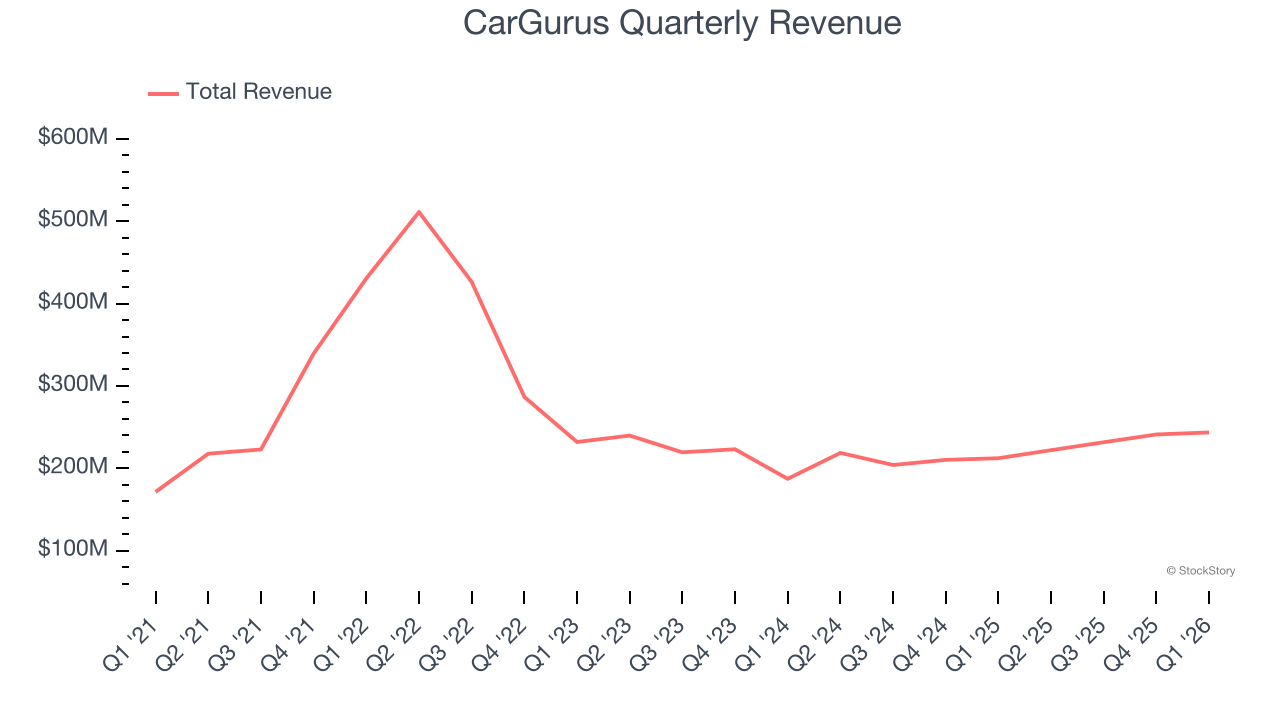

Online auto marketplace CarGurus (NASDAQ: CARG) met Wall Street’s revenue expectations in Q1 CY2026, with sales up 14.8% year on year to $243.6 million. The company expects next quarter’s revenue to be around $249.5 million, close to analysts’ estimates. Its non-GAAP profit of $0.58 per share was 1.8% above analysts’ consensus estimates.

Is now the time to buy CarGurus? Find out by accessing our full research report, it’s free.

CarGurus (CARG) Q1 CY2026 Highlights:

- Revenue: $243.6 million vs analyst estimates of $243 million (14.8% year-on-year growth, in line)

- Adjusted EPS: $0.58 vs analyst estimates of $0.57 (1.8% beat)

- Adjusted EBITDA: $80.23 million vs analyst estimates of $76.83 million (32.9% margin, 4.4% beat)

- Revenue Guidance for Q2 CY2026 is $249.5 million at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for Q2 CY2026 is $0.61 at the midpoint, above analyst estimates of $0.60

- EBITDA guidance for Q2 CY2026 is $81.5 million at the midpoint, above analyst estimates of $80.04 million

