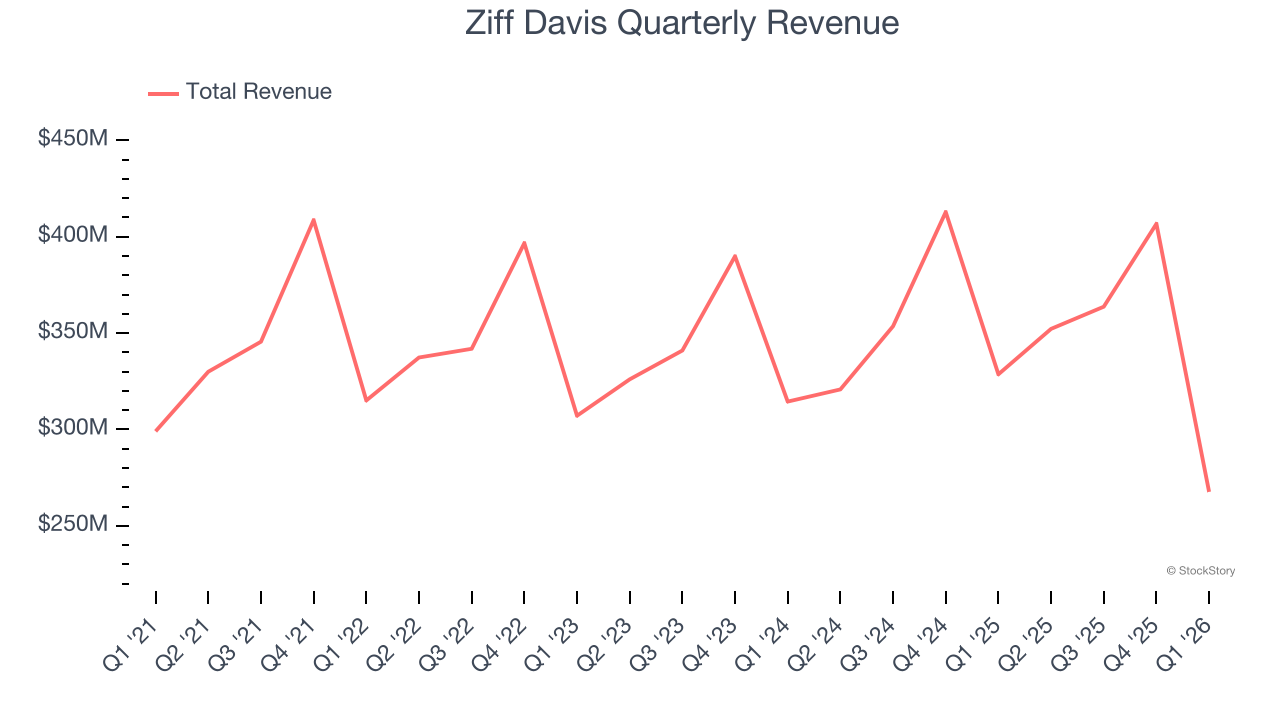

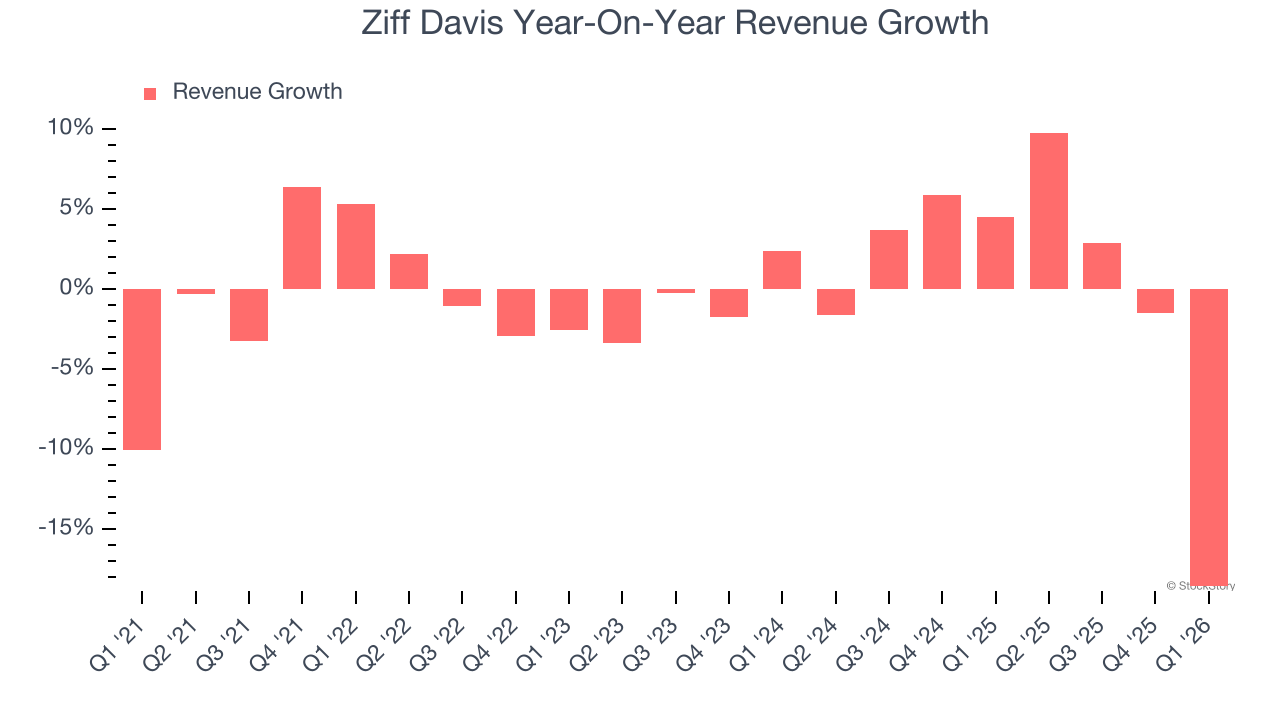

Digital media company Ziff Davis (NASDAQ: ZD) fell short of the market’s revenue expectations in Q1 CY2026, with sales falling 18.6% year on year to $267.6 million. Its non-GAAP profit of $0.73 per share was 5.1% below analysts’ consensus estimates.

Is now the time to buy Ziff Davis? Find out by accessing our full research report, it’s free.

Ziff Davis (ZD) Q1 CY2026 Highlights:

- Revenue: $267.6 million vs analyst estimates of $287.4 million (18.6% year-on-year decline, 6.9% miss)

