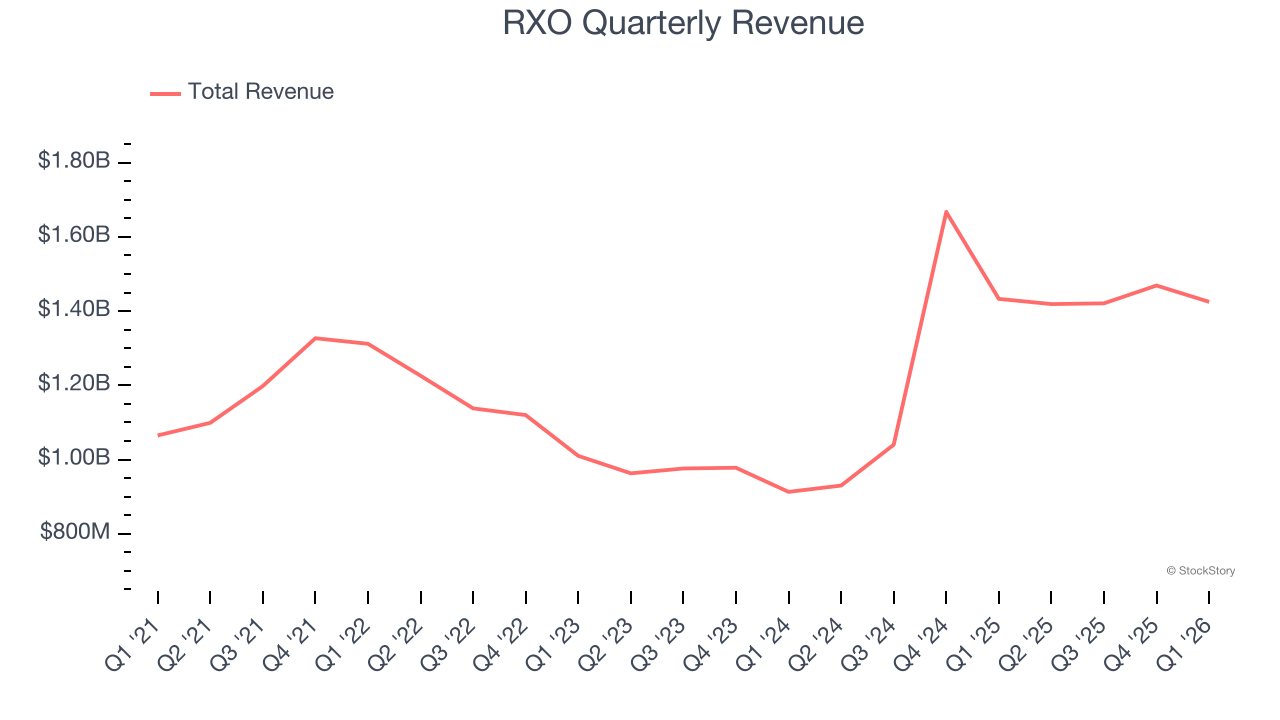

Freight Delivery Company RXO (NYSE: RXO) reported Q1 CY2026 results topping the market’s revenue expectations, but sales were flat year on year at $1.43 billion. Its non-GAAP loss of $0.09 per share was in line with analysts’ consensus estimates.

Is now the time to buy RXO? Find out by accessing our full research report, it’s free.

RXO (RXO) Q1 CY2026 Highlights:

- Revenue: $1.43 billion vs analyst estimates of $1.34 billion (flat year on year, 6% beat)

- Adjusted EPS: -$0.09 vs analyst estimates of -$0.09 (in line)

- Adjusted EBITDA: $6 million vs analyst estimates of $6.13 million (0.4% margin, 2.1% miss)

- EBITDA guidance for Q2 CY2026 is $32 million at the midpoint, above analyst estimates of $23.76 million

