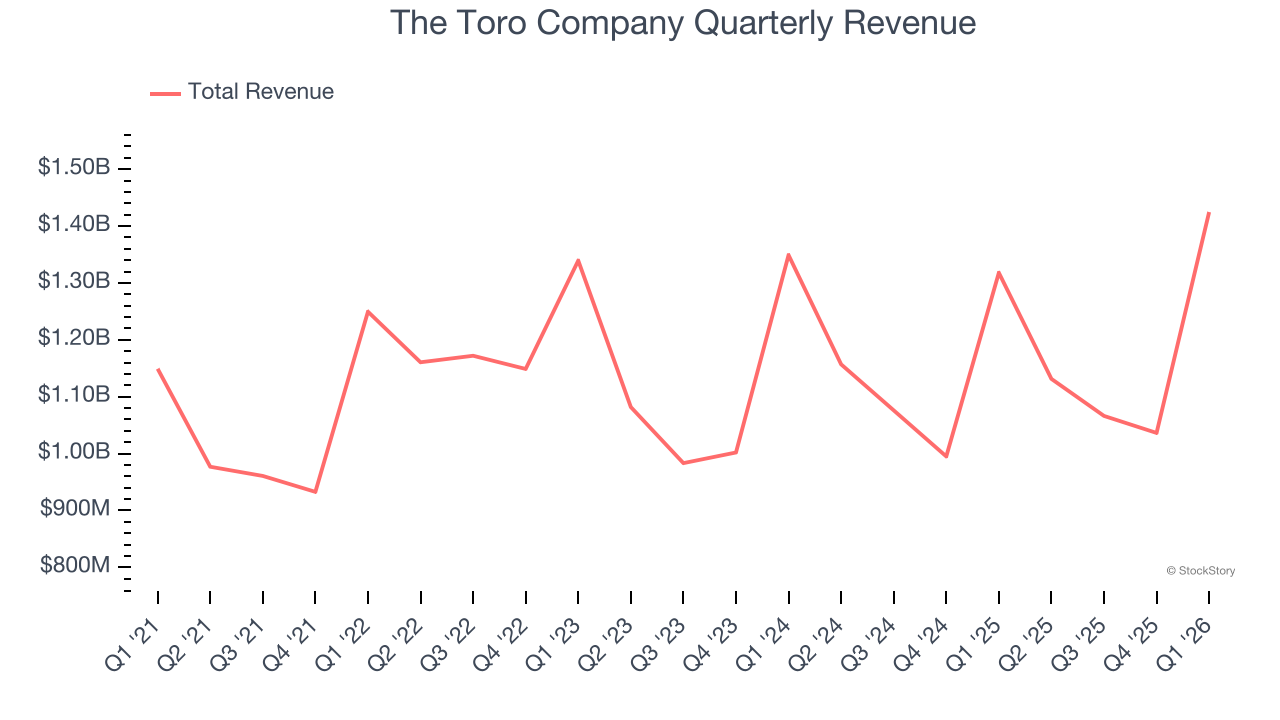

Outdoor equipment company Toro (NYSE: TTC) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 8.1% year on year to $1.42 billion. Its non-GAAP profit of $1.60 per share was 6.7% above analysts’ consensus estimates.

Is now the time to buy The Toro Company? Find out by accessing our full research report, it’s free.

The Toro Company (TTC) Q1 CY2026 Highlights:

- Revenue: $1.42 billion vs analyst estimates of $1.39 billion (8.1% year-on-year growth, 2.1% beat)

- Adjusted EPS: $1.60 vs analyst estimates of $1.50 (6.7% beat)

- Management raised its full-year Adjusted EPS guidance to $4.56 at the midpoint, a 1.3% increase