- Adjusted EPS: $0.73 vs analyst expectations of $0.77 (5.1% miss)

- Adjusted EBITDA: $63.36 million vs analyst estimates of $62.77 million (23.7% margin, 0.9% beat)

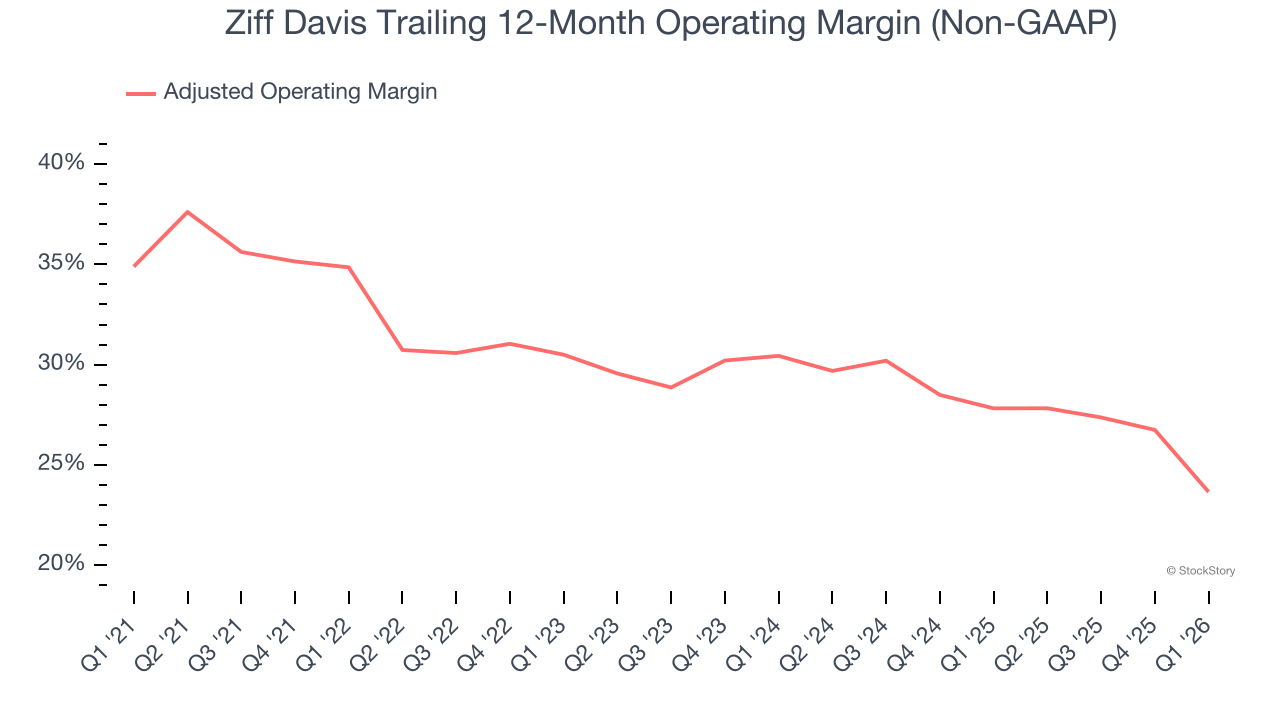

- Operating Margin: 1.1%, down from 10.7% in the same quarter last year

- Free Cash Flow was -$3.17 million compared to -$5.01 million in the same quarter last year

- Market Capitalization: $1.65 billion

“We remain focused on unlocking value for our shareholders as we look to complete the divestiture of the Connectivity business as well as explore additional value-creating transactions,” said Vivek Shah, CEO of Ziff Davis.

