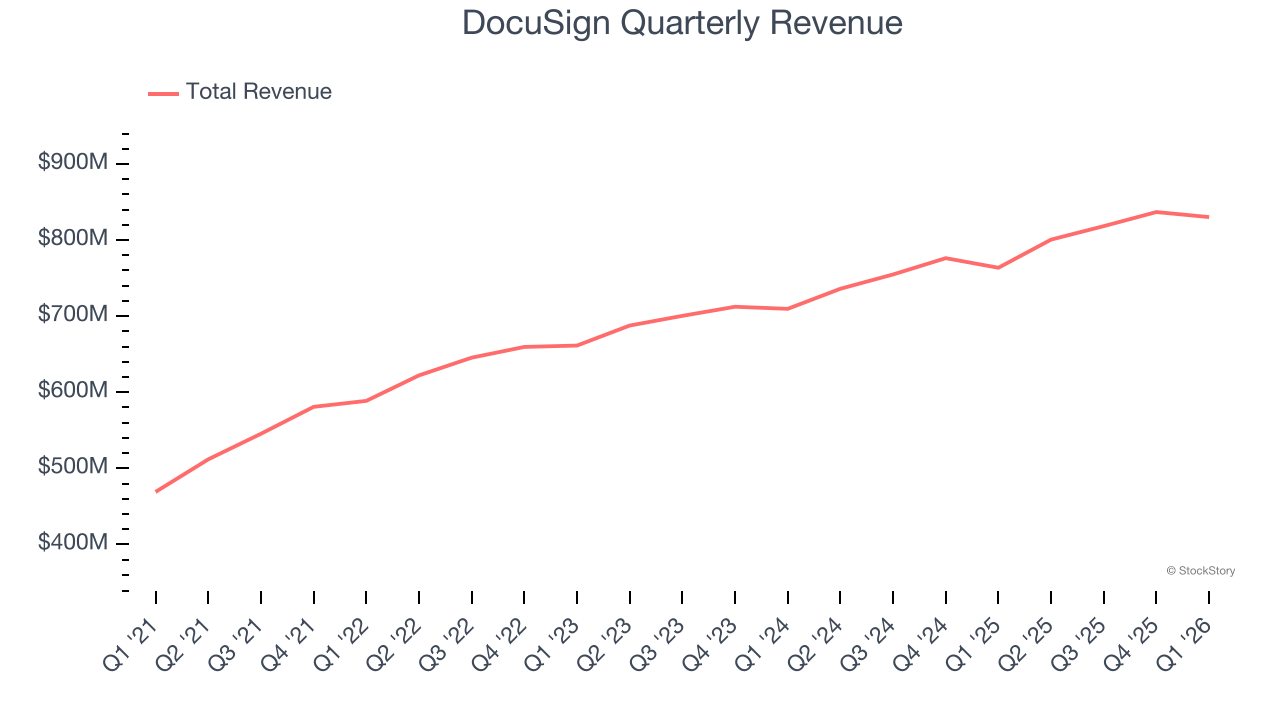

Electronic signature company DocuSign (NASDAQ: DOCU) announced better-than-expected revenue in Q1 CY2026, with sales up 8.7% year on year to $830.2 million. The company expects next quarter’s revenue to be around $867 million, close to analysts’ estimates. Its non-GAAP profit of $1.09 per share was 9.7% above analysts’ consensus estimates.

Is now the time to buy DocuSign? Find out by accessing our full research report, it’s free.

DocuSign (DOCU) Q1 CY2026 Highlights:

- Revenue: $830.2 million vs analyst estimates of $825.3 million (8.7% year-on-year growth, 0.6% beat)

- Adjusted EPS: $1.09 vs analyst estimates of $0.99 (9.7% beat)

- Adjusted Operating Income: $265.6 million vs analyst estimates of $241.4 million (32% margin, 10% beat)

- The company slightly lifted its revenue guidance for the full year to $3.50 billion at the midpoint from $3.49 billion

- Operating Margin: 13.4%, up from 7.9% in the same quarter last year

- Free Cash Flow Margin: 34.9%, down from 41.8% in the previous quarter

- Market Capitalization: $10.18 billion

"In Q1, we saw continued growing demand for Docusign's AI-native IAM platform with 40,000 customers investing in our rapidly expanding roadmap," said Allan Thygesen, CEO of Docusign.

