Shareholders of Array would probably like to forget the past six months even happened. The stock dropped 39.9% and now trades at $34.73. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Array, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think Array Will Underperform?

Even though the stock has become cheaper, we’re swiping left on Array for now. Here are three reasons why there are better opportunities than AD, plus one stock we’d rather own.

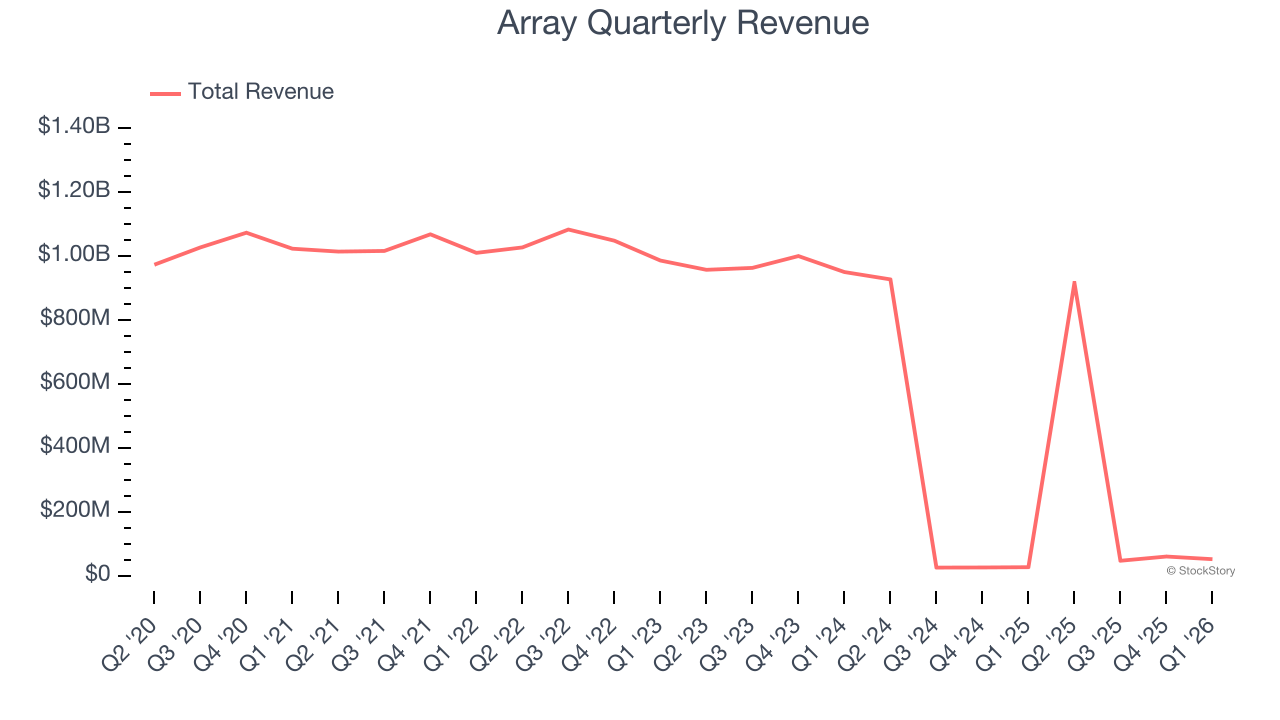

1. Revenue Spiraling Downwards

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Array’s demand was weak over the last five years as its sales fell at a 23.5% annual rate. This wasn’t a great result and signals it’s a low quality business.