Company Overview

Originally a pioneering technology publisher founded in 1927 that became famous for PC Magazine, Ziff Davis (NASDAQ: ZD) operates a portfolio of digital media brands and subscription services across technology, shopping, gaming, healthcare, and cybersecurity markets.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $1.39 billion in revenue over the past 12 months, Ziff Davis is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Ziff Davis struggled to increase demand as its $1.39 billion of sales for the trailing 12 months was close to its revenue five years ago. This shows demand was soft, a tough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Just like its five-year trend, Ziff Davis’s revenue over the last two years was flat, suggesting it is in a slump.

This quarter, Ziff Davis missed Wall Street’s estimates and reported a rather uninspiring 18.6% year-on-year revenue decline, generating $267.6 million of revenue.

Looking ahead, sell-side analysts expect revenue to decline by 4.5% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Adjusted Operating Margin

Ziff Davis has been a well-oiled machine over the last five years. It demonstrated elite profitability for a business services business, boasting an average adjusted operating margin of 29.4%.

Analyzing the trend in its profitability, Ziff Davis’s adjusted operating margin decreased by 11.2 percentage points over the last five years. Even though its historical margin was healthy, shareholders will want to see Ziff Davis become more profitable in the future.

This quarter, Ziff Davis generated an adjusted operating margin profit margin of 5.2%, down 17.1 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

Earnings Per Share

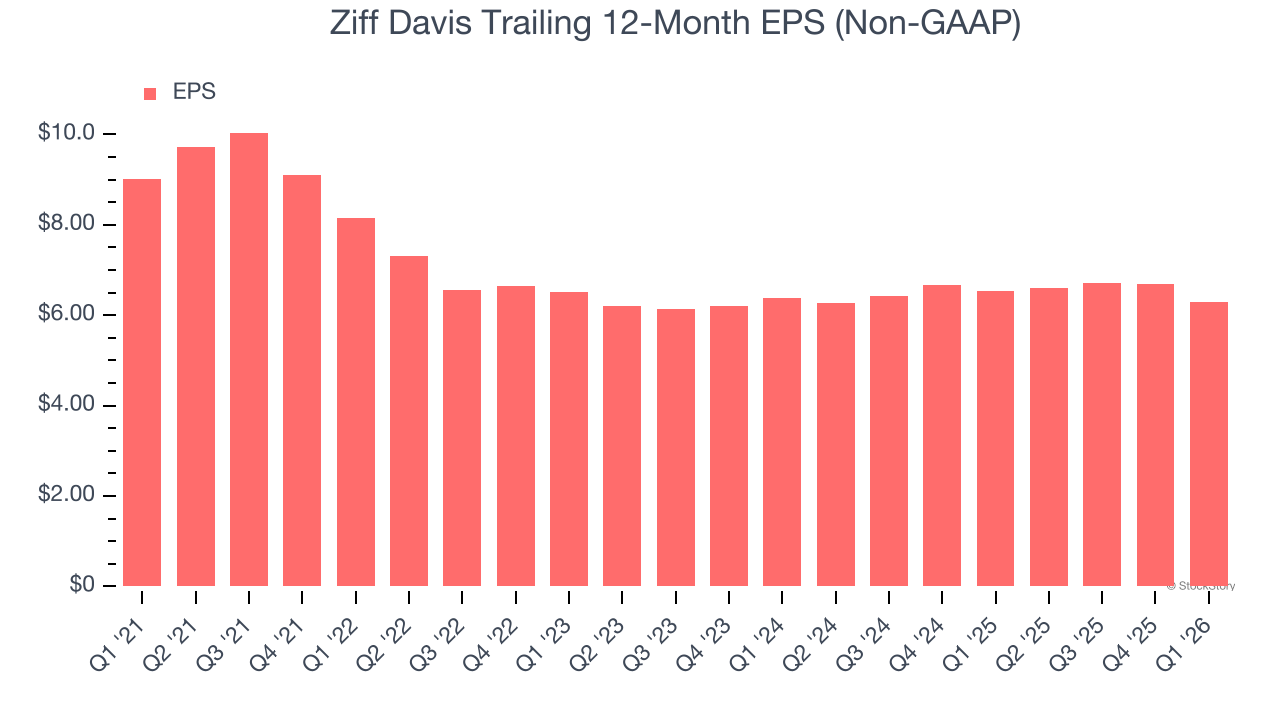

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Ziff Davis, its EPS declined by 7% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

We can take a deeper look into Ziff Davis’s earnings to better understand the drivers of its performance. As we mentioned earlier, Ziff Davis’s adjusted operating margin declined by 11.2 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Ziff Davis, EPS didn’t budge over the last two years, but at least that was better than its five-year trend. We hope its earnings can grow in the coming years.

In Q1, Ziff Davis reported adjusted EPS of $0.73, down from $1.14 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Ziff Davis’s full-year EPS of $6.29 to shrink by 13.2%.

Key Takeaways from Ziff Davis’s Q1 Results

We struggled to find many positives in these results. Its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 1.9% to $42.51 immediately after reporting.

Ziff Davis’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).