Energy prices could be on the verge of a sharp move higher, and the market may not be fully prepared for what comes next. Richard Haass, president emeritus of the Council on Foreign Relations, has warned that prices could “skyrocket” if the Iran war drags on without a diplomatic breakthrough. In his view, the market has underreacted, largely because the full supply disruption has yet to show up in real time.

Tankers that passed through the Strait of Hormuz before tensions escalated are only now reaching destinations such as Europe. Meanwhile, the pipeline behind them has thinned. As incoming supply slows, the market could quickly feel the strain, allowing prices to move higher with little resistance.

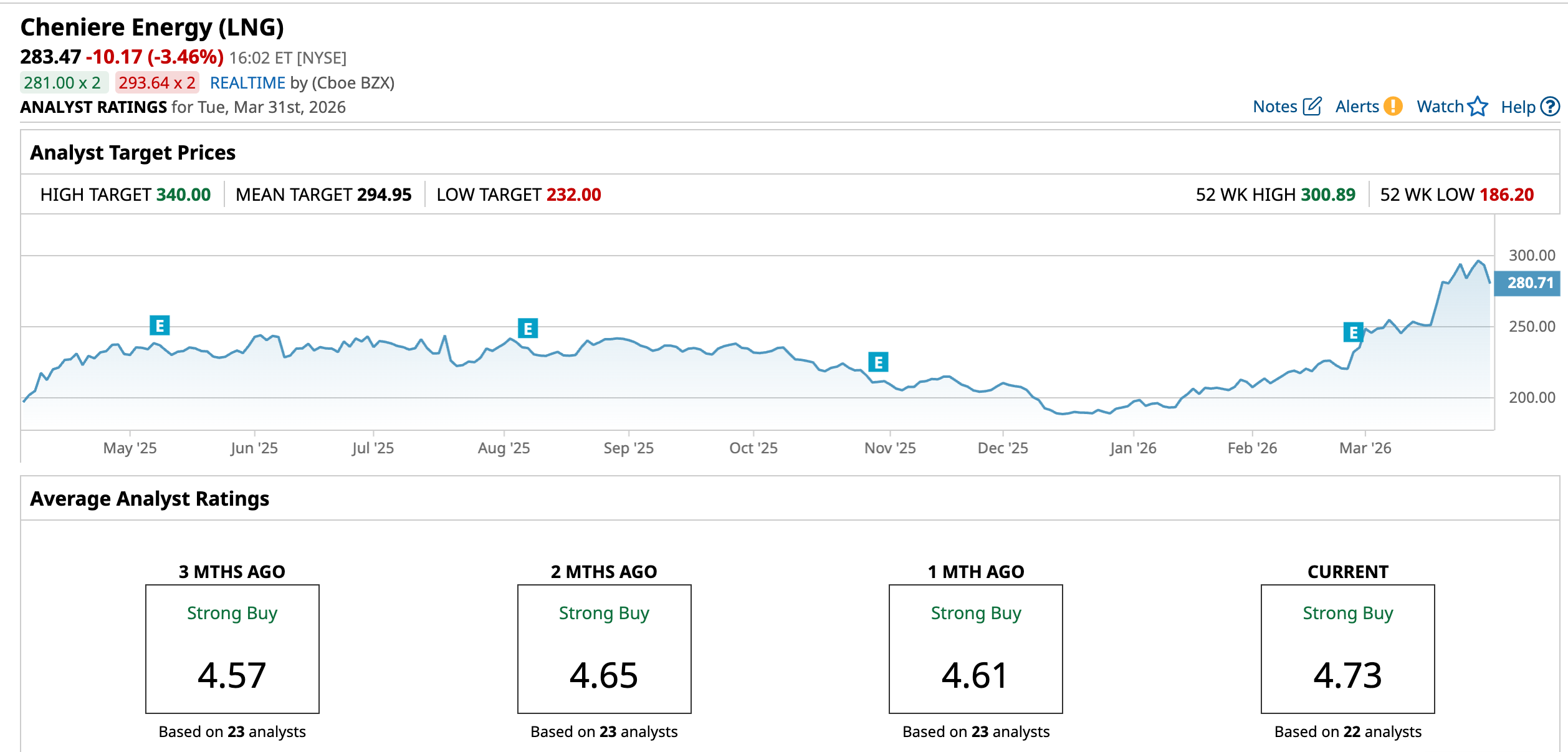

In that environment, Cheniere Energy (LNG) emerges as one of the most compelling ways to play the trend. The stock has already pushed toward $300, reflecting growing investor conviction. With more than 95% of its capacity tied to long-term contracts, the company would secure stable cash flows while preserving upside through uncontracted volumes that can benefit from tighter pricing.