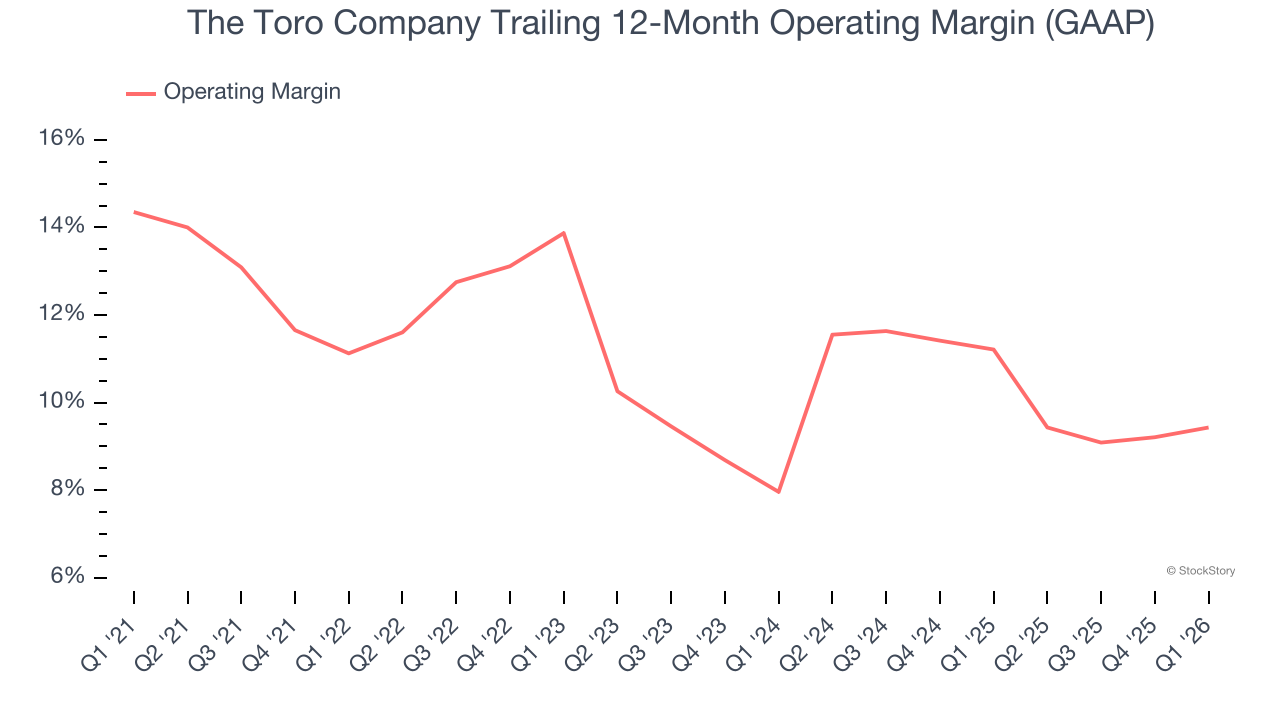

- Operating Margin: 13.7%, in line with the same quarter last year

- Free Cash Flow Margin: 17.6%, up from 11.6% in the same quarter last year

- Market Capitalization: $8.82 billion

Company Overview

Ceasing all production to support the war effort during World War II, Toro (NYSE: TTC) offers outdoor equipment for residential, commercial, and agricultural use.

