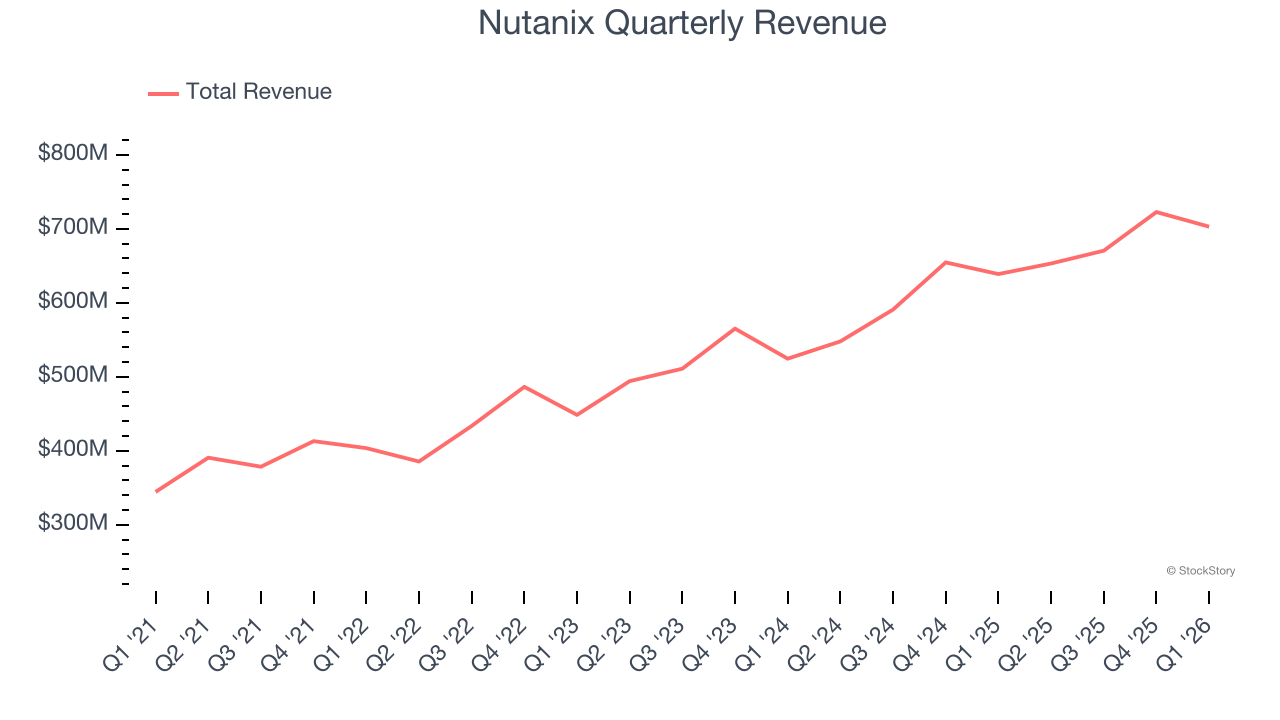

Hybrid multicloud computing company Nutanix (NASDAQ: NTNX) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 10% year on year to $703.1 million. On the other hand, next quarter’s revenue guidance of $735 million was less impressive, coming in 1.1% below analysts’ estimates. Its non-GAAP profit of $0.47 per share was 34.1% above analysts’ consensus estimates.

Is now the time to buy Nutanix? Find out by accessing our full research report, it’s free.

