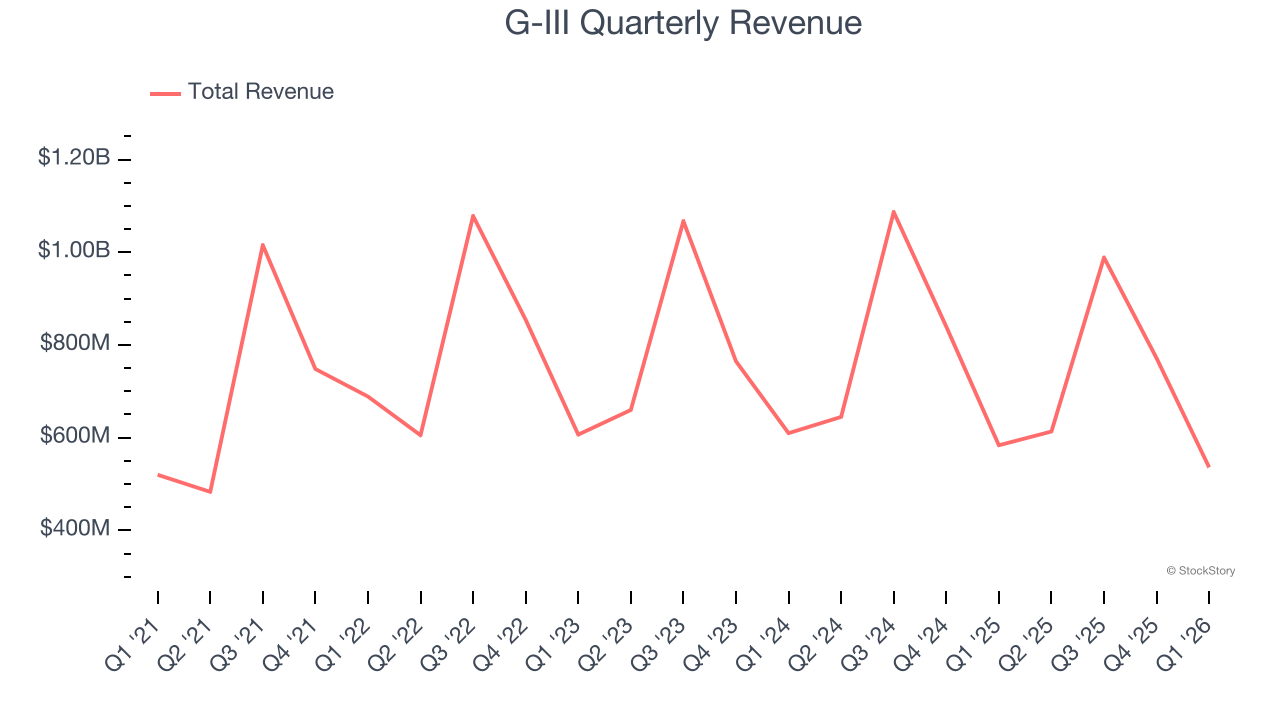

Fashion conglomerate G-III (NASDAQ: GIII) reported Q1 CY2026 results exceeding the market’s revenue expectations, but sales fell by 8.2% year on year to $536 million. Guidance for next quarter’s revenue was optimistic at $570 million at the midpoint, 2.7% above analysts’ estimates. Its non-GAAP loss of $0.21 per share was 30% above analysts’ consensus estimates.

Is now the time to buy G-III? Find out by accessing our full research report, it’s free.

G-III (GIII) Q1 CY2026 Highlights:

- Revenue: $536 million vs analyst estimates of $529.9 million (8.2% year-on-year decline, 1.1% beat)

- Adjusted EPS: -$0.21 vs analyst estimates of -$0.30 (30% beat)

- Adjusted EBITDA: -$7.66 million (-1.4% margin, 148% year-on-year decline)

- The company reconfirmed its revenue guidance for the full year of $2.71 billion at the midpoint

- Management raised its full-year Adjusted EPS guidance to $2.20 at the midpoint, a 7.3% increase

- EBITDA guidance for the full year is $180 million at the midpoint, above analyst estimates of $162.8 million

- Operating Margin: 15.9%, up from 1.5% in the same quarter last year

- Market Capitalization: $1.35 billion

Morris Goldfarb, G-III’s Chairman and Chief Executive Officer, said, “I am very pleased with our first quarter results, which demonstrate the G-III team’s ability to execute in a dynamic environment. The quarter was better than expected with both our net sales and earnings coming in ahead of guidance. Our go-forward portfolio saw continued momentum and healthy full-price selling, which contributed to meaningful gross margin expansion versus the prior year. Based on our strong first quarter results, we are raising our earnings guidance for fiscal 2027.”

Company Overview

Founded as a small leather goods business, G-III (NASDAQ: GIII) is a fashion and apparel conglomerate with a diverse portfolio of brands.