Revenue Growth

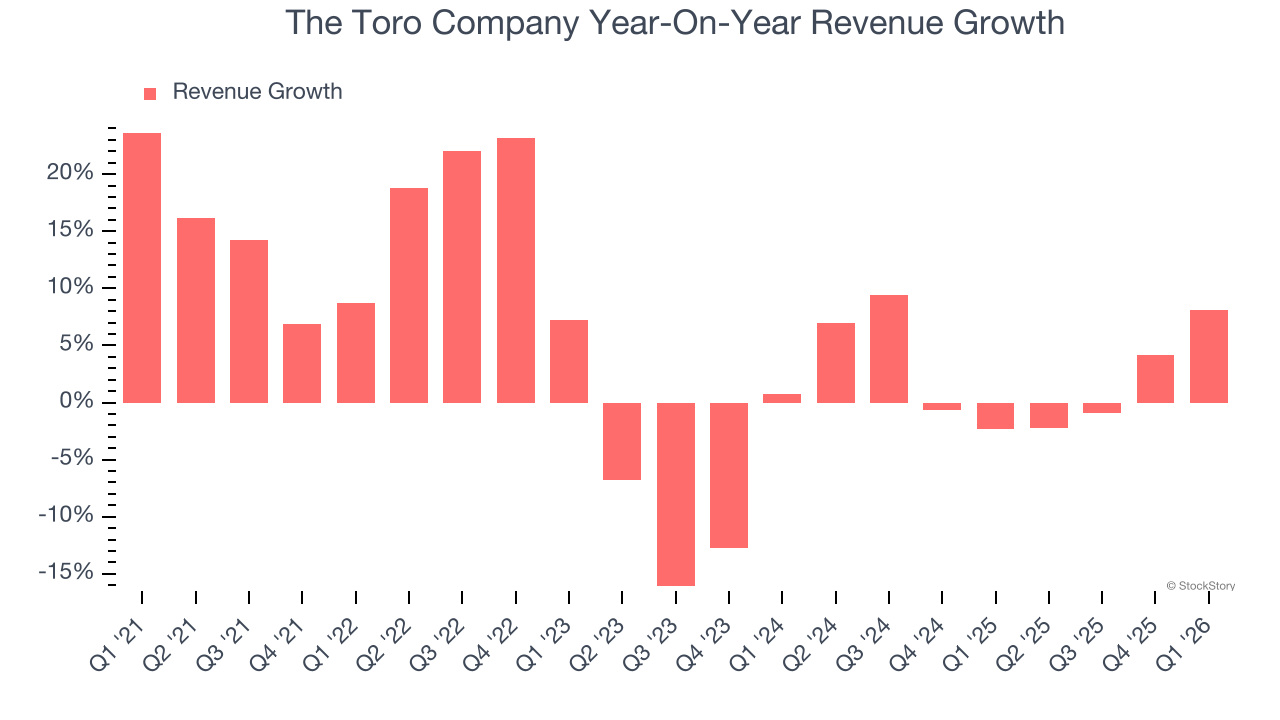

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, The Toro Company’s 4.7% annualized revenue growth over the last five years was tepid. This fell short of our benchmark for the industrials sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. The Toro Company’s recent performance shows its demand has slowed as its annualized revenue growth of 2.7% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