Nutanix (NTNX) Q1 CY2026 Highlights:

- Revenue: $703.1 million vs analyst estimates of $686.3 million (10% year-on-year growth, 2.4% beat)

- Adjusted EPS: $0.47 vs analyst estimates of $0.35 (34.1% beat)

- Adjusted Operating Income: $156.5 million vs analyst estimates of $115.7 million (22.3% margin, 35.2% beat)

- Revenue Guidance for Q2 CY2026 is $735 million at the midpoint, below analyst estimates of $743.5 million

- Operating Margin: 10%, up from 7.6% in the same quarter last year

- Free Cash Flow Margin: 28%, up from 26.5% in the previous quarter

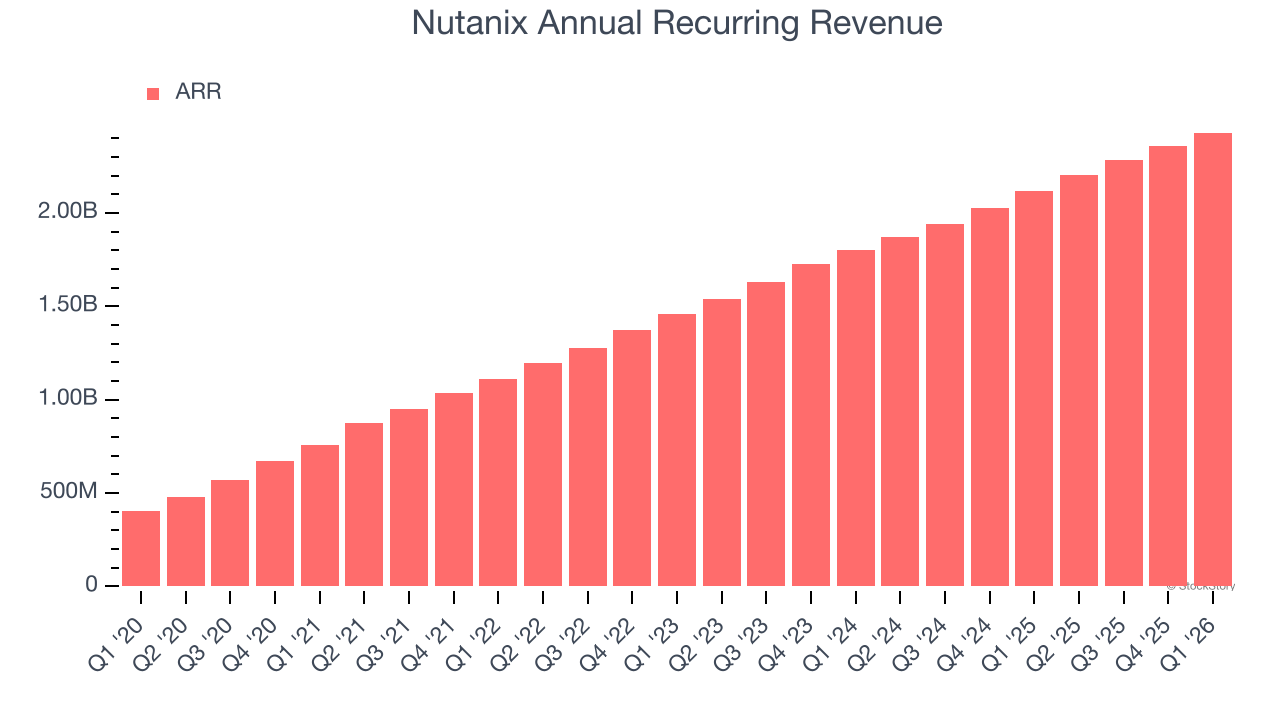

- Annual Recurring Revenue: $2.43 billion vs analyst estimates of $2.42 billion (14.7% year-on-year growth, in line)

- Billings: $812.9 million at quarter end, up 25.3% year on year

- Market Capitalization: $12.54 billion

Company Overview

Originally pioneering hyperconverged infrastructure to break down traditional data center silos, Nutanix (NASDAQ: NTNX) provides a unified software platform that enables organizations to run applications and manage data across private, public, and hybrid cloud environments.