Revenue Growth

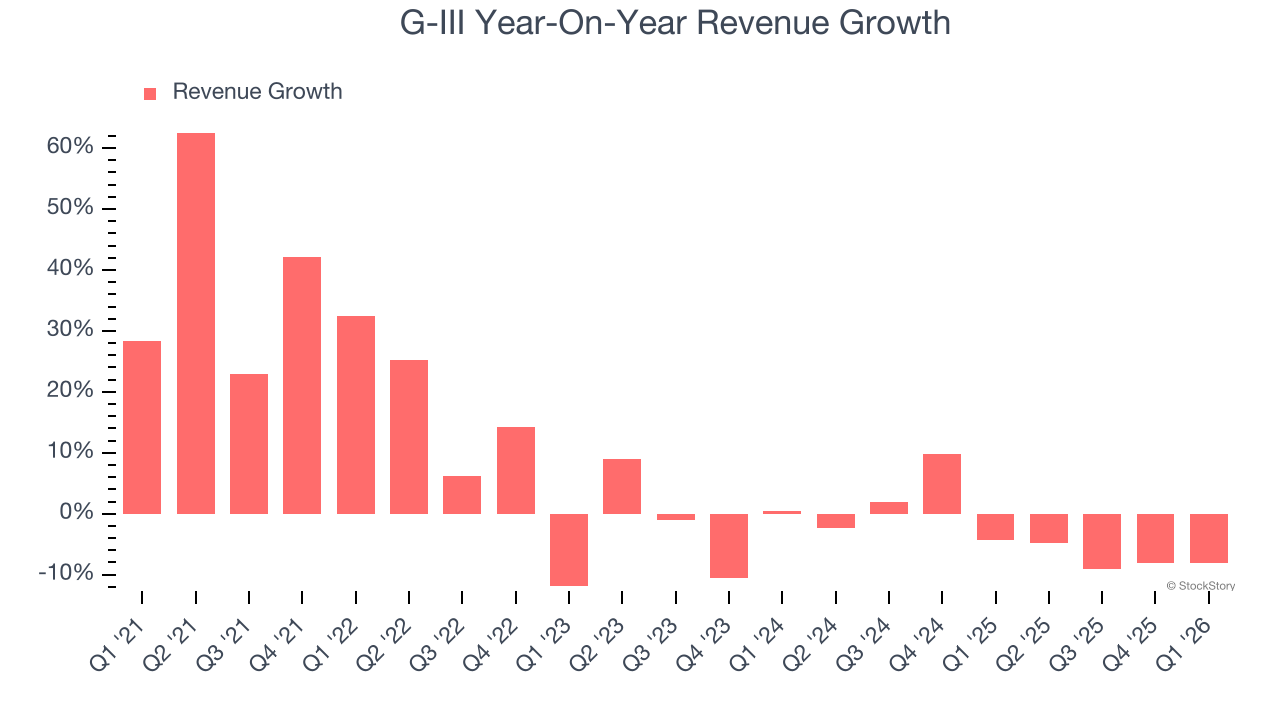

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, G-III’s 6% annualized revenue growth over the last five years was weak. This fell short of our benchmark for the consumer discretionary sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. G-III’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 3.1% annually.

This quarter, G-III’s revenue fell by 8.2% year on year to $536 million but beat Wall Street’s estimates by 1.1%. Company management is currently guiding for a 7.1% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 7% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will face some demand challenges.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

