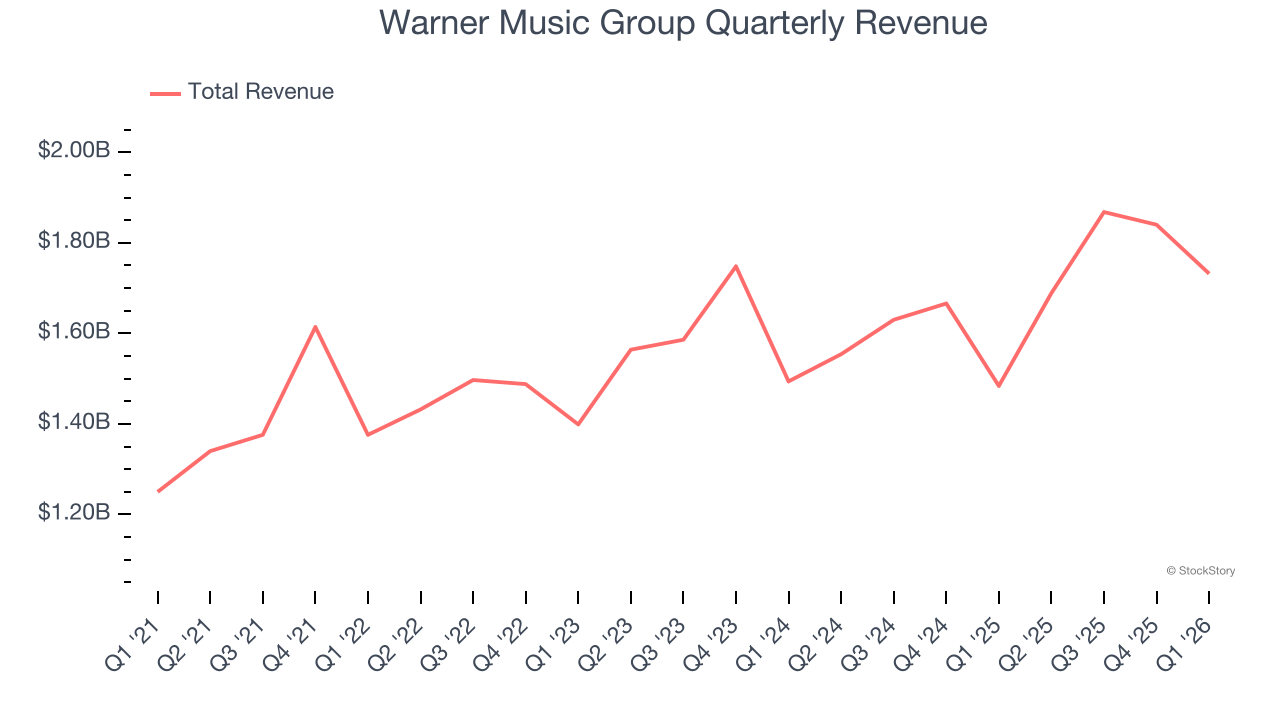

Global music entertainment company Warner Music Group (NASDAQ: WMG) announced better-than-expected revenue in Q1 CY2026, with sales up 16.7% year on year to $1.73 billion. Its GAAP profit of $0.34 per share was 26.9% above analysts’ consensus estimates.

Is now the time to buy Warner Music Group? Find out by accessing our full research report, it’s free.

Warner Music Group (WMG) Q1 CY2026 Highlights:

- Revenue: $1.73 billion vs analyst estimates of $1.61 billion (16.7% year-on-year growth, 7.5% beat)

- EPS (GAAP): $0.34 vs analyst estimates of $0.27 (26.9% beat)

- Adjusted EBITDA: $397 million vs analyst estimates of $356 million (22.9% margin, 11.5% beat)

- Operating Margin: 15.2%, up from 11.3% in the same quarter last year

- Free Cash Flow Margin: 5.7%, up from 2.2% in the same quarter last year

- Market Capitalization: $15.85 billion

Company Overview

Launching the careers of legendary artists like Frank Sinatra, Warner Music Group (NASDAQ: WMG) is a music company managing a diverse portfolio of artists, recordings, and music publishing services worldwide.