Company Overview

Creating the digital equivalent of "sign on the dotted line" for over a billion users worldwide, DocuSign (NASDAQ: DOCU) provides an agreement management platform that enables businesses to electronically prepare, sign, and manage documents and contracts.

Revenue Growth

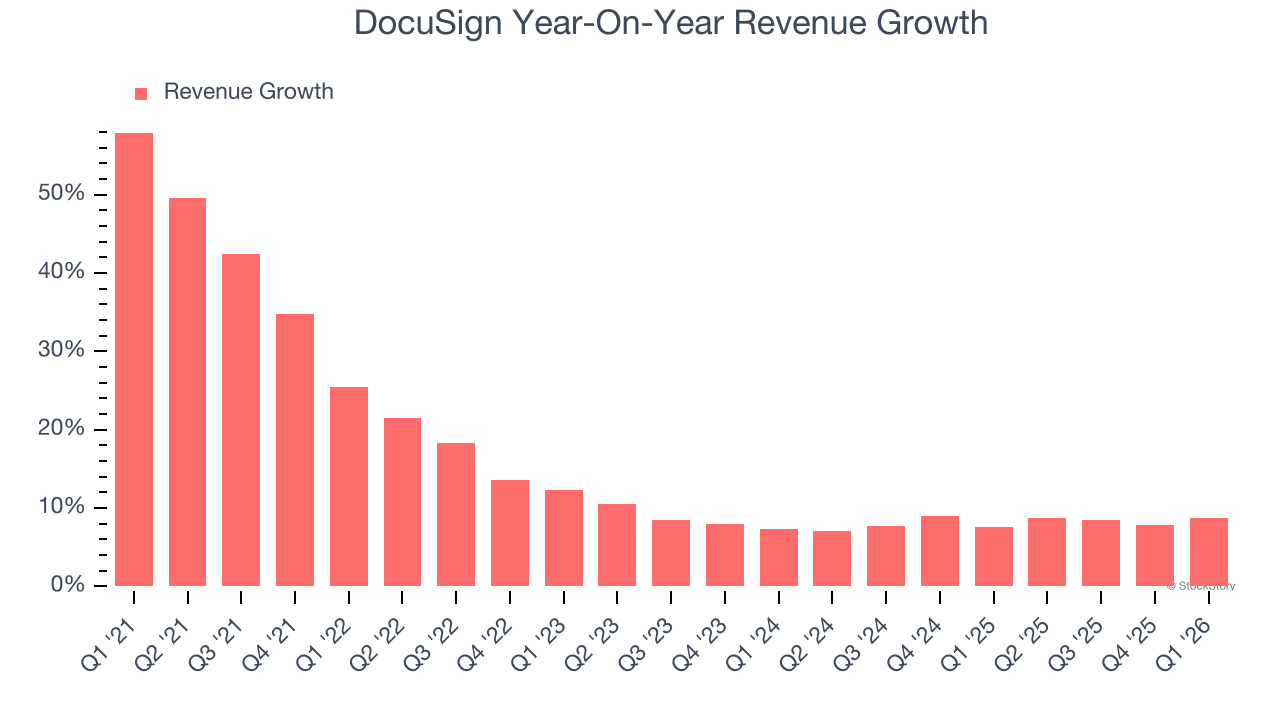

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, DocuSign grew its sales at a 15.1% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. DocuSign’s recent performance shows its demand has slowed as its annualized revenue growth of 8.1% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, DocuSign reported year-on-year revenue growth of 8.7%, and its $830.2 million of revenue exceeded Wall Street’s estimates by 0.6%. Company management is currently guiding for a 8.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.1% over the next 12 months, similar to its two-year rate. This projection doesn’t excite us and suggests its newer products and services will not lead to better top-line performance yet.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

DocuSign’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between DocuSign’s products and its peers.

Key Takeaways from DocuSign’s Q1 Results

We struggled to find many positives in these results. Zooming out, we think this was a mixed quarter. The market seemed to be hoping for more, and the stock traded down 1.7% to $50.31 immediately after reporting.

So should you invest in DocuSign right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).