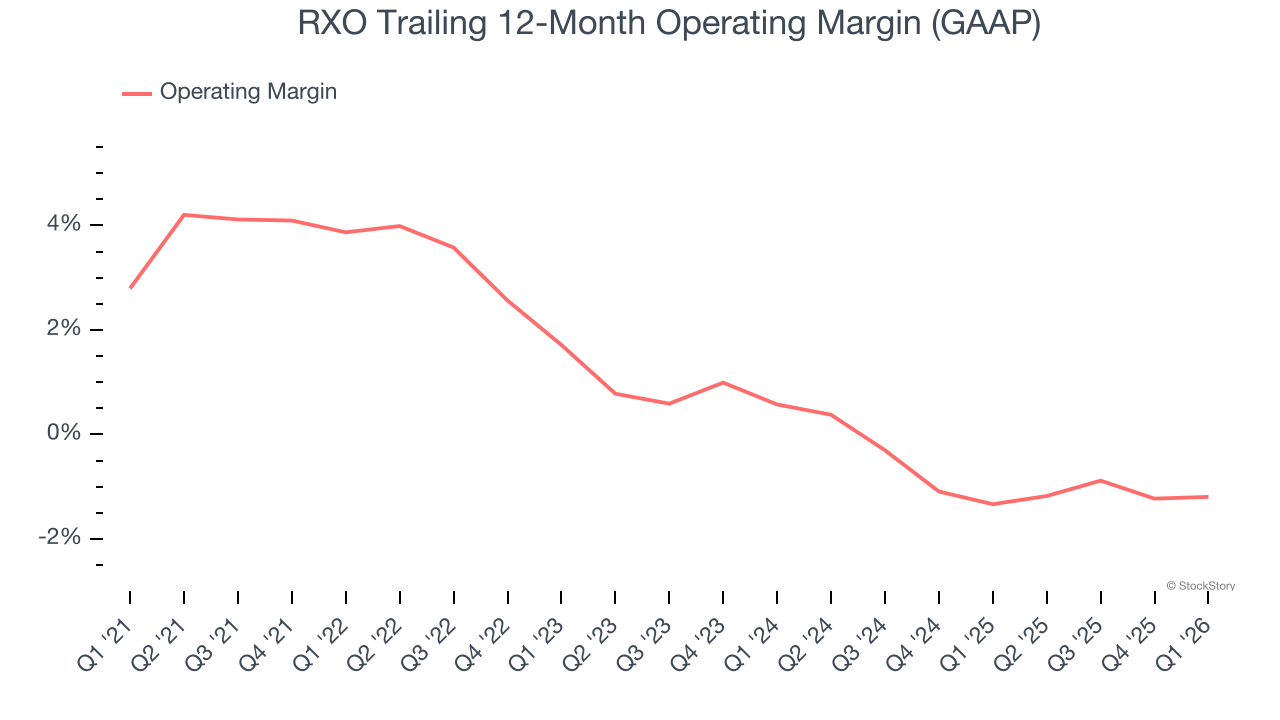

- Operating Margin: -2%, in line with the same quarter last year

- Free Cash Flow was -$24 million compared to -$17 million in the same quarter last year

