October 13, 2025 – The financial landscape for millions of American retirement savers has undergone a significant transformation throughout 2025, as a pronounced shift from equity-based investments towards more conservative asset classes like bonds, stable value funds, and money market funds has taken hold. This move, driven by a cocktail of market volatility, economic uncertainties, and geopolitical concerns, marks the most dramatic reallocation of 401(k) assets since the market disruptions of October 2020. The immediate implications for financial markets include downward pressure on stock valuations, increased demand for fixed income, and heightened overall market volatility as retirement savers prioritize capital preservation over aggressive growth.

This widespread de-risking by 401(k) participants signals a collective anxiety about the future, potentially leading to suboptimal long-term returns for those who lock in losses and miss subsequent market rebounds. However, it also reflects a pragmatic response to an environment where high interest rates have made conservative fixed-income assets more attractive, offering a tangible yield not seen in years.

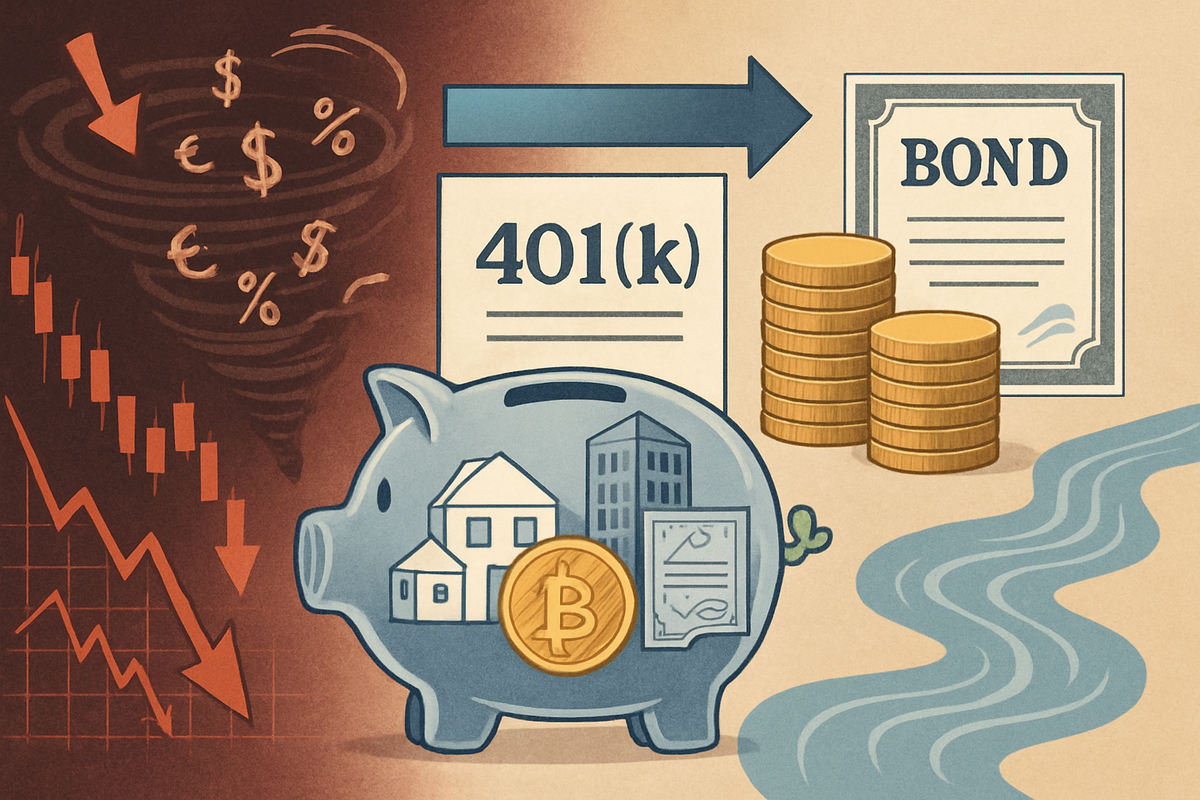

Detailed Coverage: The Great 401(k) Rebalancing of 2025

The shift in 401(k) investor behavior became acutely evident in March 2025, with trading activity surging to levels reminiscent of the early COVID-19 market crash. This elevated activity persisted throughout the second quarter of the year, with data from Alight Solutions indicating that on 40 out of 61 trading days in Q2, investors actively moved funds out of equities. The primary outflows were observed from target-date funds, large-cap U.S. stock funds, mid-cap equities, U.S. small-cap equity funds, and company stock.

These divested funds were largely redirected into more secure havens: bond funds absorbed a striking 42% of Q2 inflows, while stable value funds accounted for 40% of March's total trading inflows, alongside significant allocations to money market funds. This widespread preference for capital preservation represented the largest such tilt in half a decade. While a substantial portion of investors actively rebalanced, it is notable that not all participated; Vanguard reported that 97% of its 401(k) participants did not trade at all in 2025, adhering to a "set-it-and-forget-it" approach, often within target-date funds.

