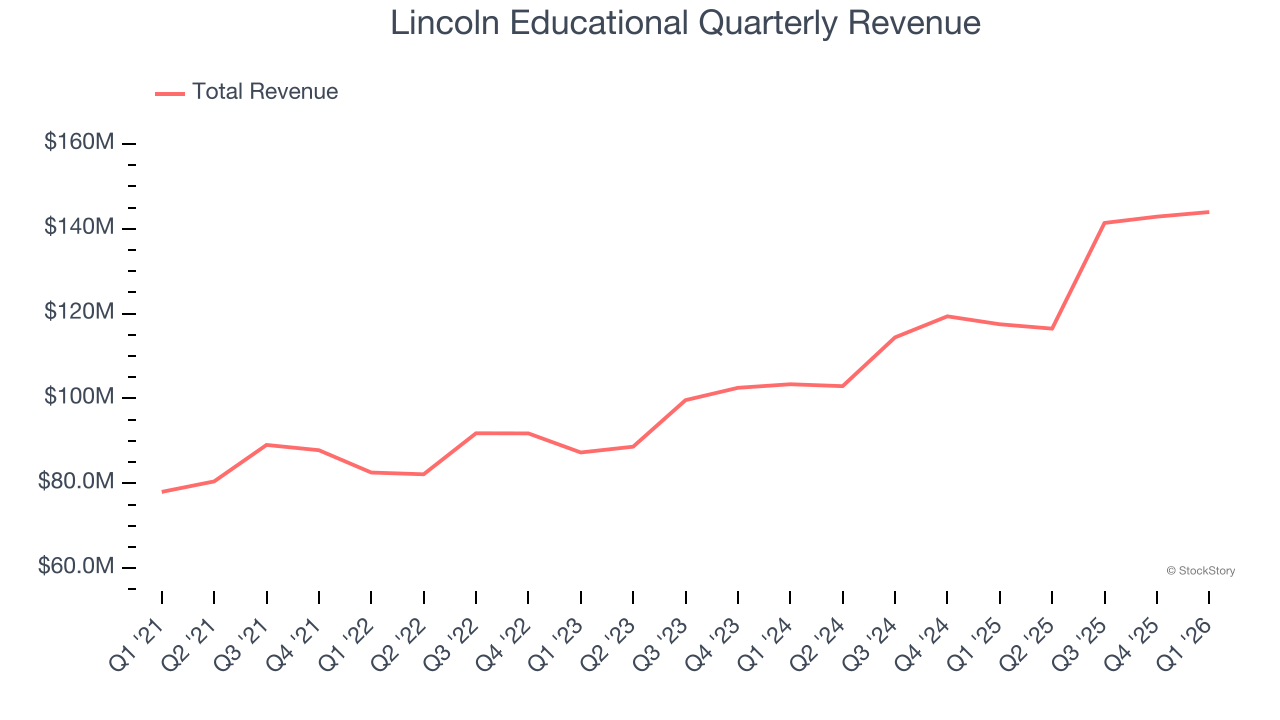

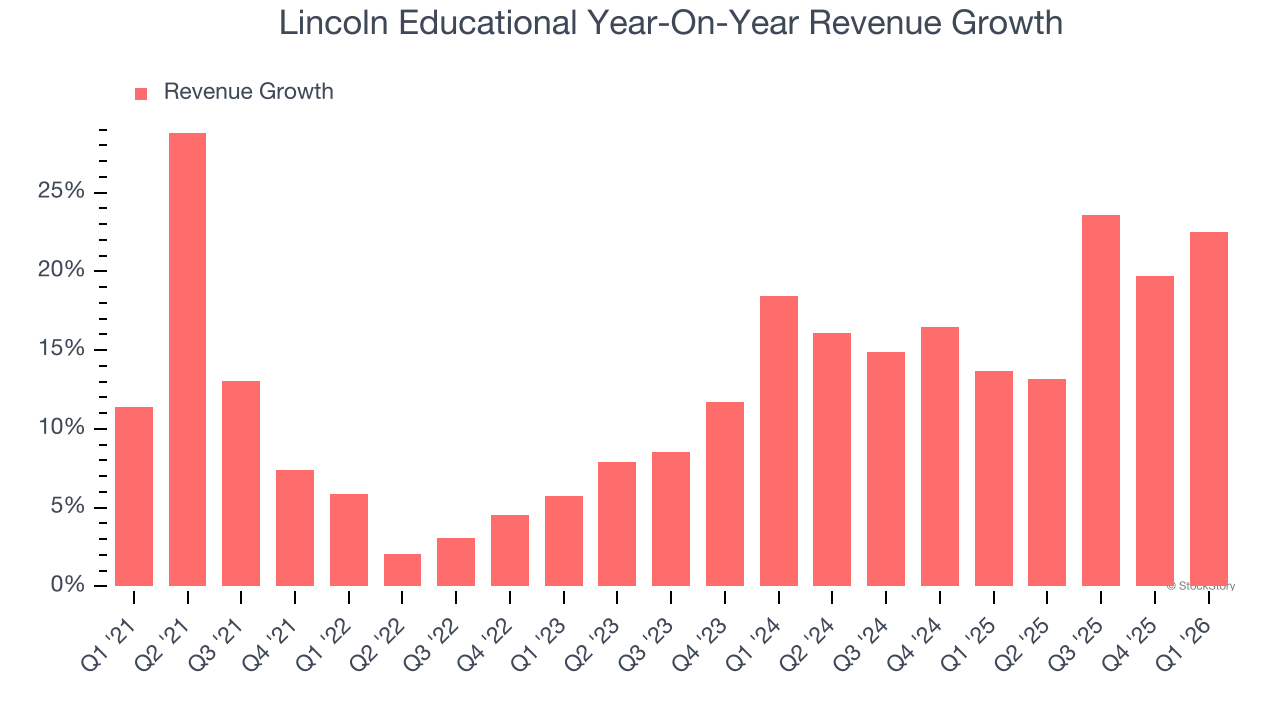

Education company Lincoln Educational (NASDAQ: LINC) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 22.5% year on year to $144 million. The company’s full-year revenue guidance of $595 million at the midpoint came in 1.8% above analysts’ estimates. Its GAAP profit of $0.14 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Lincoln Educational? Find out by accessing our full research report, it’s free.

Lincoln Educational (LINC) Q1 CY2026 Highlights:

- Revenue: $144 million vs analyst estimates of $136.2 million (22.5% year-on-year growth, 5.7% beat)

- EPS (GAAP): $0.14 vs analyst estimates of $0.04 (significant beat)

- Adjusted EBITDA: $15.48 million vs analyst estimates of $12.39 million (10.8% margin, 25% beat)

- The company lifted its revenue guidance for the full year to $595 million at the midpoint from $585 million, a 1.7% increase

- EPS (GAAP) guidance for the full year is $0.78 at the midpoint, beating analyst estimates by 13.8%

- EBITDA guidance for the full year is $78 million at the midpoint, above analyst estimates of $74.12 million

