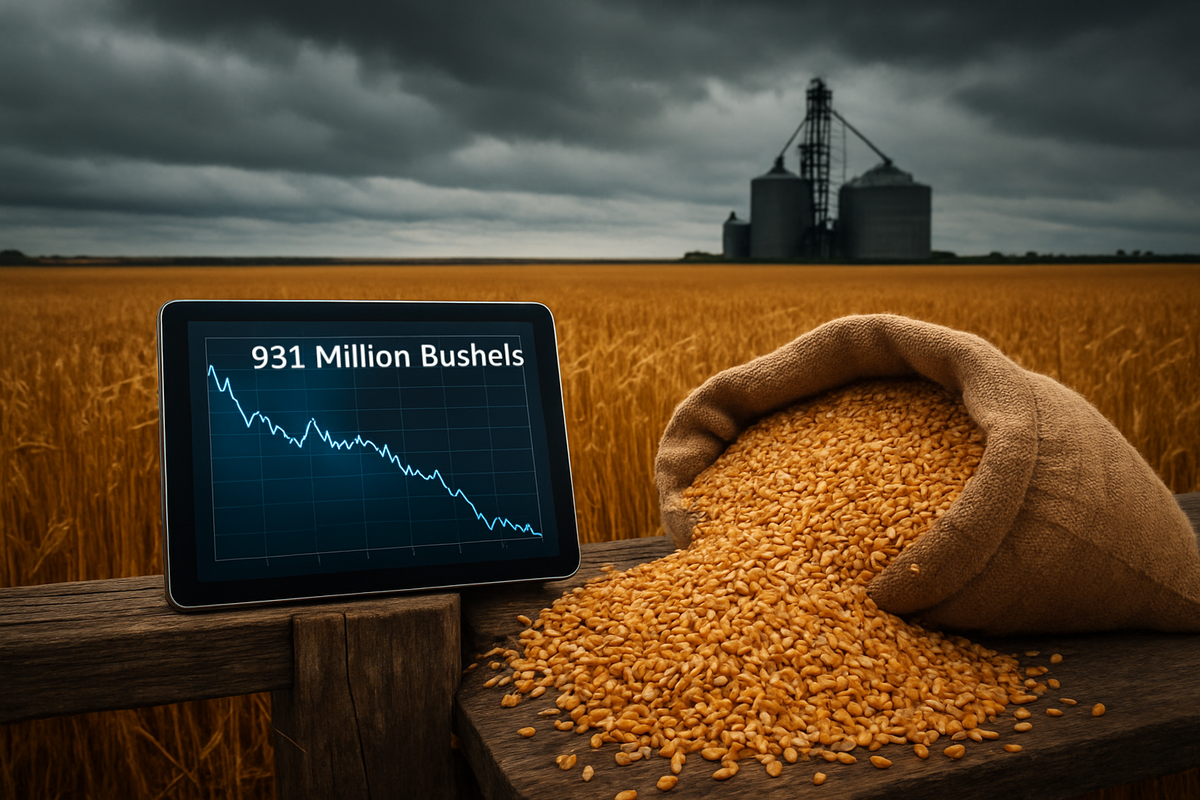

The American wheat market faced a wave of selling pressure this week following the release of the U.S. Department of Agriculture’s (USDA) February World Agricultural Supply and Demand Estimates (WASDE) report. The report, a critical barometer for global food commodities, stunned traders by upwardly revising U.S. wheat ending stocks to a staggering 931 million bushels. This represents the most significant domestic stockpile since the 2019/20 marketing year, signaling a transition from years of tight supply to a period of heavy oversupply.

The immediate implications for the market were swift and decisive. Wheat futures on the Chicago Board of Trade (CBOT) and the Kansas City Board of Trade (KCBT) plummeted in the wake of the news, as the data suggested that domestic demand is failing to keep pace with supply. Despite a reduction in winter wheat acreage—a factor that typically bolsters prices—the combination of sluggish domestic food consumption and a flood of cheap grain from South America has created a "perfect storm" of bearish sentiment for U.S. producers.

Detailed Breakdown of the February WASDE Shock

The headline figure of the February 2026 WASDE report was undoubtedly the 931-million-bushel ending stock projection. To understand how the market reached this point, one must look at the gradual erosion of demand throughout the 2025/26 marketing year. The USDA highlighted a significant "lower-than-expected food use" category, which serves as the backbone of domestic wheat consumption. While population growth usually keeps this number stable, a shift in consumer preferences and a minor slowdown in the commercial baking sector have left more grain in the bins than analysts had anticipated.

The timeline leading to this report began in late 2025, when harvest yields in the Pacific Northwest and the Northern Plains exceeded initial forecasts. While the "Winter Wheat and Canola Seedings" report earlier this year indicated that U.S. farmers had actually reduced winter wheat plantings for the upcoming season, the market has largely ignored this potential future supply tightening. The current surplus is simply too large to overlook. Stakeholders, including the American Farm Bureau and major grain elevators, are now grappling with a market where supply is significantly outstripping the "disappearance" rate.