Revenue Growth

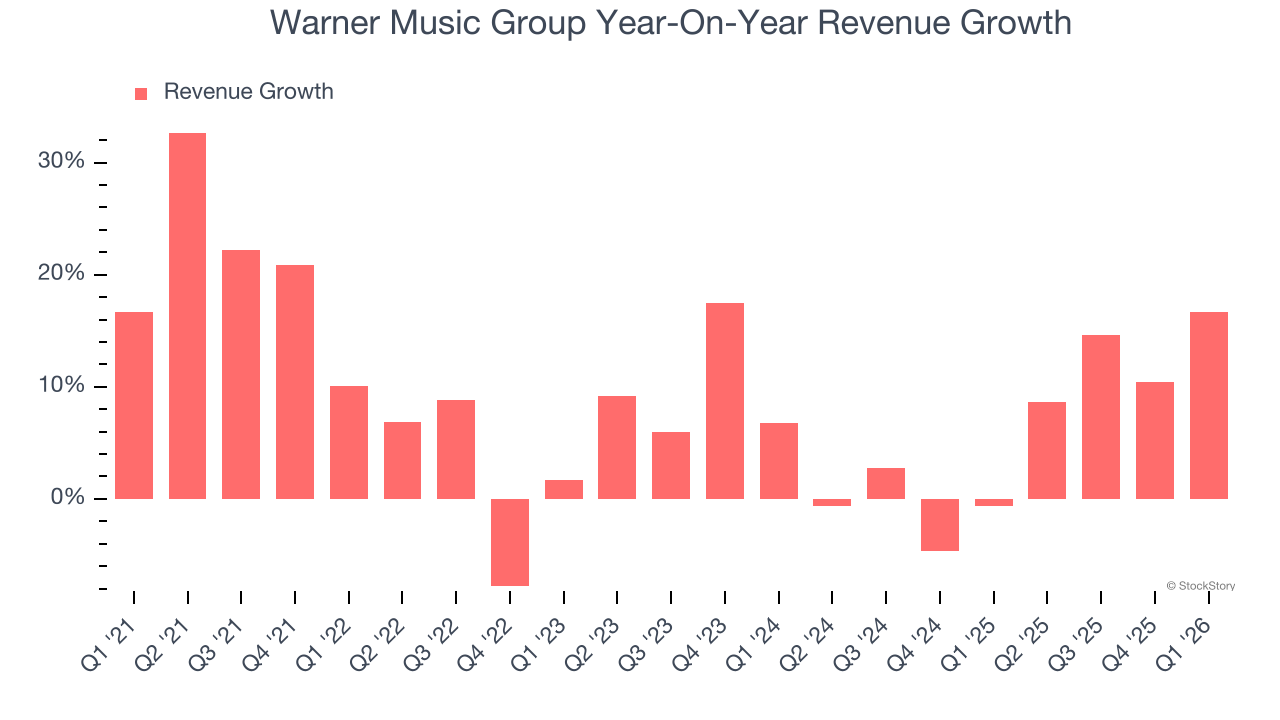

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Warner Music Group’s sales grew at a weak 8.6% compounded annual growth rate over the last five years. This fell short of our benchmark for the consumer discretionary sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Warner Music Group’s recent performance shows its demand has slowed as its annualized revenue growth of 5.6% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