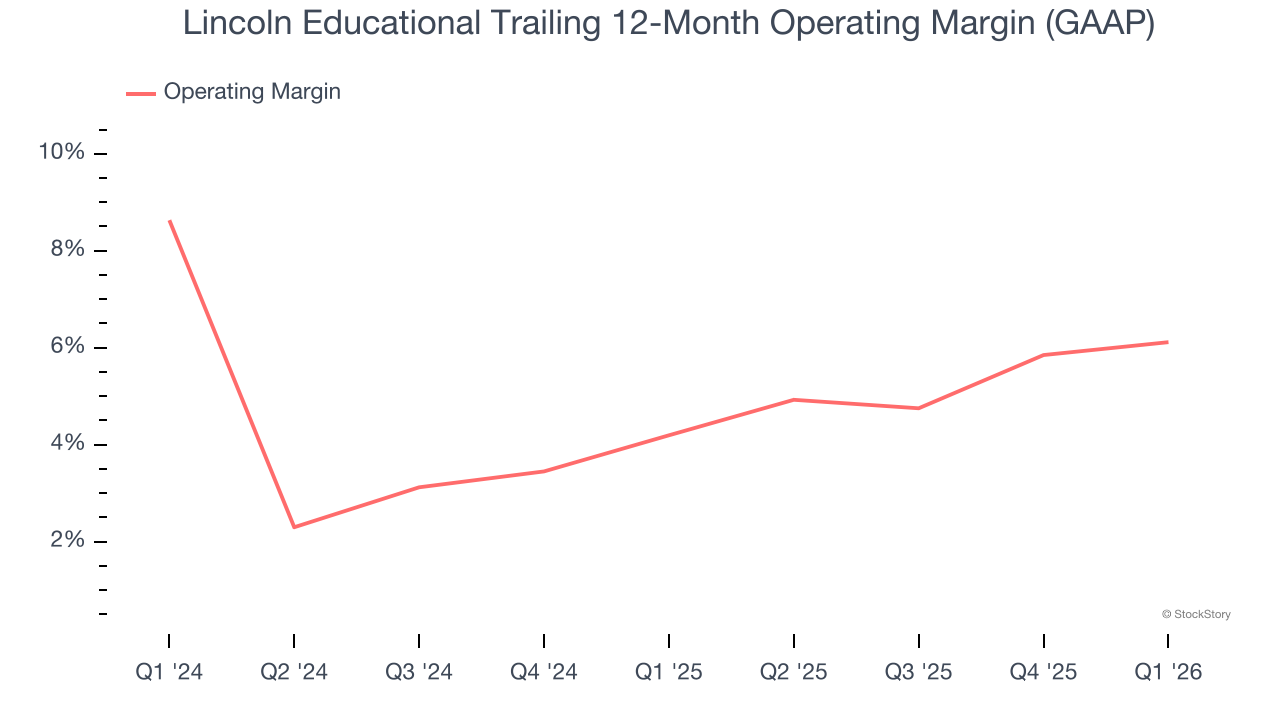

- Operating Margin: 4.5%, up from 2.9% in the same quarter last year

- Free Cash Flow was -$10.06 million compared to -$28.27 million in the same quarter last year

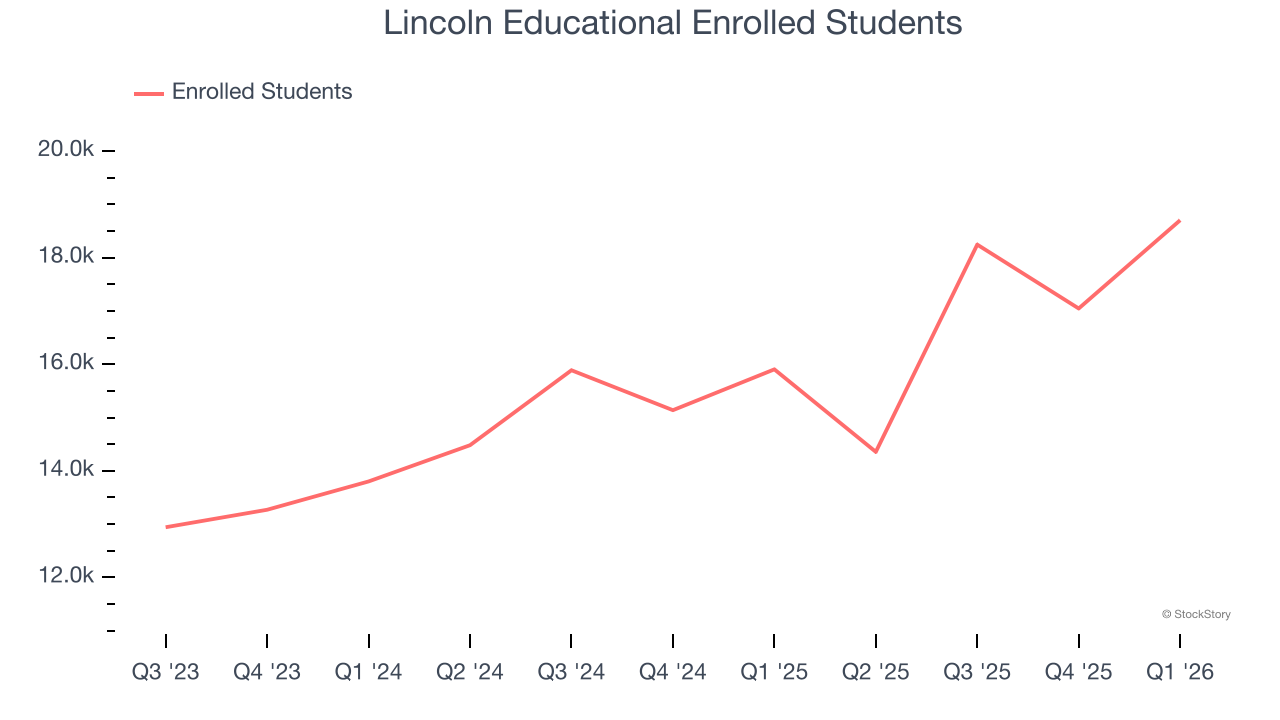

- Enrolled Students: up 2,798 year on year

- Market Capitalization: $1.42 billion

“The first quarter financial and operating results illustrate the substantial progress made towards achieving our objective of providing the best education and training for in-demand careers while generating consistent, increasing returns to our shareholders,” said Scott Shaw, CEO and President.

