Wrapping up Q1 earnings, we look at the numbers and key takeaways for the data & business process services stocks, including Equifax (NYSE: EFX) and its peers.

A combination of increasing reliance on data and analytics across various industries and the desire for cost efficiency through outsourcing could mean that companies in this space gain. As functions such as payroll, HR, and credit risk assessment rely on more digitization, key players in the data & business process services industry could be increased demand. On the other hand, the sector faces headwinds from growing regulatory scrutiny on data privacy and security, with laws like GDPR and evolving U.S. regulations potentially limiting data collection and monetization strategies. Additionally, rising cyber threats pose risks to firms handling sensitive personal and financial information, creating outsized headline risk when things go wrong in this area.

The 10 data & business process services stocks we track reported a strong Q1. As a group, revenues beat analysts’ consensus estimates by 2.7% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady. On average, they are relatively unchanged since the latest earnings results.

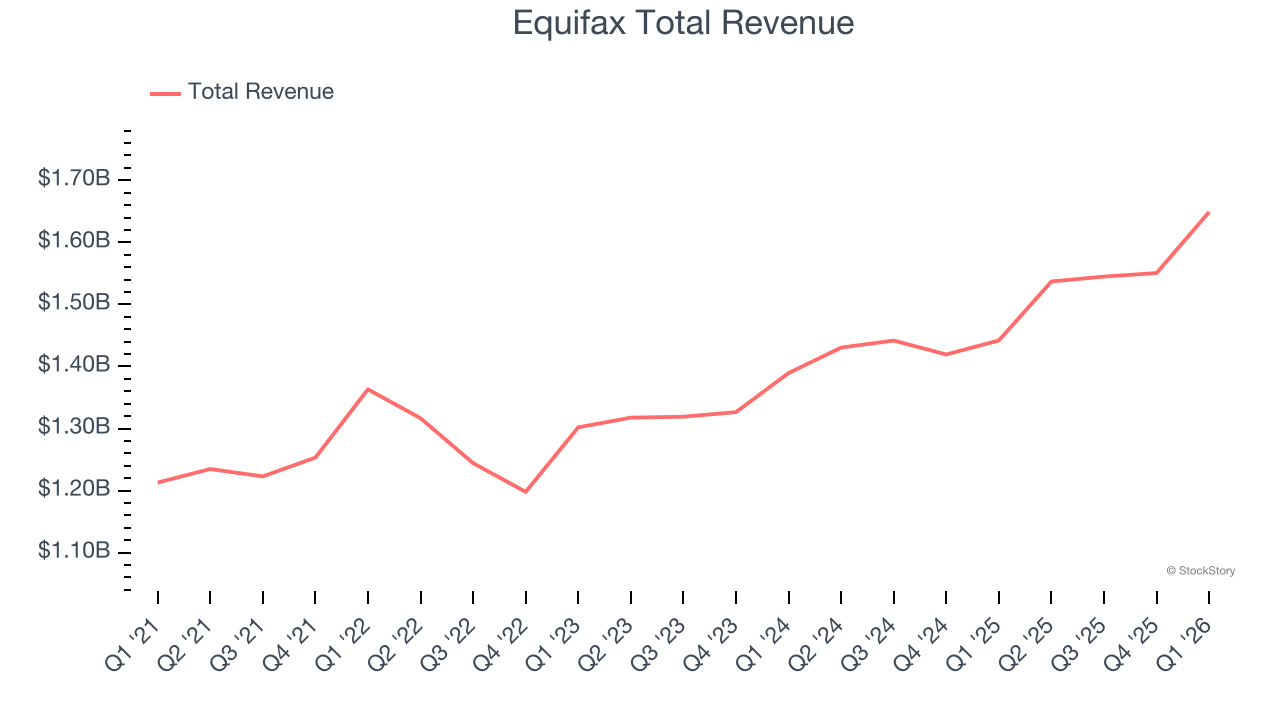

Equifax (NYSE: EFX)

Holding detailed financial records on over 800 million consumers worldwide and dating back to 1899, Equifax (NYSE: EFX) is a global data analytics company that collects, analyzes, and sells consumer and business credit information to lenders, employers, and other businesses.

Equifax reported revenues of $1.65 billion, up 14.3% year on year. This print exceeded analysts’ expectations by 2%. Overall, it was a satisfactory quarter for the company with a beat of analysts’ EPS estimates but a slight miss of analysts’ full-year EPS guidance estimates.

"Equifax delivered a very strong first quarter performance executing on our EFX2028 Strategic Priorities with reported revenue of $1.649 billion, up a strong 14%, with 13% local currency revenue growth which was $37 million above the midpoint of our February guidance." said Mark W. Begor, Equifax Chief Executive Officer.

Even though it had a relatively good quarter, the market seems discontent with the results. The stock is down 13.7% since reporting and currently trades at $171.18.

Is now the time to buy Equifax? Access our full analysis of the earnings results here, it’s free.