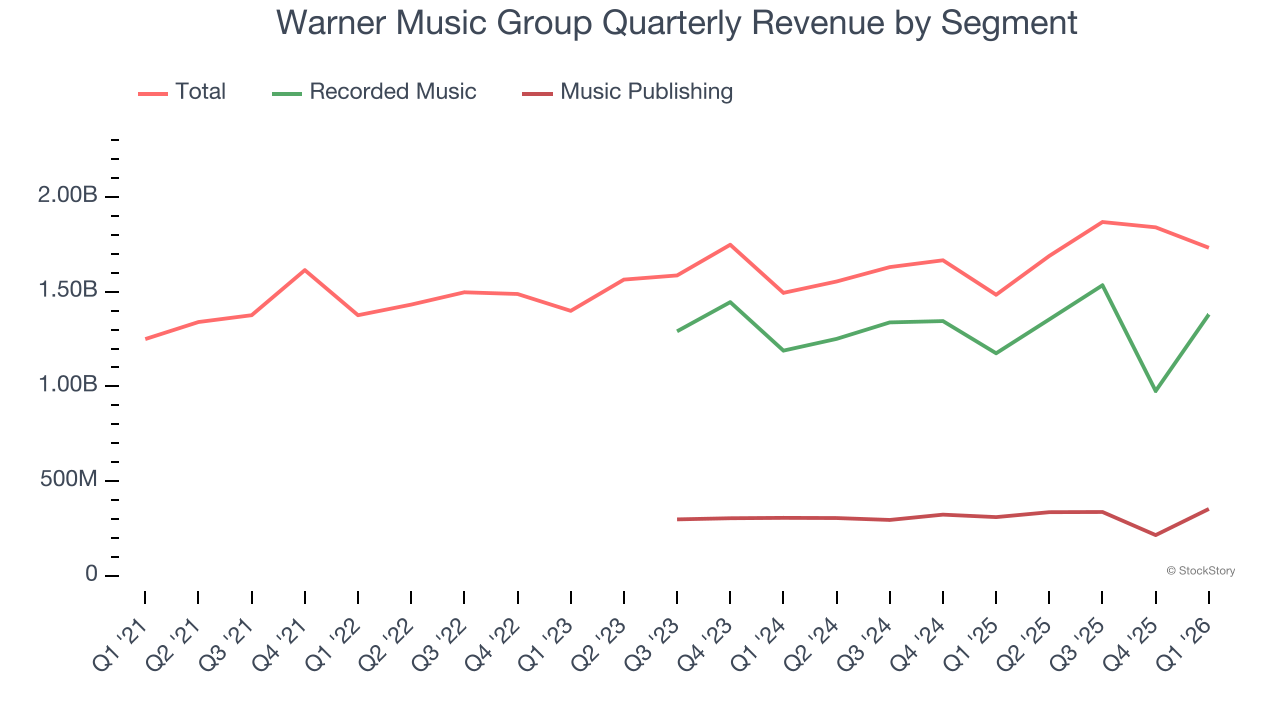

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Recorded Music and Music Publishing, which are 79.7% and 20.4% of revenue. Over the last two years, Warner Music Group’s Recorded Music revenue (new music production) averaged 1.2% year-on-year growth while its Music Publishing revenue (royalties from catalog music) averaged 1.6% growth.

This quarter, Warner Music Group reported year-on-year revenue growth of 16.7%, and its $1.73 billion of revenue exceeded Wall Street’s estimates by 7.5%.

Looking ahead, sell-side analysts expect revenue to grow 3.3% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and indicates its products and services will face some demand challenges.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