Revenue Growth

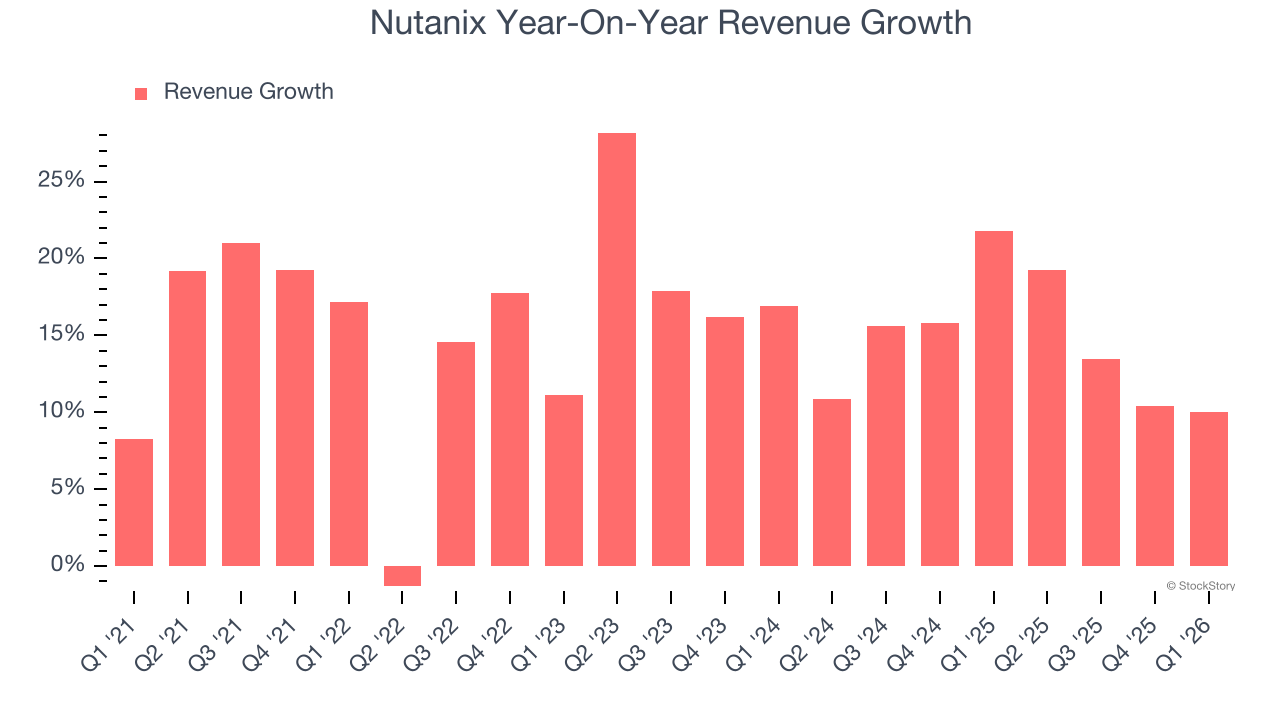

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Nutanix grew its sales at a 15.6% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded. Luckily, there are other things to like about Nutanix.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Nutanix’s recent performance shows its demand has slowed as its annualized revenue growth of 14.6% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Nutanix reported year-on-year revenue growth of 10%, and its $703.1 million of revenue exceeded Wall Street’s estimates by 2.4%. Company management is currently guiding for a 12.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 12.9% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Nutanix’s ARR punched in at $2.43 billion in Q1, and over the last four quarters, its growth slightly outpaced the sector as it averaged 16.5% year-on-year increases. This alternate topline metric grew faster than total sales, which likely means that the recurring portions of the business are growing faster than less predictable, choppier ones such as implementation fees. That could be a good sign for future revenue growth.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Nutanix is very efficient at acquiring new customers, and its CAC payback period checked in at 22.3 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Nutanix more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

Key Takeaways from Nutanix’s Q1 Results

We were impressed by how significantly Nutanix blew past analysts’ billings expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter slightly missed. Zooming out, we think this was a mixed quarter. The stock traded up 2.3% to $47.73 immediately after reporting.

Big picture, is Nutanix a buy here and now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).