Compounding the domestic issue is the aggressive competition from international players. The USDA confirmed record-breaking production in Argentina, which has benefited from near-ideal weather conditions during its recent harvest. With Argentina’s wheat flooding the global market at highly competitive prices, U.S. exports have struggled to find a foothold in traditional markets like Southeast Asia and South America. This lack of export "vent" has forced even more grain into domestic storage, further bloating the ending stocks figure.

The Corporate Landscape: Winners and Losers

The shift to a high-supply, low-price environment creates a stark divide between "upstream" producers and "downstream" processors. Consumer packaged goods (CPG) companies are the primary beneficiaries of this trend. General Mills, Inc. (NYSE: GIS) and Mondelez International, Inc. (NASDAQ: MDLZ) are expected to see significant margin expansion in the coming quarters. As major purchasers of flour and wheat derivatives for products ranging from Cheerios to Ritz crackers, lower raw material costs provide these firms with the flexibility to either increase marketing spend or pass savings to shareholders through buybacks.

Conversely, the agricultural machinery and input sectors may face headwinds. Companies like Deere & Company (NYSE: DE) and Corteva, Inc. (NYSE: CTVA) often see a correlation between grain prices and farmer sentiment. With wheat prices languishing near multi-year lows, farmers are less likely to invest in high-end combines or premium seed treatments for the next planting cycle. The "wealth effect" in the rural economy is tied directly to the value of the crop in the silo, and 931 million bushels of low-value wheat suggests a cautious spending environment for 2026.

For the "middlemen" of the industry—the grain originators and traders—the impact is more nuanced. Archer-Daniels-Midland Company (NYSE: ADM) and Bunge Global SA (NYSE: BG) thrive on volatility and "carry." A market with high ending stocks often enters a state of "contango," where future prices are higher than spot prices. This allows these companies to earn reliable income by storing grain in their massive elevator networks and selling it forward. However, the lower outright price of the commodity can reduce the total dollar value of their trading books, making volume and storage efficiency the primary drivers of profit.

Wider Significance and Historical Context

This sudden return to a surplus environment echoes the market dynamics of 2019, just before the global pandemic and subsequent geopolitical conflicts disrupted supply chains. For the past several years, the "scarcity narrative" dominated the wheat market, driven by droughts in the U.S. Plains and the conflict in the Black Sea region. The February 2026 report marks a definitive end to that era, suggesting that global production capacity has finally adjusted to the higher price signals of the early 2020s.

The broader industry trend now shifts toward "demand destruction" and the struggle for export share. The record production in Argentina is a reminder of the increasing volatility and potential of South American agriculture. As Argentina stabilizes its economy and improves its logistical infrastructure, it is becoming a more formidable competitor to U.S. soft red and hard red winter wheat. This puts pressure on U.S. trade policymakers to find new markets or increase the competitiveness of U.S. grain through infrastructure investment.

Furthermore, the "lower-than-expected food use" cited by the USDA may point to a more permanent shift in the American diet. As alternative flours (almond, oat, and chickpea) gain market share and "ultra-processed" foods face increased regulatory and health scrutiny, the traditional wheat-milling industry may be entering a period of structural stagnation. This forces companies to pivot their strategies toward higher-margin, specialty grain products rather than relying on the volume of commodity white flour.

What Comes Next for the Wheat Market?

In the short term, the market will keep a close eye on "winterkill" reports. While the current stocks are high, a major weather disaster in the U.S. Central Plains during the spring could quickly change the narrative. However, given the 931-million-bushel cushion, it would take a historic crop failure to move the needle back toward a deficit. Investors should expect wheat prices to remain in a sideways-to-lower trading range through the first half of 2026.

Strategically, U.S. farmers may continue to pivot away from wheat in the next planting cycle, favoring crops like soybeans or corn if the price ratios remain unfavorable. This "acreage war" will be the primary focus of the USDA’s Prospective Plantings report in March. If the industry sees a massive flight from wheat, it could set the stage for a price recovery in late 2027, but that is a long-term prospect that provides little comfort to producers today.

Market opportunities may emerge in the "spread" between different classes of wheat. With soft wheat in high supply, hard wheat—which has higher protein and is essential for bread making—might maintain a premium. Sophisticated traders will likely look to exploit these quality-based price differences as the 2026 growing season progresses.

Summary and Final Assessment

The February WASDE report has redefined the 2026 agricultural outlook, replacing fears of shortage with the reality of a glut. The jump to 931 million bushels in ending stocks, fueled by record Argentinian harvests and tepid domestic food demand, has placed a firm lid on wheat prices. While this is a boon for consumer-facing giants like General Mills and Mondelez, it presents a significant challenge for the American farmer and the companies that supply them.

Moving forward, the market’s focus will shift from "how much do we have?" to "how can we move it?" The ability of the U.S. to compete in a crowded global export market will be the defining factor for the remainder of the year. Investors should watch for the March planting intentions and any shifts in South American export taxes or policies that could further impact the global supply balance. For now, the "Wheat King" remains under heavy pressure, and the surplus is likely here to stay.

This content is intended for informational purposes only and is not financial advice.