Company Overview

Established in 1946, Lincoln Educational (NASDAQ: LINC) is a provider of specialized technical training in the United States, offering career-oriented programs to provide practical skills required in the workforce.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Lincoln Educational grew its sales at a 12.6% compounded annual growth rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Lincoln Educational’s annualized revenue growth of 17.6% over the last two years is above its five-year trend, which is encouraging.

Lincoln Educational also discloses its number of enrolled students, which reached 18,702 in the latest quarter. Over the last two years, Lincoln Educational’s enrolled students averaged 13.7% year-on-year growth. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, Lincoln Educational reported robust year-on-year revenue growth of 22.5%, and its $144 million of revenue topped Wall Street estimates by 5.7%.

Looking ahead, sell-side analysts expect revenue to grow 9.7% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will face some demand challenges.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Lincoln Educational’s operating margin has risen over the last 12 months and averaged 5.2% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

In Q1, Lincoln Educational generated an operating margin profit margin of 4.5%, up 1.5 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

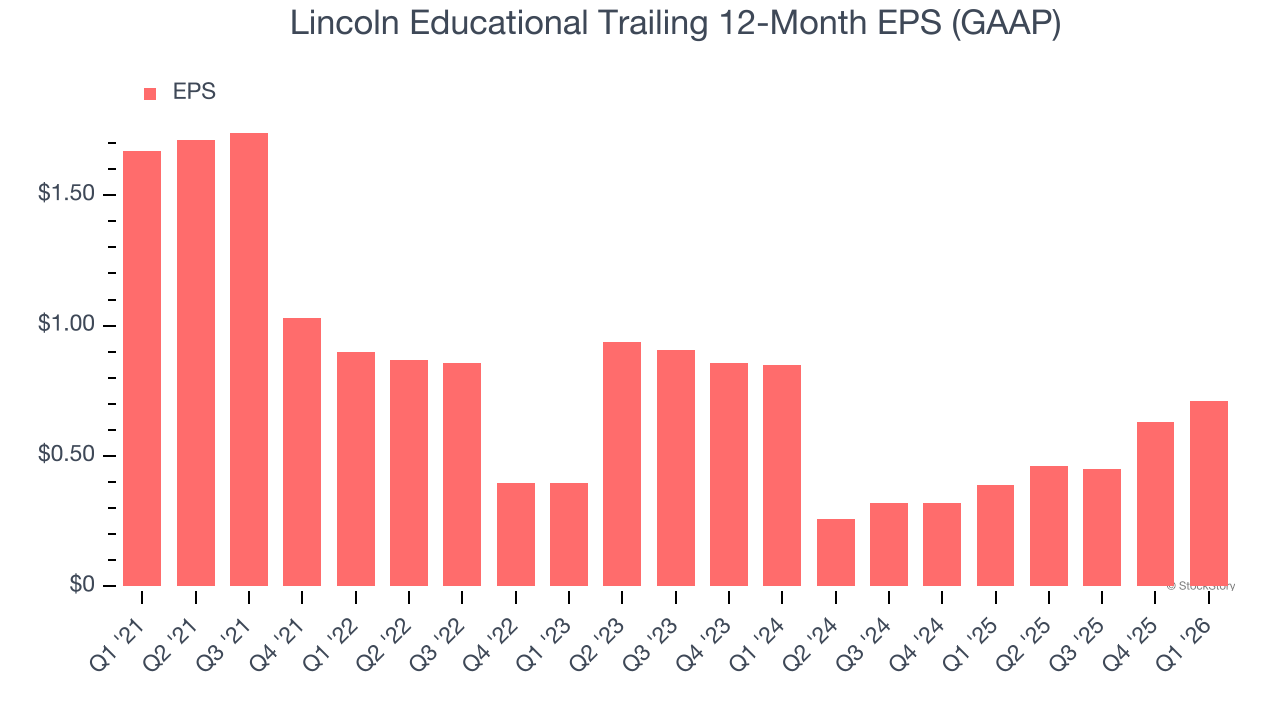

Sadly for Lincoln Educational, its EPS declined by 15.7% annually over the last five years while its revenue grew by 12.6%. This tells us the company became less profitable on a per-share basis as it expanded.

In Q1, Lincoln Educational reported EPS of $0.14, up from $0.06 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Lincoln Educational’s Q1 Results

It was good to see Lincoln Educational beat analysts’ revenue expectations this quarter. We were also excited its EPS outperformed Wall Street’s estimates. Looking ahead, EBITDA and EPS guidance both came in ahead. Zooming out, we think this was a solid print. The stock traded up 2.2% to $45.82 immediately following the results.

Indeed, Lincoln Educational had a rock-solid quarterly earnings result, but is this stock a good investment here? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).