- Operating Margin: 16.5%, down from 23.9% in the same quarter last year

- Free Cash Flow Margin: 25.9%, down from 31.7% in the previous quarter

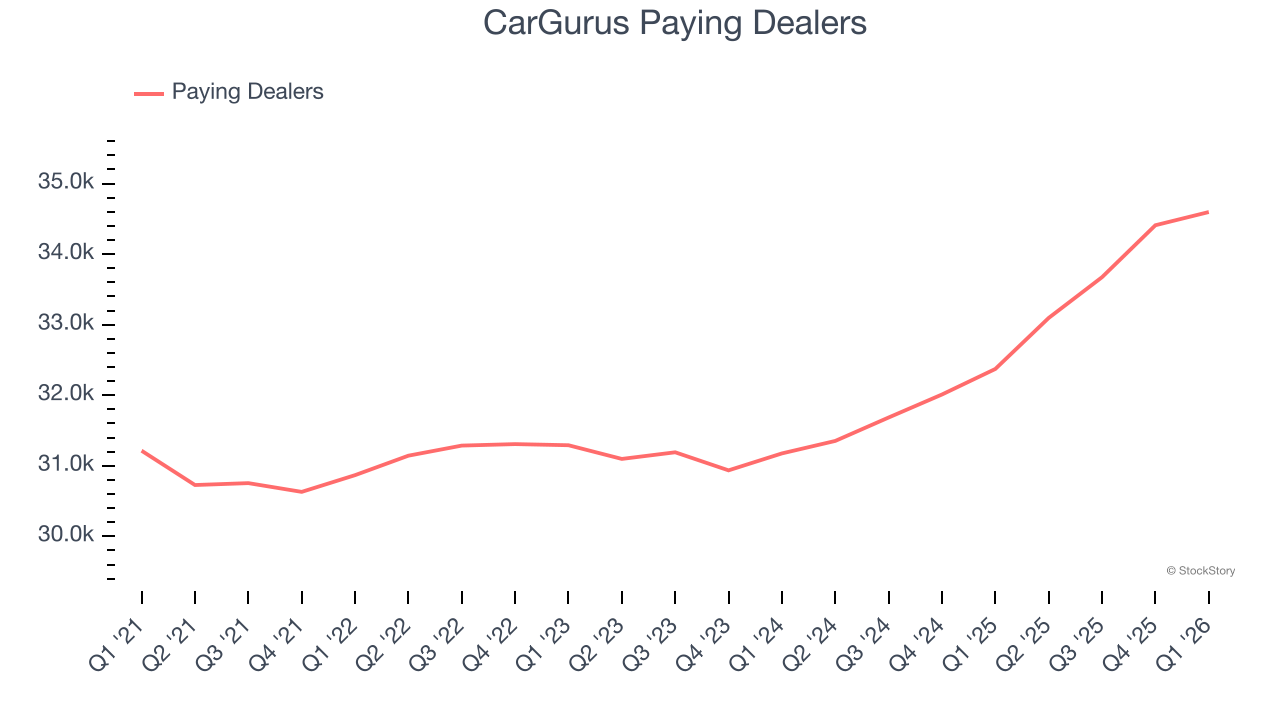

- Paying Dealers: 34,596, up 2,224 year on year

- Market Capitalization: $3.56 billion

“We are pleased with our first quarter results, as we sustained our momentum with revenue growing 15% year-over-year as we continued to invest in AI-led product innovation across dealer pillars and the consumer journey,” said Jason Trevisan, Chief Executive Officer at CarGurus.

Company Overview

Bringing transparency to a sometimes opaque process, CarGurus (NASDAQ: CARG) is a digital marketplace where auto dealers can connect with potential customers and where car buyers can browse, purchase, and obtain financing.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last three years, CarGurus’s demand was weak and its revenue declined by 13.6% per year. This wasn’t a great result, but there are still things to like about CarGurus.

This quarter, CarGurus’s year-on-year revenue growth was 14.8%, and its $243.6 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 12.4% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 10.3% over the next 12 months, an acceleration versus the last three years. This projection is above average for the sector and implies its newer products and services will fuel better top-line performance.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Paying Dealers

User Growth

As an online marketplace, CarGurus generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Over the last two years, CarGurus’s paying dealers, a key performance metric for the company, increased by 4.5% annually to 34,596 in the latest quarter. This growth rate lags behind the hottest consumer internet applications. If CarGurus wants to accelerate growth, it likely needs to engage users more effectively with its existing offerings or innovate with new products.