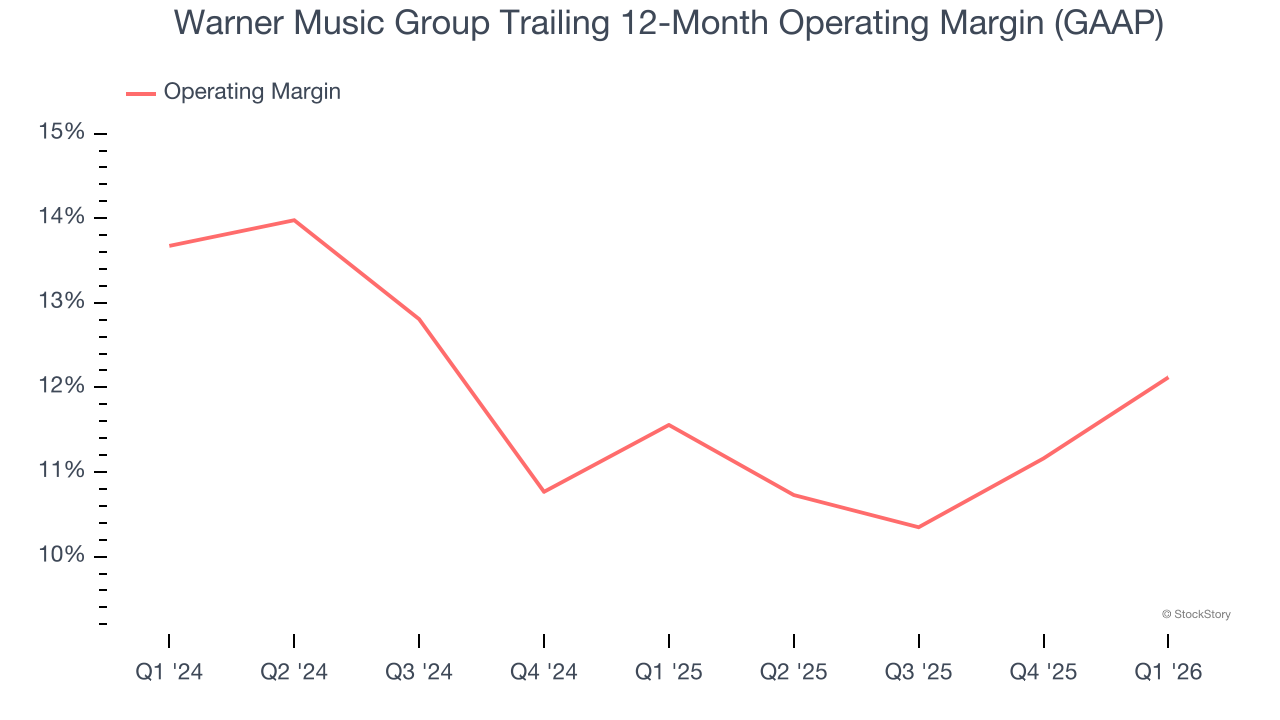

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Warner Music Group’s operating margin has more or less stayed the same over the last 12 months , and we generally like to see margin increases due to economies of scale and cost efficiency over time.

In Q1, Warner Music Group generated an operating margin profit margin of 15.2%, up 3.9 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

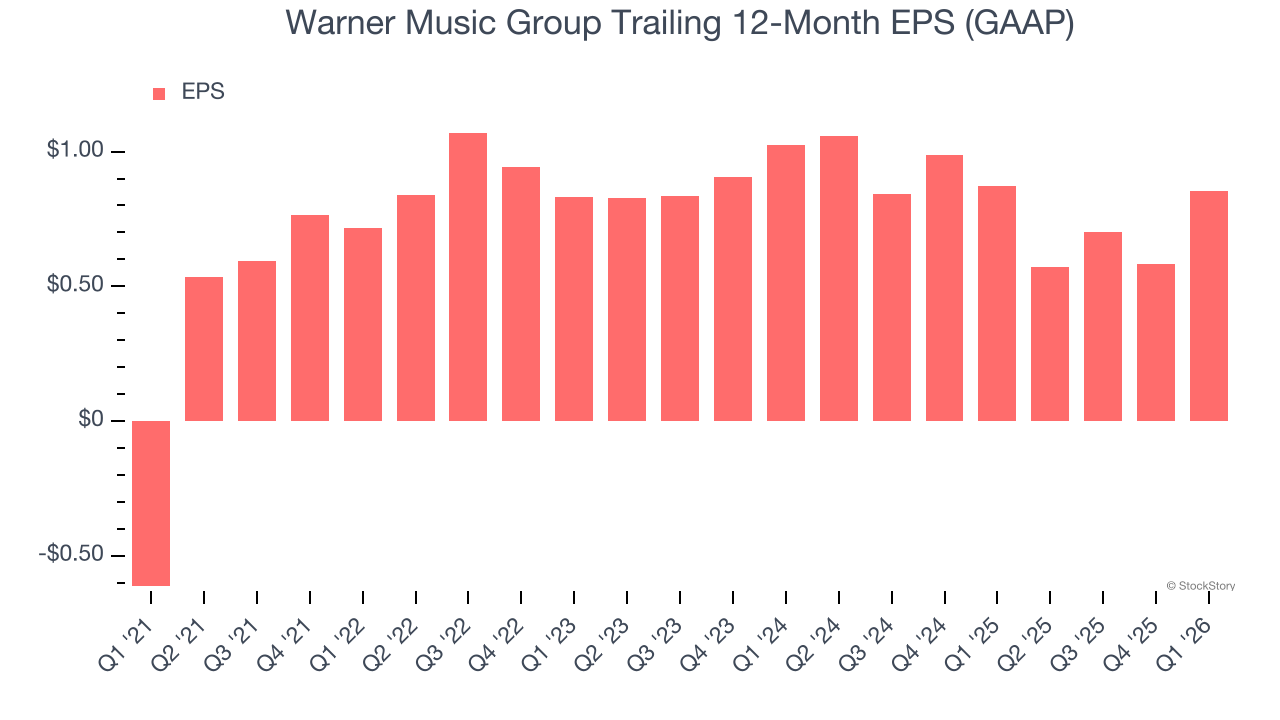

Warner Music Group’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q1, Warner Music Group reported EPS of $0.34, up from $0.07 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Warner Music Group’s full-year EPS of $0.86 to grow 83%.

Key Takeaways from Warner Music Group’s Q1 Results

We enjoyed seeing Warner Music Group beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 4.6% to $32.49 immediately following the results.

Sure, Warner Music Group had a solid quarter, but if we look at the bigger picture, is this stock a buy? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).