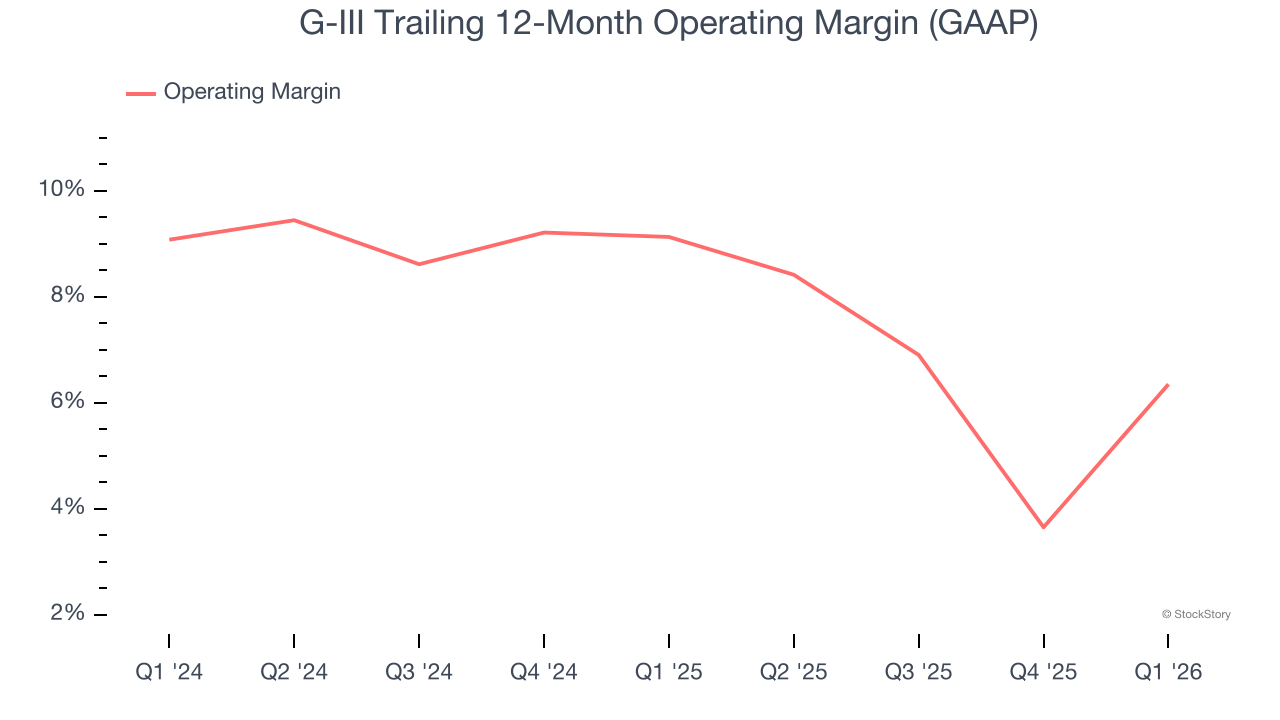

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

G-III’s operating margin has shrunk over the last 12 months and averaged 7.8% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

In Q1, G-III generated an operating margin profit margin of 15.9%, up 14.5 percentage points year on year. This increase was a welcome development, especially since its revenue fell, showing it was more efficient because it scaled down its expenses.

Earnings Per Share

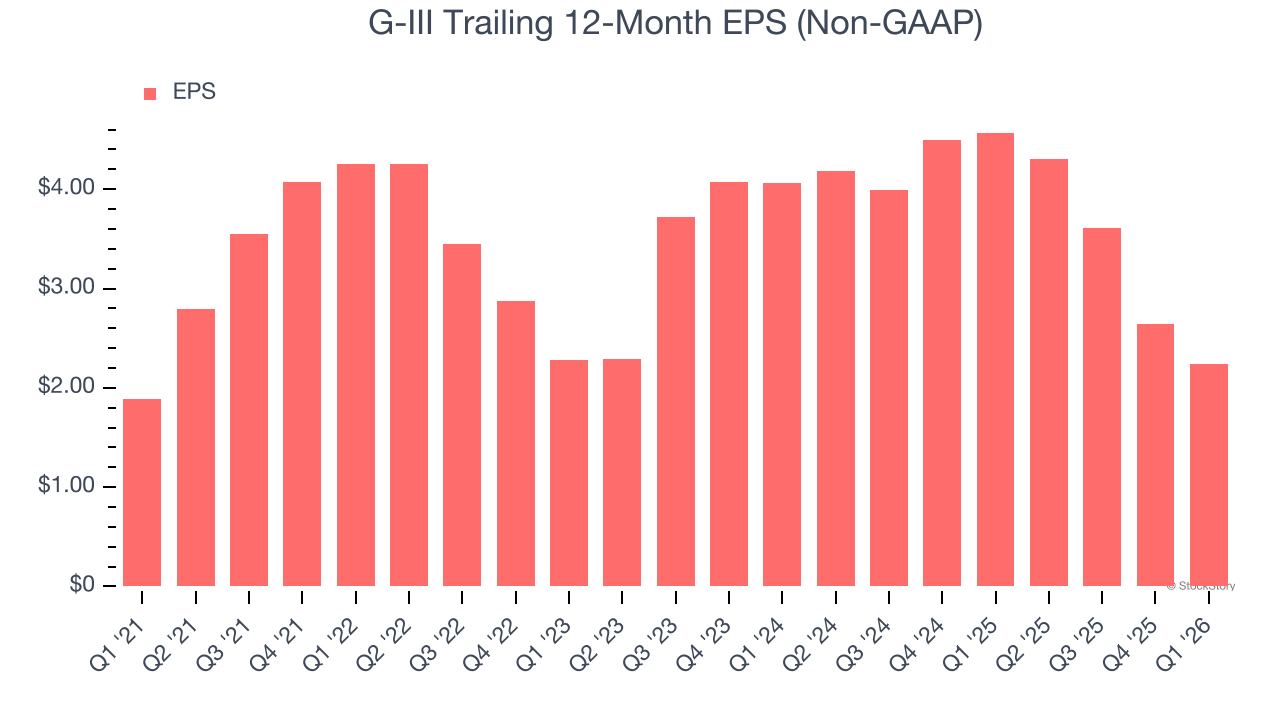

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

G-III’s EPS grew at a weak 3.5% compounded annual growth rate over the last five years, lower than its 6% annualized revenue growth. We can see the difference stemmed from higher taxes as the company actually improved its operating margin and repurchased its shares during this time.

In Q1, G-III reported adjusted EPS of negative $0.21, down from $0.19 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from G-III’s Q1 Results

We were impressed by G-III’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 8.9% to $34.90 immediately following the results.

G-III had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).