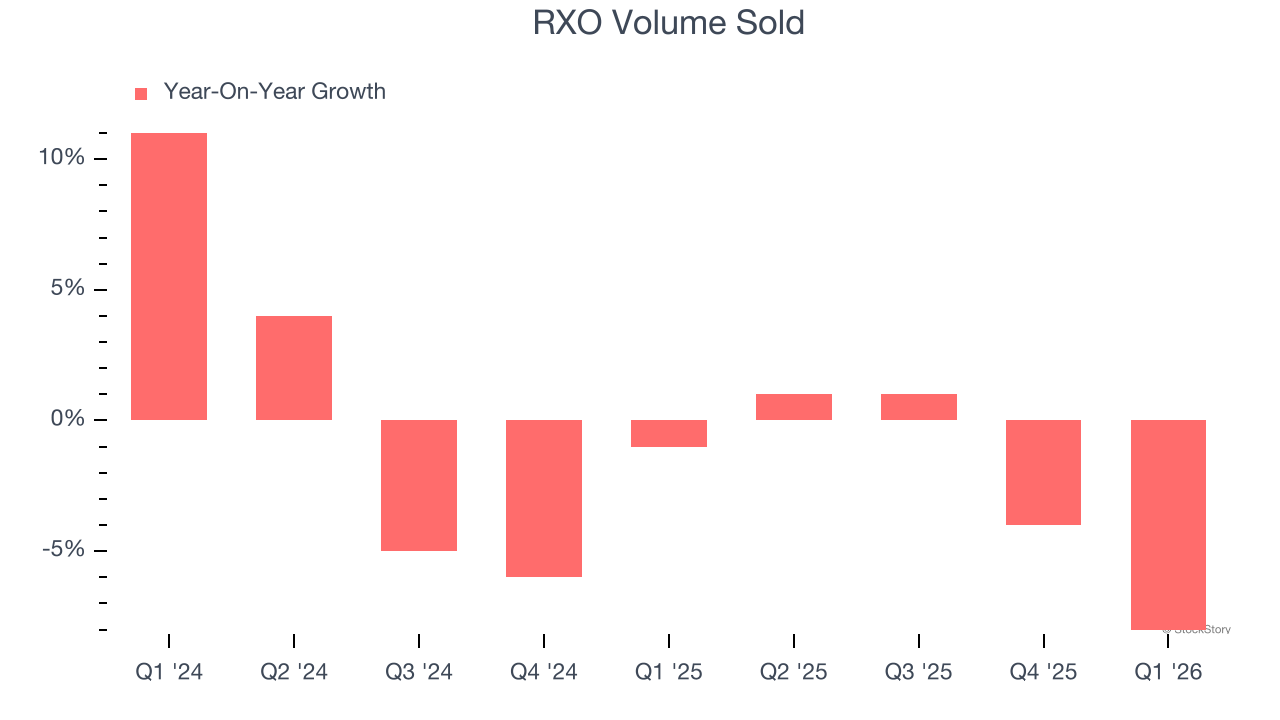

- Sales Volumes fell 8% year on year (-1% in the same quarter last year)

- Market Capitalization: $3.23 billion

RXO Chairman and CEO Drew Wilkerson said, “We have significant momentum in our business. We’re converting our strong Brokerage sales pipeline and, while our Brokerage volume declined by 8% year-over-year in the first quarter, our full truckload volume improved every month as the quarter progressed. In addition, our truckload spot mix increased by 500 basis points sequentially in the quarter, which helped drive an increase in gross profit per load. During the quarter, our Managed Transportation business was awarded more than $100 million in freight under management and our late-stage sales pipeline increased by more than $200 million. When it comes to the broader market, we’re seeing clear signs of improvement, primarily driven by supply-side tightening, despite overall soft demand.”

Company Overview

With access to millions of trucks, RXO (NYSE: RXO) offers full-truckload, less-than-truckload, and last-mile deliveries.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, RXO grew its sales at a solid 9% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers.

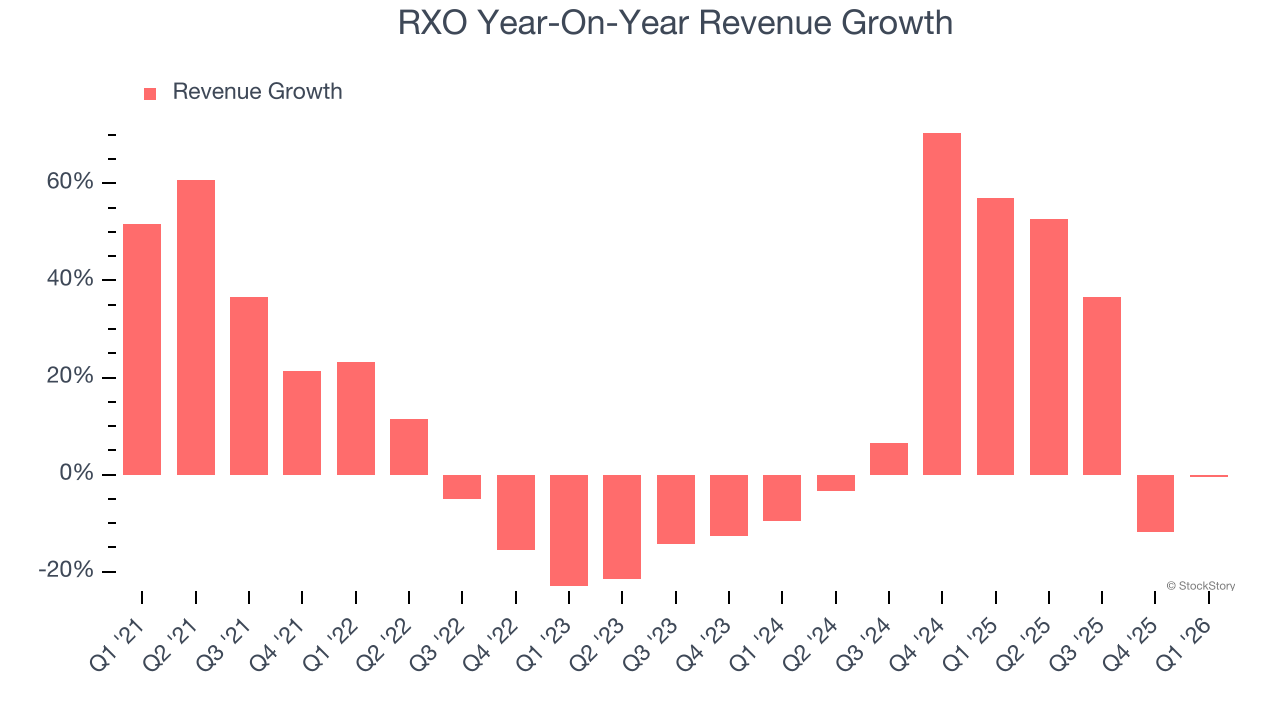

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. RXO’s annualized revenue growth of 22.4% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

RXO also reports its number of units sold. Over the last two years, RXO’s units sold averaged 2.2% year-on-year declines. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, RXO’s $1.43 billion of revenue was flat year on year but beat Wall Street’s estimates by 6%.

