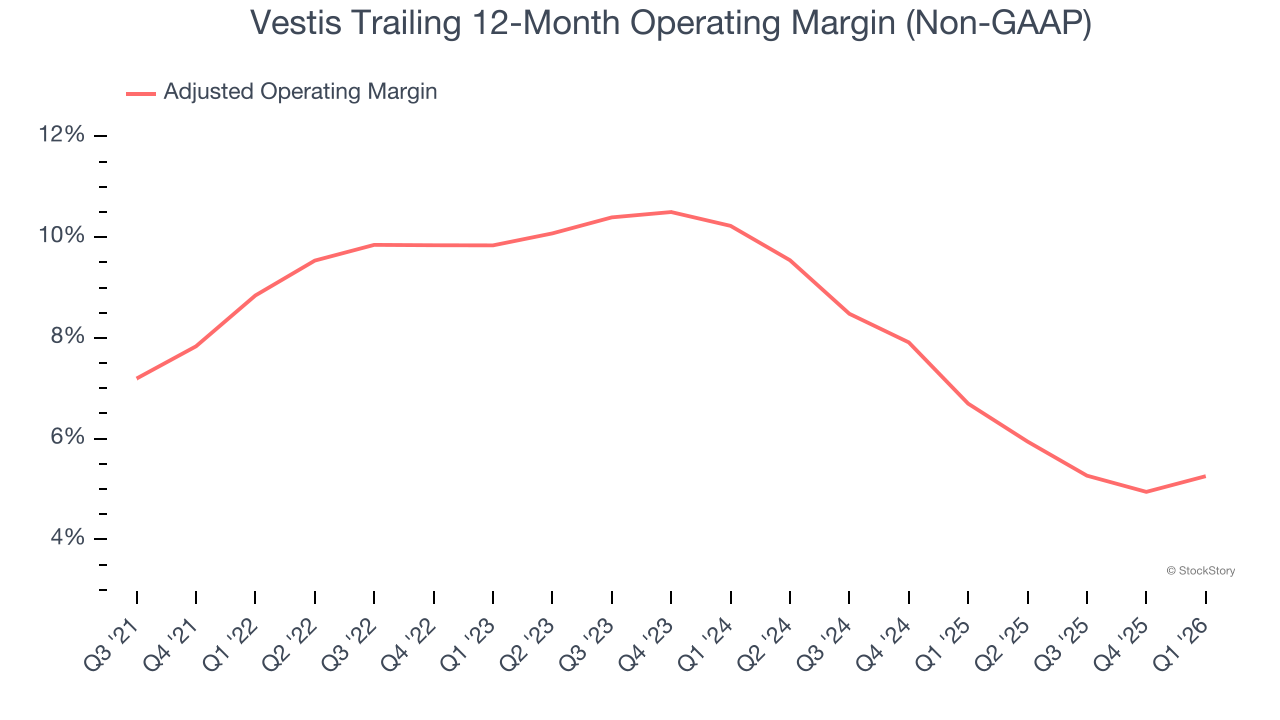

Adjusted Operating Margin

Vestis was profitable over the last five years but held back by its large cost base. Its average adjusted operating margin of 8.2% was weak for a business services business.

Looking at the trend in its profitability, Vestis’s adjusted operating margin decreased by 3.6 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Vestis’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Vestis generated an adjusted operating margin profit margin of 4.6%, up 1.3 percentage points year on year. This increase was a welcome development and shows it was more efficient.

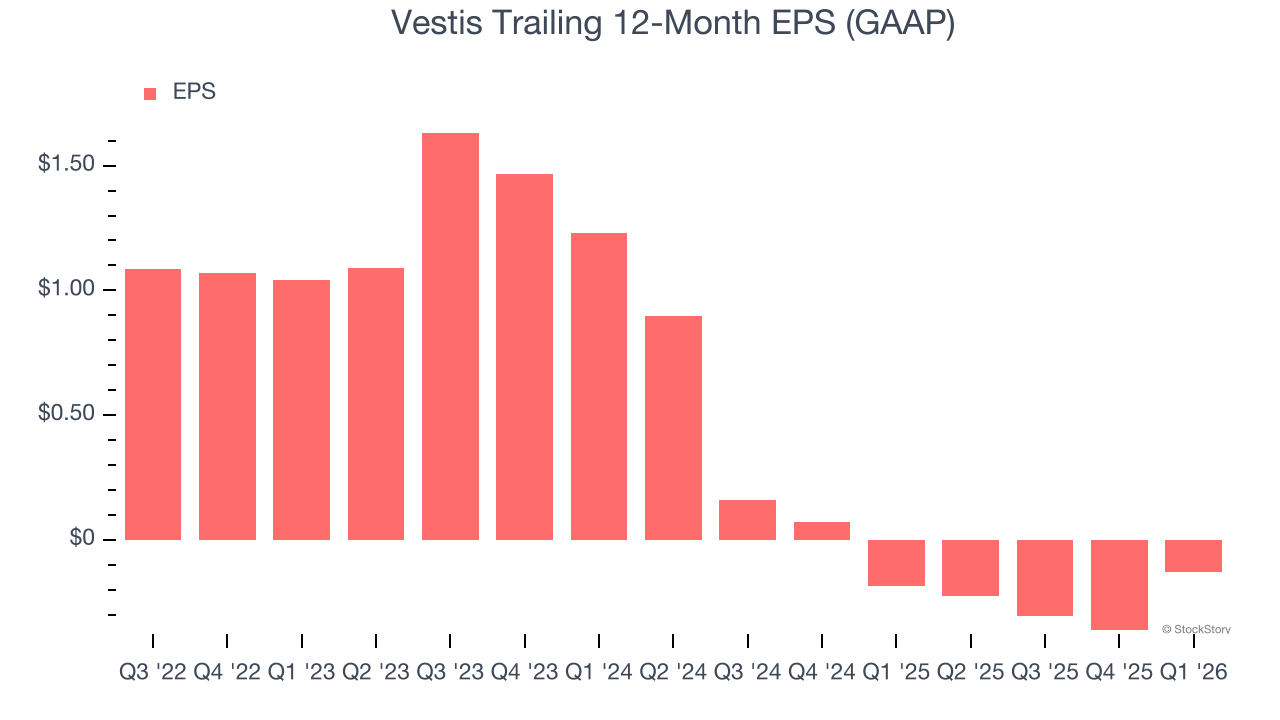

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Vestis’s full-year EPS turned negative over the last four years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Vestis’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Sadly for Vestis, its EPS declined by more than its revenue over the last two years, dropping 45.1%. This tells us the company struggled to adjust to shrinking demand.

Diving into the nuances of Vestis’s earnings can give us a better understanding of its performance. While we mentioned earlier that Vestis’s adjusted operating margin expanded this quarter, a two-year view shows its margin has declined. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, Vestis reported EPS of $0.02, up from negative $0.21 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Vestis’s full-year EPS of negative $0.13 will flip to positive $0.18.

Key Takeaways from Vestis’s Q1 Results

It was good to see Vestis top analysts’ revenue expectations this quarter. EBITDA guidance was also ahead. On the company's 'Strategic Business Transformation', Vestis increase cost savings targets as well. Zooming out, we think this was a good quarter. The stock traded up 28.6% to $11.93 immediately following the results.

Big picture, is Vestis a buy here and now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).