The global financial landscape is currently grappling with a potent mix of escalating geopolitical tensions and economic uncertainty, driving unprecedented volatility across major asset classes. Gold and silver prices have surged to historic levels, propelled by a renewed and aggressive phase of the US-China trade war, which is sending shockwaves through global stock markets and injecting fresh instability into the once-surging Bitcoin market. As of October 14, 2025, investors are flocking to traditional safe havens, reflecting deep concerns about inflation, supply chain disruptions, and the long-term implications of a fractured global economy.

This dramatic shift underscores a fundamental repricing of risk, as the world's two largest economies engage in a tit-for-tat escalation of tariffs and export restrictions. The ripple effects are profound, forcing companies to re-evaluate supply chains, central banks to reconsider monetary policy, and investors to navigate a treacherous path marked by both peril and potential opportunity. The current environment signals a challenging period for growth-oriented assets and a robust endorsement for precious metals as hedges against a turbulent future.

Escalating Trade Tensions Fuel Commodity Rally and Market Disarray

The catalyst for the recent market upheaval is the significant re-escalation of the US-China trade war, which has transformed into what analysts are terming a "supply-chain siege." On October 9, 2025, China initiated new export restrictions on critical rare earths, production equipment, materials, and associated technologies, citing national security. This strategic move was swiftly met with retaliation from the United States. On October 10, US President Donald Trump announced plans for sweeping 100% tariffs on a broad range of Chinese imports, effective November 1, in addition to existing levies. Furthermore, the US declared new export controls on "any and all critical software," widening the scope of economic warfare. Both nations also imposed new tit-for-tat port fees on each other's shipping, demonstrating a clear intent to weaponize every aspect of their economic interaction. China, while expressing openness to negotiation, declared its readiness to "fight to the end" if the US continued to escalate.