Looking ahead, sell-side analysts expect revenue to grow 3.1% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will see some demand headwinds.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

RXO was roughly breakeven when averaging the last five years of quarterly operating profits, inadequate for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, RXO’s operating margin decreased by 5.1 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. RXO’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, RXO generated an operating margin profit margin of negative 2%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

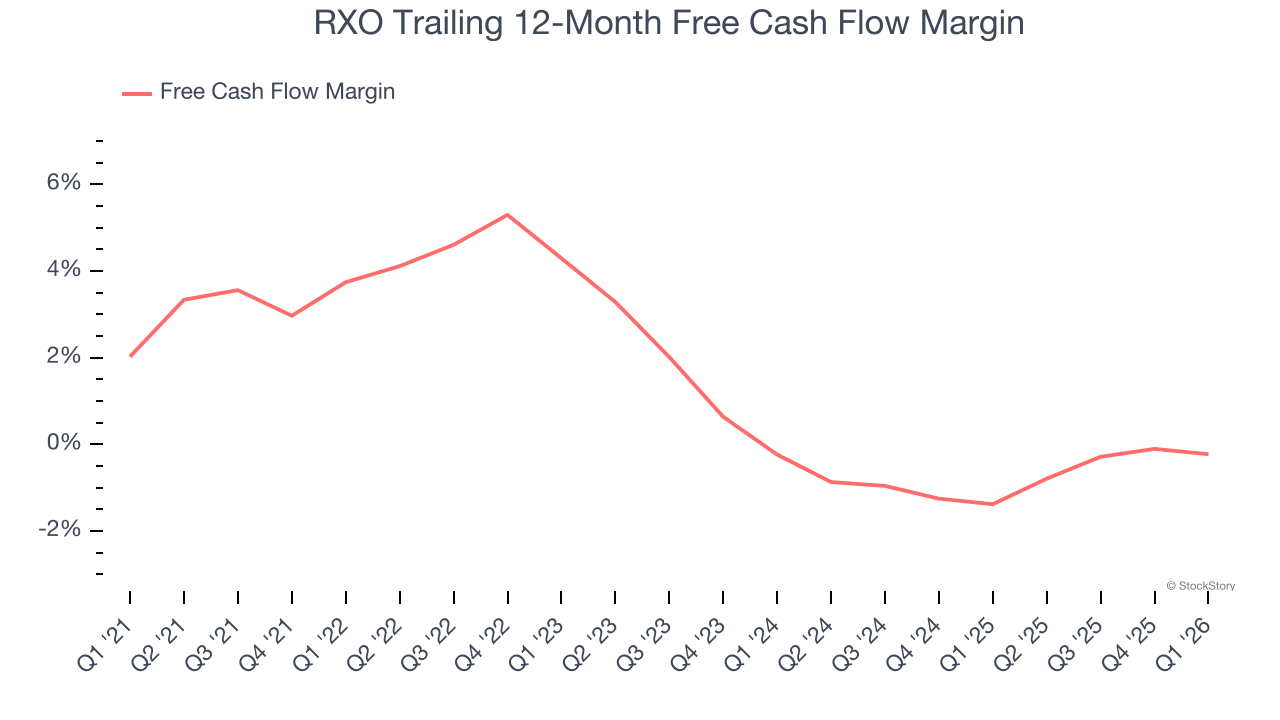

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

RXO has shown poor cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 1.2%, below what we’d expect for an industrials business.

Taking a step back, we can see that RXO’s margin dropped by 4 percentage points during that time. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the trend continues, it could signal it’s in the middle of an investment cycle.

RXO burned through $24 million of cash in Q1, equivalent to a negative 1.7% margin. The company’s cash burn was similar to its $17 million of lost cash in the same quarter last year. These numbers deviate from its longer-term margin, indicating it is a seasonal business that must build up inventory during certain quarters.

Key Takeaways from RXO’s Q1 Results

We were impressed by RXO’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its adjusted operating income missed and its EBITDA fell short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The stock traded up 9.4% to $21.46 immediately following the results.

Is RXO an attractive investment opportunity right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).