In Q1, CarGurus added 2,224 paying dealers, leading to 6.9% year-on-year growth. The quarterly print was higher than its two-year result, suggesting its new initiatives are accelerating user growth.

Revenue Per User

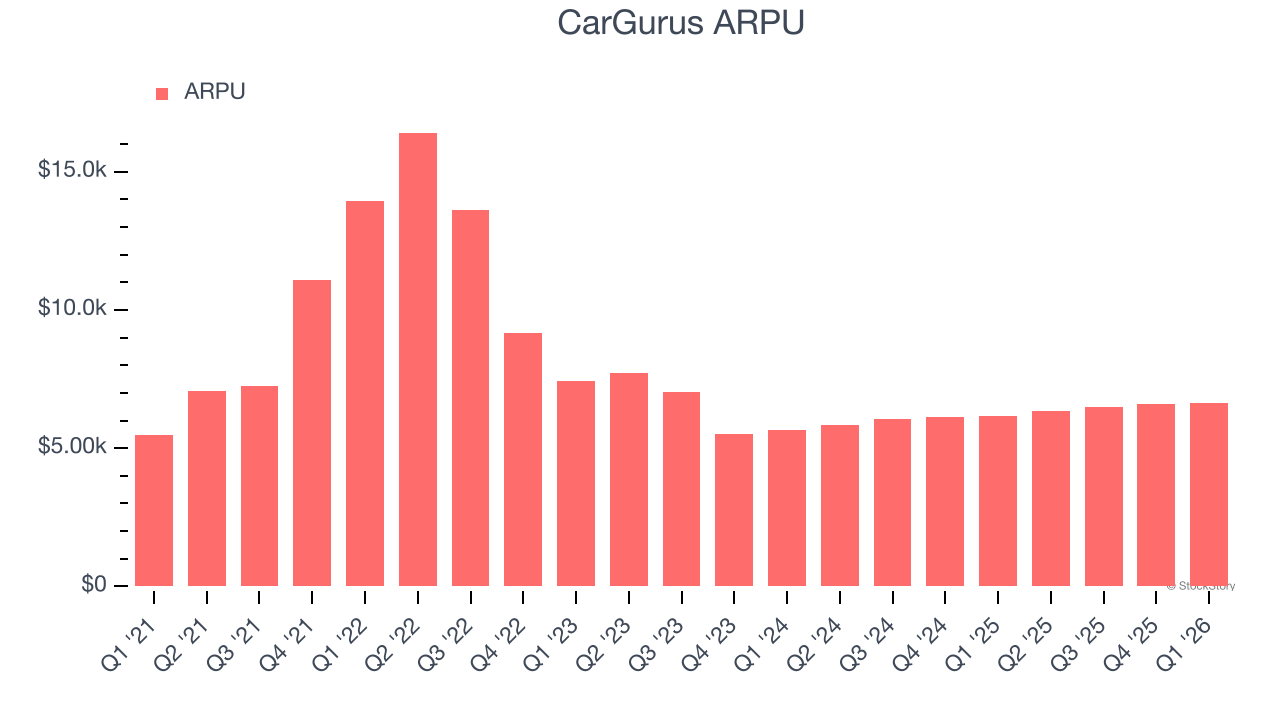

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns in transaction fees from each user. ARPU also gives us unique insights into a user’s average order size and CarGurus’s take rate, or "cut", on each order.

CarGurus’s ARPU growth has been subpar over the last two years, averaging 1.7%. This isn’t great when combined with its weaker paying dealers performance. If CarGurus tries boosting ARPU by taking a more aggressive approach to monetization, it’s unclear whether user growth would be sustainable.

This quarter, CarGurus’s ARPU clocked in at $6,647. It grew by 7.7% year on year, mirroring the performance of its paying dealers.

Key Takeaways from CarGurus’s Q1 Results

We enjoyed seeing CarGurus beat analysts’ EBITDA expectations this quarter. We were also glad its EBITDA guidance for next quarter exceeded Wall Street’s estimates. Overall, this print had some key positives. The market seemed to be hoping for more, and the stock traded down 5.7% to $35.96 immediately after reporting.

Should you buy the stock or not? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).