The timeline leading to this moment was characterized by significant market events. Late 2024 saw the IRS announce increased 401(k) contribution limits for 2025, alongside the implementation of SECURE 2.0 Act provisions like automatic enrollment. However, Q1 2025 brought "choppy markets," "tariff-induced volatility," and broader economic uncertainties, unsettling investors. A notable market correction in April 2025, with the S&P 500 Index experiencing a nearly 19% drop, intensified anxiety. Despite a strong market recovery by July, 401(k) investors continued their lean towards conservative investments in August. A pivotal development in August 2025 was an Executive Order (EO) titled "Democratizing Access to Alternative Assets for 401(k) Investors," aiming to broaden investment options to include private equity, real estate, and digital assets.

Key players in this evolving landscape include the millions of 401(k) plan participants, particularly affluent investors who were sensitive to market fluctuations. Data providers and research firms like Alight Solutions, Vanguard, and Janus Henderson provided critical insights. Financial advisors played a vital role in guiding investors, while government and regulatory bodies, including the IRS, Department of Labor (DOL), and the Securities and Exchange Commission (SEC), shaped the rules. Asset management and retirement services providers such as BlackRock (NYSE: BLK) and Empower began integrating or planning to incorporate private assets, anticipating regulatory shifts. Initial market reactions included widespread "panic" selling among some investors, followed by concerns about "opportunity costs" as markets recovered. The executive order on private assets generated considerable industry discussion, seen as unlocking a "$12 trillion opportunity" for institutional investors, though a "striking disconnect" between investor demand and institutional barriers remained.

Winners and Losers: Companies Navigating the Asset Shift

The pronounced shift of 401(k) investors towards more conservative assets, coupled with the rising interest rate environment of 2025, creates clear winners and losers among public companies.

Companies Poised to Win: Asset managers with robust fixed-income offerings stand to gain significantly. Firms like BlackRock (NYSE: BLK), Vanguard, Fidelity, and PIMCO (a subsidiary of Allianz SE - XTRA: ALV), with their extensive range of bond funds and fixed-income ETFs, will see increased Assets Under Management (AUM) and, consequently, higher management fees. Similarly, providers of money market funds will benefit from inflows into cash and cash equivalents, especially as higher interest rates make these funds more attractive. Banks and other financial institutions also stand to gain, as higher interest rates improve their net interest margins, and increased allocations to cash translate into more deposits. Insurance companies, which typically hold large bond portfolios, will see improved investment income from better-yielding new bond investments.

Companies Facing Headwinds: Conversely, asset managers primarily focused on equity funds (e.g., large-cap, small-cap, growth, value) will likely experience decreased AUM as investors withdraw from these products, directly impacting their fee income and profitability. Brokerage firms with significant equity trading desks may see reduced trading volumes and, thus, lower commission and trading fee revenue. Publicly traded companies, especially those reliant on equity financing, could also face challenges. A broad shift out of stocks can depress overall market valuations, making it more expensive for companies to raise capital through new stock offerings, affecting employee stock options, and potentially signaling reduced investor confidence.

Considering the current date of October 2025, the elevated interest rate environment makes the shift to conservative assets more impactful for bond-related companies. The ongoing evolution of target-date funds, which automatically de-risk over time, further reinforces this trend. While recession fears have surfaced, a generally steady economy with solid corporate margins has been observed, though market concerns about macroeconomic and political environments continue to fuel risk-averse sentiment. The growing interest in retirement income solutions also aligns with increased allocations to more stable assets as individuals approach or enter retirement.

Wider Significance: A Paradigm Shift in Retirement Investing

The 401(k) asset shift of 2025 is not merely a reactive response to market conditions; it's a critical indicator of broader, evolving trends in retirement investing. This event highlights a dual movement: a reactive flight to traditional conservative assets and a proactive, policy-driven push towards integrating alternative assets.

The reactive shift to traditional conservative assets in Q2 2025, moving from equities to fixed income, mirrors historical investor behavior during periods of market stress, such as the COVID-19 crash in October 2020. This pro-cyclical investment behavior, where contributions dip during downturns and accelerate during booms, is a consistent pattern globally. However, a significant counter-trend is the burgeoning demand for alternative assets like private equity, private credit, real estate, and even cryptocurrencies within 401(k) plans. Surveys, such as Schroders' "2025 U.S. Retirement Survey," indicate nearly half of 401(k) participants would invest in private assets for diversification and enhanced returns. This suggests an evolution of diversification strategies, moving beyond traditional stocks and bonds, a practice previously common only among institutional investors.

This dual movement has significant ripple effects. For asset managers, the opening of 401(k) plans to alternative assets presents a massive opportunity, prompting firms like BlackRock (NYSE: BLK), Empower, and Goldman Sachs to integrate these into target-date funds. This will intensify competition and likely lead to increased fees, raising concerns about a "silent partner problem" where intermediaries extract substantial wealth. Plan sponsors and recordkeepers face increased responsibilities and potential litigation risks under ERISA, demanding enhanced due diligence and robust platforms for less liquid assets. Financial advisors will become even more crucial in educating investors on these complex new options. A sustained shift of 401(k) capital towards private markets could also reduce inflows into public equities, altering market dynamics.