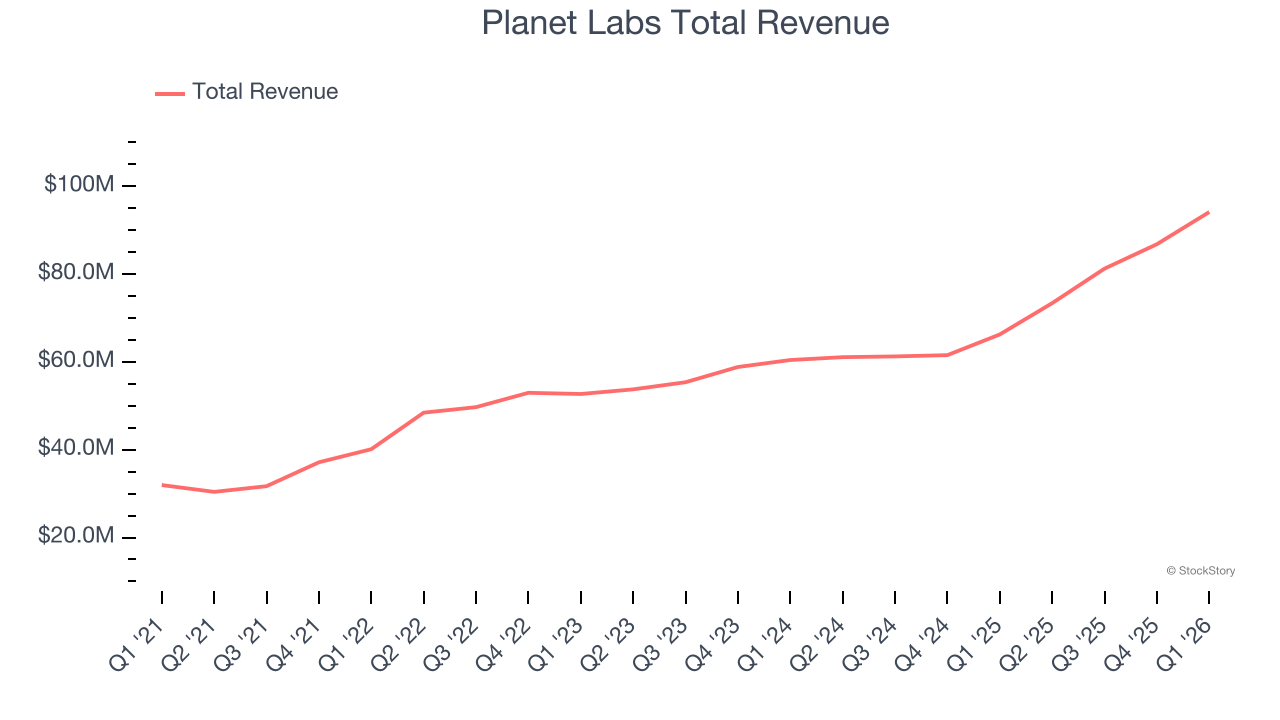

Best Q1: Planet Labs (NYSE: PL)

Pioneering the concept of "agile aerospace" with hundreds of small but powerful satellites, Planet Labs (NYSE: PL) operates the world's largest fleet of Earth observation satellites, capturing daily images of our planet to provide insights on deforestation, agriculture, and climate change.

Planet Labs reported revenues of $94.15 million, up 42.1% year on year, outperforming analysts’ expectations by 4.3%. The business had an exceptional quarter with a beat of analysts’ EPS estimates and revenue guidance for next quarter exceeding analysts’ expectations.

Planet Labs pulled off the fastest revenue growth and highest full-year guidance raise among its peers. Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 3.1% since reporting. It currently trades at $42.19.

Is now the time to buy Planet Labs? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: TransUnion (NYSE: TRU)

One of the three major credit bureaus in the United States alongside Equifax and Experian, TransUnion (NYSE: TRU) is a global information and insights company that provides credit reports, fraud prevention tools, and data analytics to help businesses make decisions and consumers manage their financial health.

TransUnion reported revenues of $1.25 billion, up 13.7% year on year, exceeding analysts’ expectations by 2.7%. Still, it was a mixed quarter as it posted a miss of analysts’ full-year EPS guidance estimates.

The stock is flat since the results and currently trades at $70.49.

Read our full analysis of TransUnion’s results here.

Fair Isaac Corporation (NYSE: FICO)

Creator of the three-digit number that can determine whether you get a mortgage or credit card, Fair Isaac Corporation (NYSE: FICO) develops analytics software and the widely used FICO Score, which is the standard measure of consumer credit risk in the United States.

Fair Isaac Corporation reported revenues of $691.7 million, up 38.7% year on year. This result beat analysts’ expectations by 9.1%. It was a very strong quarter as it also logged an impressive beat of analysts’ ARR estimates.

Fair Isaac Corporation pulled off the biggest analyst estimate beat but had the weakest full-year guidance update among its peers. The stock is up 15.1% since reporting and currently trades at $1,163.

Read our full, actionable report on Fair Isaac Corporation here, it’s free.

CoStar (NASDAQ: CSGP)

With a research department that makes over 10,000 property updates daily to its 35-year-old database, CoStar Group (NASDAQ: CSGP) provides comprehensive real estate data, analytics, and online marketplaces for commercial and residential properties in the U.S. and U.K.

CoStar reported revenues of $897 million, up 22.5% year on year. This number met analysts’ expectations. Overall, it was a strong quarter as it also produced a beat of analysts’ EPS estimates and an impressive beat of analysts’ EPS guidance for next quarter estimates.

CoStar had the weakest performance against analyst estimates among its peers. The stock is down 5.9% since reporting and currently trades at $33.85.

Read our full, actionable report on CoStar here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.