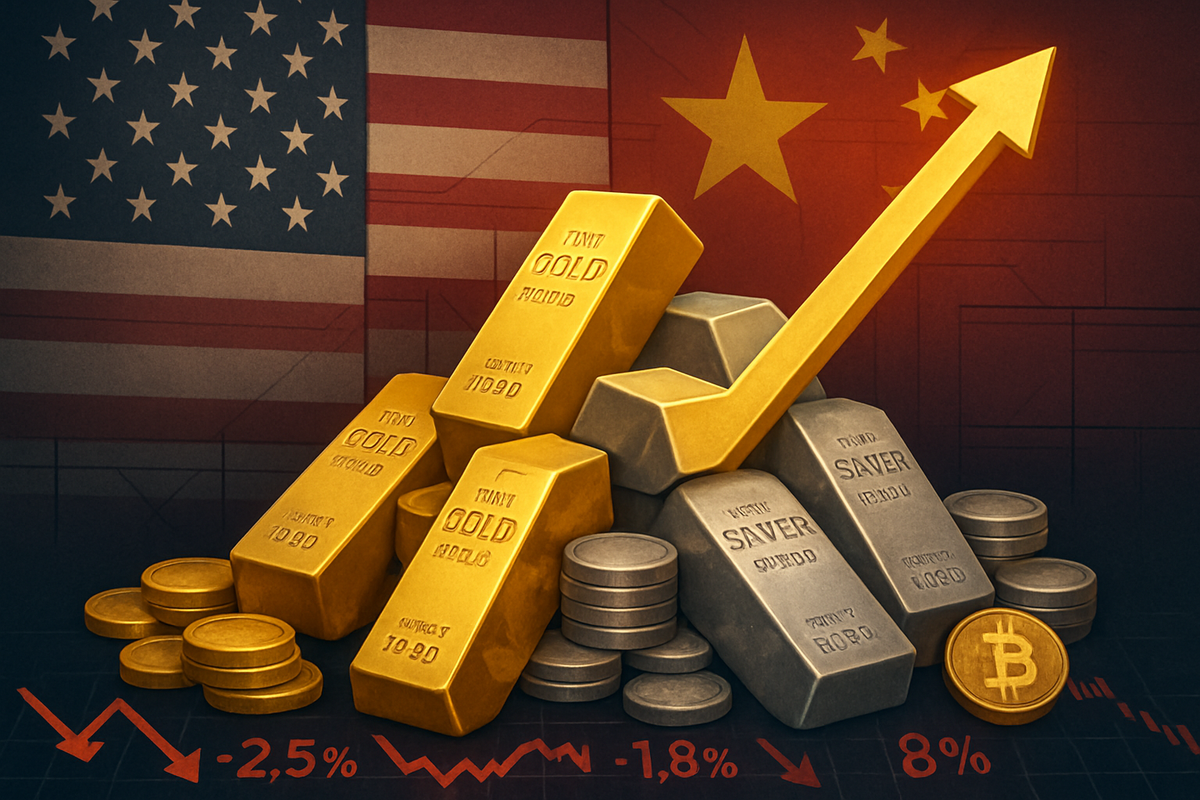

This aggressive posture has sent investors scrambling for safety. Gold (XAU) prices soared to an all-time high of $4,179.48 per ounce, trading around $4,105.90 on October 14, marking an 11.59% increase over the past month and a staggering 54.33% rise year-on-year. Silver (XAG) has mirrored this ascent, reaching a new record of $52.58 per ounce in London markets, surpassing its 1980 peak, and trading around $50.54 per troy ounce. This represents an 18.40% monthly gain and a 60.63% annual increase. The surge in precious metals is attributed to growing expectations of US Federal Reserve rate cuts, persistent inflation concerns, increased central bank purchases, and their traditional role as a hedge against geopolitical risks and currency debasement. Analysts now project gold could average $3,675/oz by Q4 2025 and potentially reach $4,000/oz by Q2 2026. Silver's rally is further bolstered by robust industrial demand, particularly in green technologies like solar panels and electric vehicles, coupled with severe supply deficits and rapidly declining inventories, leading to a notable "short squeeze" in physical markets.

Global stock markets have reacted with heightened sensitivity to these geopolitical tremors. While underlying fundamentals like modest inflation and growing corporate earnings have provided some support, the re-escalation of the US-China trade war has triggered a pronounced "risk-off" sentiment. Major geopolitical risk events typically lead to declines in stock prices, with emerging markets experiencing more substantial drops. The BlackRock Geopolitical Risk Indicator remains elevated, reflecting ongoing investor attention to these conflicts. Bitcoin (BTC), which had recently surged to a new all-time high above $126,000 in early October due to institutional inflows and regulatory clarity, experienced a sharp retreat, dropping below $112,000 by October 14. The announcement of new US tariffs contributed to a loss of approximately $500 billion in the broader crypto market capitalization, as demand for traditional safe havens like gold temporarily superseded that for digital assets.

Corporate Fortunes: Navigating the Trade War's Crosscurrents

The intensifying US-China trade war and the subsequent commodity price spikes are creating a clear divide between potential winners and losers in the corporate world. Companies involved in the mining and production of precious metals are poised for significant gains. For instance, major gold miners like Barrick Gold Corporation (NYSE: GOLD) and Newmont Corporation (NYSE: NEM), along with silver producers such as Pan American Silver Corp. (NASDAQ: PAAS) and Wheaton Precious Metals Corp. (NYSE: WPM), are likely to see increased revenues and profitability due to the elevated prices of their core products. Their stocks could continue to outperform the broader market as long as safe-haven demand persists and commodity prices remain high.

Conversely, companies heavily reliant on global supply chains, particularly those with significant exposure to both US and Chinese markets, face substantial headwinds. Technology firms, manufacturers, and retailers that source components from China or export finished goods to the country will bear the brunt of the new tariffs and export restrictions. For example, US oilseed exporters, like those representing major agricultural companies such as Archer-Daniels-Midland Company (NYSE: ADM) and Bunge Limited (NYSE: BG), could see their exports to China "wiped out," severely eroding their global trade. This "supply-chain siege" threatens to disrupt production, increase costs, and diminish profit margins for a vast array of businesses, forcing costly and time-consuming efforts to diversify sourcing and manufacturing away from China.

Furthermore, companies in sectors deemed strategically critical by either government, such as advanced manufacturing, semiconductors, and specialized software, could face direct targeting through export controls and restrictions. This could severely limit their access to key markets or essential components, forcing strategic pivots or even divestitures. While some companies might find opportunities in reshoring or nearshoring production, the immediate impact will likely be negative, marked by increased operational complexity and reduced profitability. European economies, however, might experience a nuanced effect, potentially seeing an increase in imports from China as Chinese exporters redirect goods from the US market, which could benefit European importers but create new competitive pressures for local industries.

Broader Implications: A New Era of Economic Nationalism and Volatility

The current financial turbulence, driven by the US-China trade war and commodity surges, signifies more than just a temporary market fluctuation; it heralds a deeper shift towards economic nationalism and strategic competition. This event fits squarely into broader trends of deglobalization and the weaponization of economic tools, where trade, technology, and critical resources are increasingly seen as instruments of national power. The "supply-chain siege" strategy employed by both the US and China underscores a global move away from purely efficiency-driven supply chains towards resilience and national security, a trend that began years ago but has accelerated dramatically.