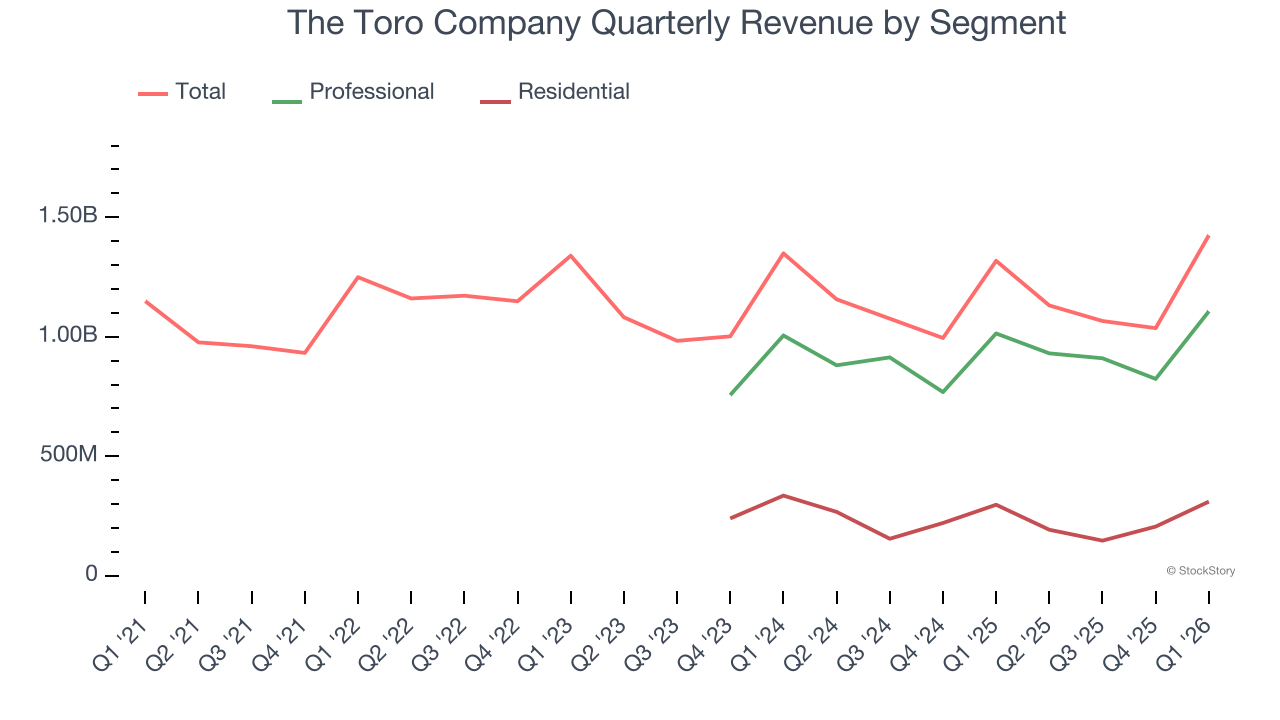

The Toro Company also breaks out the revenue for its most important segments, Professional

and Residential

, which are 77.7% and 21.8% of revenue. Over the last two years, The Toro Company’s Professional

revenue (sales to contractors) averaged 4% year-on-year growth. On the other hand, its Residential

revenue (sales to homeowners) averaged 9.1% declines.

This quarter, The Toro Company reported year-on-year revenue growth of 8.1%, and its $1.42 billion of revenue exceeded Wall Street’s estimates by 2.1%.

Looking ahead, sell-side analysts expect revenue to grow 3.3% over the next 12 months, similar to its two-year rate. This projection is underwhelming and suggests its newer products and services will not accelerate its top-line performance yet.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses — everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

The Toro Company has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 10.8%. This result isn’t too surprising as its gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, The Toro Company’s operating margin decreased by 1.7 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, The Toro Company generated an operating margin profit margin of 13.7%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth — for example, a company could inflate its sales through excessive spending on advertising and promotions.

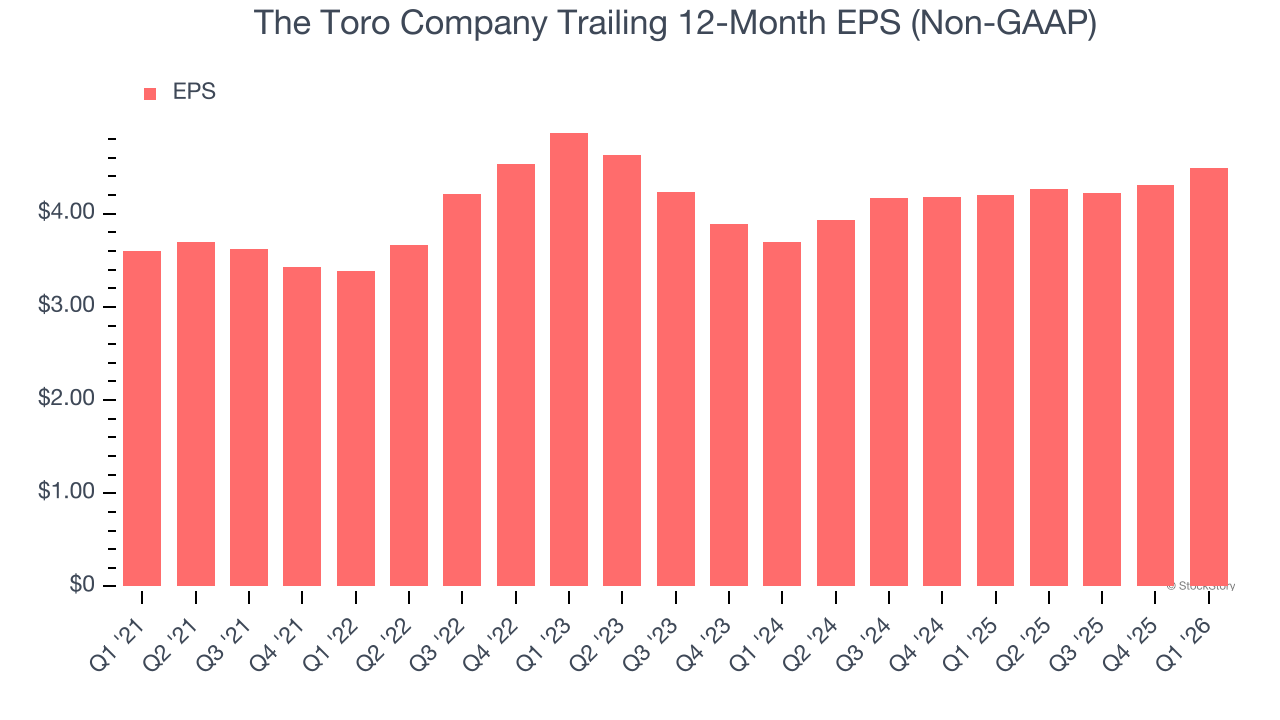

The Toro Company’s unimpressive 4.5% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

The Toro Company’s two-year annual EPS growth of 10.2% was good and topped its 2.7% two-year revenue growth.