Regulatory and policy implications are profound. President Trump's August 2025 executive order, directing the DOL and SEC to re-examine guidance limiting access to alternative assets, is a pivotal development. While aiming to "relieve regulatory burdens," this order does not fundamentally alter ERISA fiduciary duties, meaning plan sponsors must still prudently select and monitor these potentially volatile assets, magnifying legal exposure if not managed correctly. The DOL is expected to issue updated guidance, potentially rescinding previous crypto warnings. The ongoing implementation of the SECURE 2.0 Act also continues to shape retirement savings, with provisions like mandatory automatic enrollment increasing participation.

What Comes Next: Navigating the Future of 401(k) Allocations

The future of 401(k) asset allocation is poised for significant evolution, characterized by both continued risk mitigation and a gradual, strategic integration of alternative assets.

In the short term (1-3 years), the emphasis on risk mitigation is likely to persist. While interest rate cuts may be on the horizon in late 2025 or early 2026 as inflation moderates, the cautious sentiment among 401(k) investors, evident in their Q2 2025 shifts, is unlikely to dissipate entirely. The initial integration of alternative assets will likely focus on multi-asset class vehicles like target-date funds, offering diversification without requiring direct participant selection. Major providers like Vanguard and State Street (NYSE: STT) have already announced plans to offer private equity in 401(k)s, with BlackRock (NYSE: BLK) aiming for private investments in target-date funds by mid-2026.

Long term (3+ years), alternative assets are expected to become a defining feature of retirement savings, driven by their potential for higher returns, enhanced diversification, and inflation protection. Demographic shifts, with younger generations more open to diverse asset classes, including digital assets, will accelerate this adoption. Target-date funds will continue to evolve, incorporating active and passive blends, alongside real assets and alternatives. Investors will need to re-evaluate their risk tolerance, educate themselves on the complexities of alternatives (illiquidity, higher fees, valuation challenges), and seek professional guidance from fiduciary advisors. Plan sponsors must adapt by broadening investment menus, enhancing due diligence, and providing transparent communication to participants.

Market opportunities include enhanced diversification and returns from alternatives, access to new growth sectors, and product innovation from financial firms. However, challenges such as illiquidity, complex valuations, higher fees, and increased fiduciary/litigation risk for plan sponsors remain. Potential scenarios range from a gradual, controlled shift where alternatives are primarily integrated through managed solutions, to a rapid acceleration driven by market downturns. A strong possibility is the dominance of "hybrid default solutions" like target-date funds, strategically blending traditional, active fixed income, and vetted alternative assets, providing diversified exposure without active selection.

The Road Ahead: A Comprehensive Wrap-up for Retirement Savers

The year 2025 has been a pivotal period for 401(k) investors, marked by a decisive shift towards conservative assets in response to market volatility and economic uncertainties. This trend, while driven by a desire for safety, also highlights a potential disconnect between short-term emotional reactions and long-term investment goals, especially given the historical outperformance of equities over extended periods.

Moving forward, the market outlook is cautiously optimistic, with projected economic growth and strong corporate earnings, particularly for mega-cap technology firms driven by the AI revolution. The Federal Reserve is anticipated to implement rate cuts as inflation moderates in late 2025 or early 2026, though long-term bond yields may face upward pressure from global fiscal policies. Geopolitical and policy uncertainties, especially regarding trade and taxes, will remain significant market drivers. The record inflows into gold and cryptocurrencies in 2025 underscore a growing "debasement trade" as investors seek hedges against perceived government debt and a potentially weakening U.S. dollar.

The lasting impact of 2025 will be the fundamental re-evaluation of risk and return in retirement planning. The paradox of investors seeking safety while also expressing interest in alternative assets underscores the need for robust financial education. The structural transformation towards potentially expanded access to private assets and cryptocurrencies within 401(k) plans will introduce new complexities and fiduciary responsibilities, fundamentally reshaping the risk-reward calculus for retirement portfolios. Furthermore, the "retailification" of public markets is a lasting trend, with individual investors demanding greater transparency and tailored solutions.

What Investors Should Watch For in Coming Months:

- Q4 2025 Earnings and 2026 Guidance: Pay close attention to corporate performance, especially in AI-linked sectors, for insights into future growth.

- Federal Reserve Policy and Inflation Data: Monitor inflation figures and Fed communications for signals on interest rate cuts, which will impact both fixed-income and equity markets.

- Geopolitical and Trade Policy Developments: Stay informed about policy changes from the incoming presidential administration, particularly concerning taxes and international trade, which could introduce volatility.

- Regulatory Guidance on 401(k) Private Assets: Watch for concrete guidance from the DOL and SEC regarding the inclusion of private equity and other alternative assets in 401(k) plans, which could open new avenues for diversification.

- Retail Investor Sentiment and Flows: Observe retail investor activity, especially in high-momentum sectors, as it can indicate market enthusiasm and potential areas of concentrated risk.

By staying informed and thoughtfully reviewing their asset allocations, 401(k) investors can navigate the evolving market landscape and align their retirement strategies with their long-term financial objectives.

This content is intended for informational purposes only and is not financial advice