The potential ripple effects are far-reaching. Beyond immediate market reactions, the prolonged trade war could lead to persistent global inflation, as tariffs increase import costs and supply chain disruptions reduce efficiency. This could force central banks worldwide to maintain higher interest rates for longer, or even initiate new rate hikes, potentially stifling economic growth and increasing the risk of a global recession. For competitors and partners, the situation presents both challenges and opportunities. Nations not directly involved in the trade war might benefit from redirected trade flows or increased foreign direct investment as companies seek alternative manufacturing bases. However, they also face the risk of being caught in the crossfire, particularly if their economies are deeply integrated with either the US or China.

Regulatory and policy implications are profound. Governments are likely to continue enacting protectionist measures, subsidies for domestic industries, and stricter controls over sensitive technologies and resources. This could lead to a more fragmented global trading system, characterized by regional blocs and bilateral agreements rather than multilateral cooperation. Historically, periods of intense geopolitical rivalry and trade protectionism, such as the 1930s, have often led to severe economic downturns. While the current situation is different in many respects, the parallels serve as a stark reminder of the potential for economic nationalism to undermine global prosperity and stability. The ongoing Middle East conflict, involving the US, Israel, and Iran, further compounds these risks, particularly concerning global oil supplies and overall market uncertainty, reinforcing the demand for safe-haven assets.

The Path Forward: Adaptation, Diversification, and Enduring Volatility

Looking ahead, the short-term outlook suggests continued market volatility and uncertainty. Investors should prepare for sustained fluctuations in equity markets, further strength in precious metals, and unpredictable movements in cryptocurrencies like Bitcoin, which remain sensitive to "risk-off" sentiment despite their growing institutional adoption. The immediate focus will be on the next moves from Washington and Beijing. Any signs of de-escalation, even minor ones, could trigger temporary market relief, while further aggressive actions will likely exacerbate current trends. Companies will need to prioritize strategic pivots, including accelerating supply chain diversification, exploring reshoring or nearshoring options, and investing in automation to reduce reliance on vulnerable global links.

In the long term, the global economy is likely to adapt to a more fragmented and nationalistic trading environment. This could lead to the emergence of new market opportunities in sectors focused on domestic production, critical resource security, and advanced manufacturing within national borders. Companies that can successfully navigate the complexities of decoupling supply chains and adapting to new trade barriers will be better positioned for success. For example, firms specializing in logistics, automation, and cybersecurity solutions that enhance supply chain resilience could see increased demand. However, significant challenges remain, including the potential for sustained inflation, slower global growth, and increased geopolitical instability.

Potential scenarios range from a continued "cold trade war" with intermittent escalations and de-escalations, to a more severe decoupling of the US and Chinese economies, leading to distinct economic blocs. The latter scenario would necessitate fundamental shifts in global business models and could dramatically reshape international trade and investment flows. Investors should closely monitor central bank policies, particularly the US Federal Reserve's stance on interest rates, as well as any diplomatic efforts to de-escalate trade tensions. The enduring impact of this period will likely be a more regionalized global economy, where geopolitical considerations play an increasingly dominant role in investment and business decisions, making resilience and adaptability paramount for survival and growth.

Navigating the New Normal: Key Takeaways for Investors

The current financial climate is defined by the powerful interplay of escalating geopolitical tensions and profound economic shifts. The surge in gold and silver prices to all-time highs serves as a stark reminder of their enduring role as safe-haven assets in times of uncertainty, a trend amplified by the renewed intensity of the US-China trade war. This conflict, evolving into a "supply-chain siege," is fundamentally reshaping global trade, disrupting established supply chains, and creating a clear divide between corporate winners and losers. While precious metal miners stand to benefit, companies reliant on seamless global trade, particularly those with deep US-China ties, face significant challenges and the imperative to adapt rapidly.

Moving forward, the market will likely remain highly sensitive to geopolitical developments and central bank policies. The prospect of persistent inflation, driven by tariffs and supply chain inefficiencies, could influence interest rate decisions globally, impacting equity valuations and economic growth. Investors should brace for continued volatility across all asset classes, with a heightened focus on diversification and strategic allocation. The long-term trajectory points towards a more regionalized and nationalistic global economy, where resilience, localized production, and robust risk management will become critical competitive advantages for businesses.

In the coming months, investors should closely watch for any shifts in the US-China trade rhetoric, the actual implementation and impact of new tariffs and export controls, and the response of major central banks to evolving inflation and growth data. The performance of key economic indicators, particularly manufacturing output, trade balances, and inflation rates, will provide crucial insights into the health of the global economy under these new pressures. Ultimately, this period demands a pragmatic and adaptable investment strategy, recognizing that the era of frictionless globalization is giving way to a more complex and geopolitically driven financial landscape.

This content is intended for informational purposes only and is not financial advice