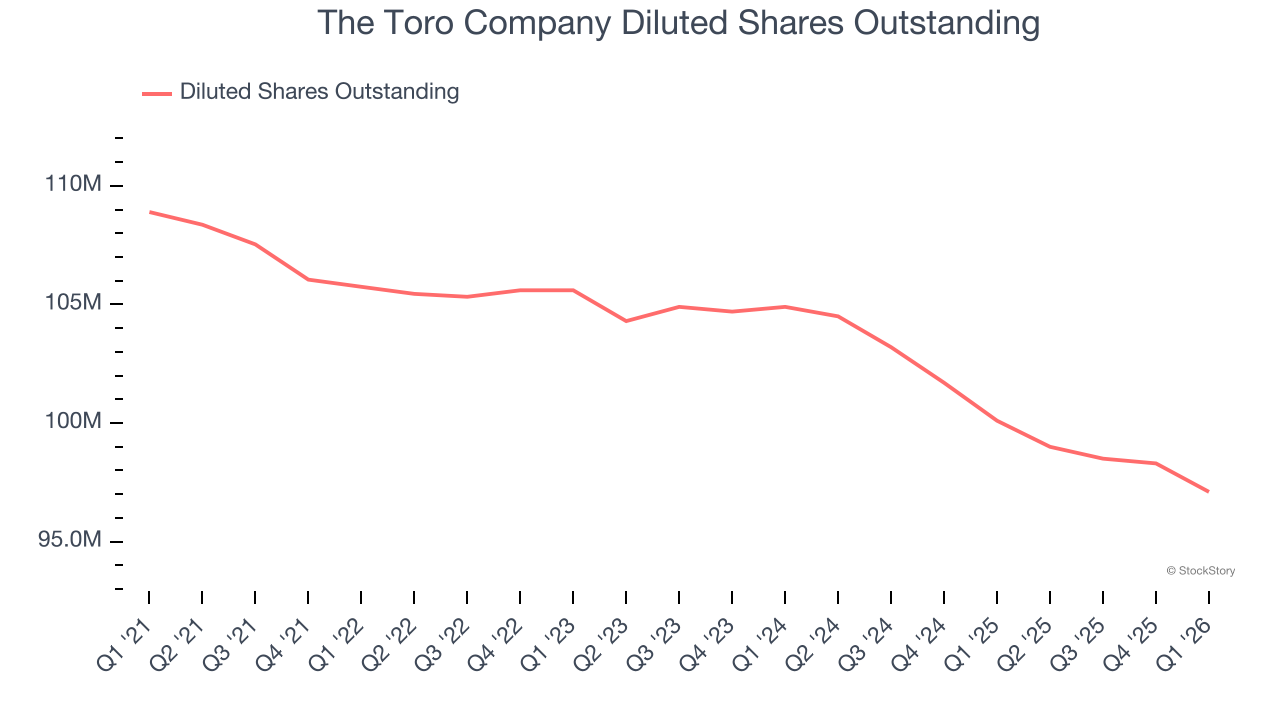

Diving into The Toro Company’s quality of earnings can give us a better understanding of its performance. A two-year view shows that The Toro Company has repurchased its stock, shrinking its share count by 7.4%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q1, The Toro Company reported adjusted EPS of $1.60, up from $1.42 in the same quarter last year. This print beat analysts’ estimates by 6.7%. Over the next 12 months, Wall Street expects The Toro Company’s full-year EPS to grow 7.3% from $4.49 to $4.82.

Key Takeaways from The Toro Company’s Q1 Results

We enjoyed seeing The Toro Company beat analysts’ revenue and EPS expectations this quarter. We were also glad its EPS guidance for the full year was raised. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 6.9% to $97.22 immediately after reporting.

The Toro Company had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).