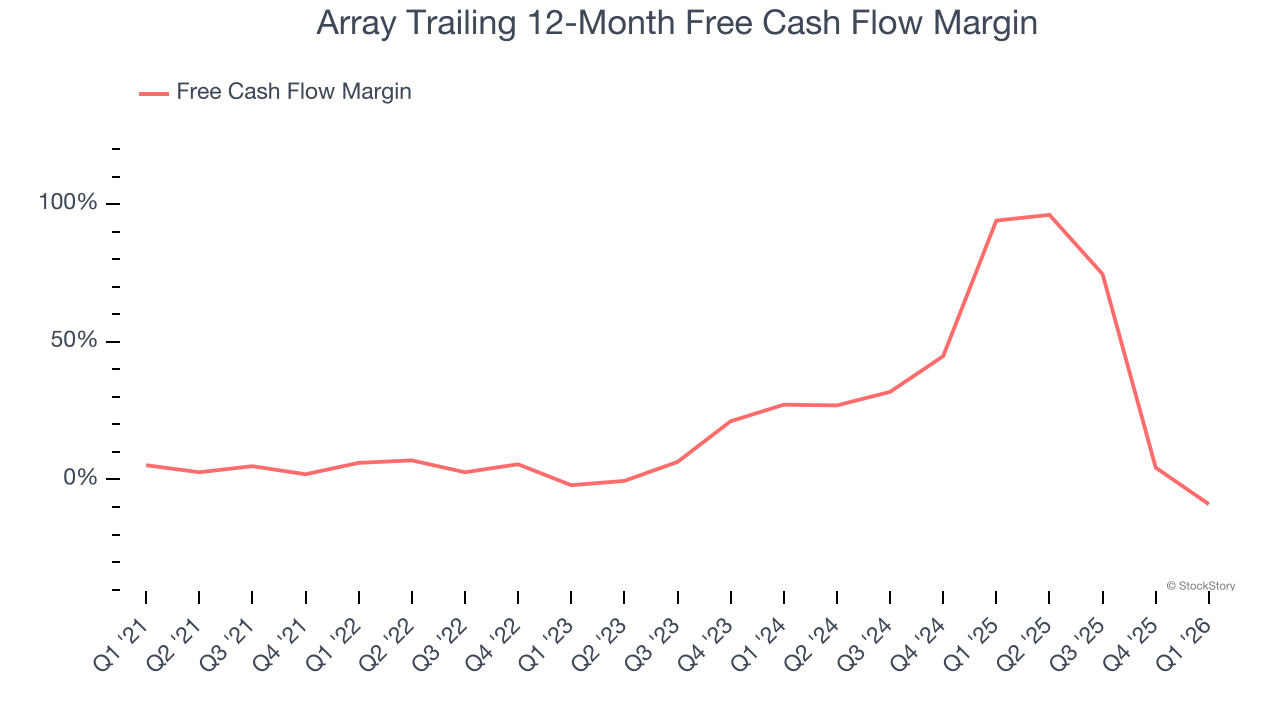

2. Free Cash Flow Margin Dropping

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Array’s margin dropped by 15 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Array’s free cash flow margin for the trailing 12 months was negative 9%.

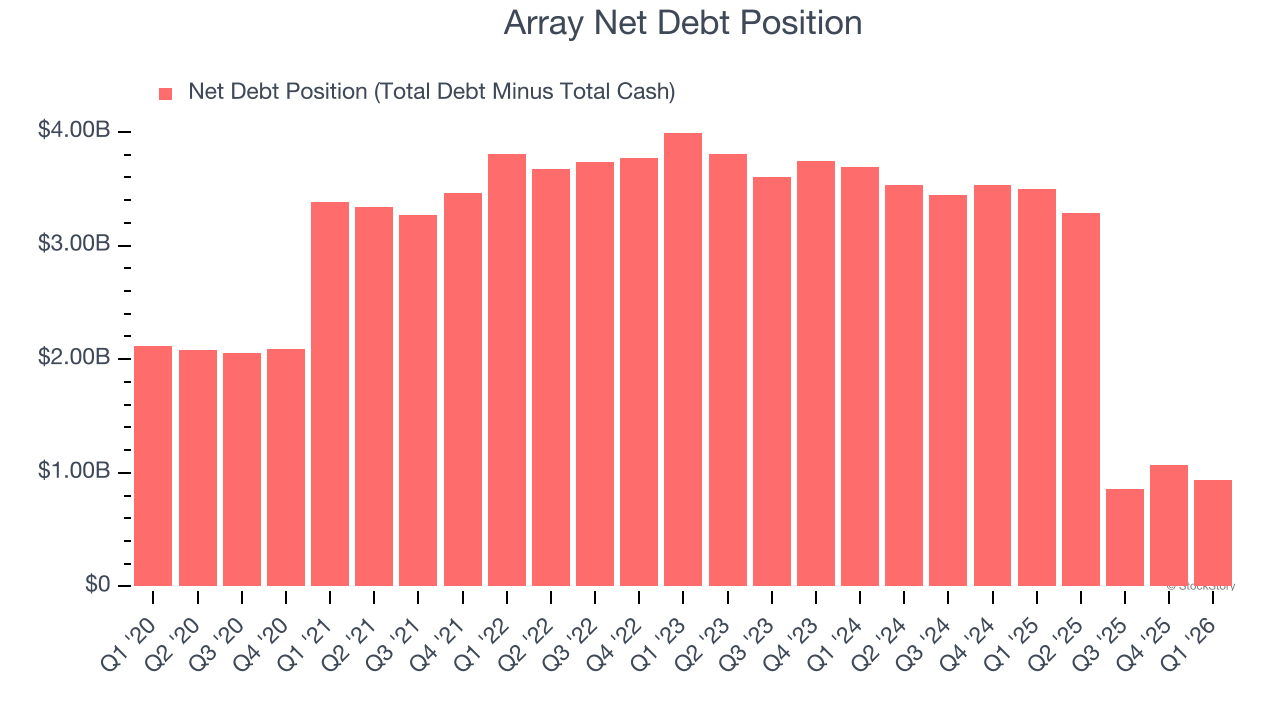

3. High Debt Levels Increase Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Array has $253.6 million of cash and $1.19 billion of debt on its balance sheet. Two things are particularly relevant here for investors in high-quality companies: 1) that debt levels aren’t too high and 2) that interest payments are not excessively burdening the business.

With $2 million of EBITDA over the last 12 months, Array’s net-debt-to-EBITDA ratio sits at 466.3x, showing it is overleveraged. We also view its annual interest payments of $29.76 million as high enough to hinder the performance of the business.

If the company’s profitability falls or the market turns unexpectedly, credit agencies could downgrade the company’s rating, making incremental borrowing more expensive and restricting growth prospects. We believe this puts Array in a risky situation, something we seek to avoid. We hope Array can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

Final Judgment

We see the value of companies helping their customers, but in the case of Array, we’re out. Following the recent decline, the stock trades at 19× forward EV-to-EBITDA (or $34.73 per share). This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere. Let us point you toward one of our all-time favorite software stocks.

Stocks We Would Buy Instead of Array

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,460% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,552% between June 2020 and June 2025). Find your next big winner with StockStory today.