At the same time, Cheniere Energy continues to secure long-term deals, including expanded Thailand orders and a 25-year agreement with Taiwan’s CPC, sharpening earnings visibility. Steady expansions at Sabine Pass and Corpus Christi, paired with a $10 billion buyback and strong cash flow, are strengthening the company’s case as one of the top oil stocks to grab.

About Cheniere Stock

Headquartered in Houston, Texas, Cheniere Energy sits at the heart of the global LNG trade, building and running export terminals at Sabine Pass and Corpus Christi while connecting them to key pipeline networks. The company also markets and trades LNG across major international markets, giving it both scale and reach.

With a market cap of about $61.7 billion, the stock has stayed firmly in rally mode. It has gained 24.35% over the past 52 weeks and surged 44.7% in 2026 alone. In just one month, the stock has jumped 19.34%, reflecting strong momentum as global energy tensions intensify.

From a valuation standpoint, the stock is currently trading at 21.09 times forward adjusted earnings and 2.76 times sales. The figures sit at a premium when compared to the industry averages and their own five-year average multiples.

On the income side, Cheniere has raised dividends for four consecutive years. The company pays an annual dividend of $2.22 per share, offering a yield of 0.76%. Its latest payout of $0.56 per share went out on Feb. 27 to shareholders on record as of Feb. 6.

A Closer Look at Cheniere’s Q4 Earnings

On Feb. 26, Cheniere Energy delivered a strong set of Q4 fiscal 2025 results, wherein revenue climbed 22.9% year-over-year (YOY) to $5.5 billion, coming in comfortably ahead of Street expectations of $5.2 billion. The top line beat reflects robust LNG demand and efficient execution at its core facilities.

Net income surged 135.6% to $2.3 billion, while consolidated adjusted EBITDA rose 29.8% to $2 billion, driven primarily by higher LNG volumes delivered during the quarter. The company generated distributable cash flow of $1.5 billion in Q4 and $5.3 billion for the full year, exceeding the high end of its guidance range by roughly $100 million.

Balance sheet strength remains firmly in place for Cheniere Energy. The company closed the year with $1.1 billion in cash and cash equivalents and total available liquidity of $8.8 billion, giving it ample flexibility to fund growth and navigate volatility. Operationally, it exported 185 LNG cargoes during the quarter, underscoring both scale and consistency.

Looking ahead, the company expects momentum to carry through 2026. Management remains on track to deliver another annual production record, supported by the anticipated completion of the remaining three trains under Stage 3. The expansion should steadily lift output and strengthen its position in a tightening global LNG market.

Guidance reflects confidence. For full-year 2026, management projects consolidated adjusted EBITDA in the range of $6.75 billion to $7.25 billion and distributable cash flow between $4.35 billion and $4.85 billion. It also expects per-unit distributions at CQP to fall between $3.10 and $3.40, reinforcing a strong cash return profile.

Analysts see earnings accelerating sharply. Q1 fiscal 2026 EPS is expected to surge 128% YOY to $3.58. For the full fiscal year 2026, the bottom line is projected to rise 26.1% to $14.08, followed by a further 1.9% increase to $14.35 in fiscal year 2027.

What Do Analysts Expect for Cheniere Stock?

Wall Street has grown increasingly confident in Cheniere Energy. At Goldman Sachs, analyst John Mackay raised his price target from $276 to $312 while maintaining a “Buy” rating on LNG stock. Meanwhile, at Morgan Stanley, Devin McDermott upgraded the stock from “Equal-Weight” to “Overweight” and lifted his target from $236 to $313.

At BofA Securities, Jean Ann Salisbury reaffirmed her “Buy” rating and raised her price target to $322 from $296, keeping pace with improving earnings visibility. At the same time, J.P. Morgan analyst Jeremy Tonet maintained an “Overweight” rating and increased his target to $338 from $279, adding further weight to the bullish narrative.

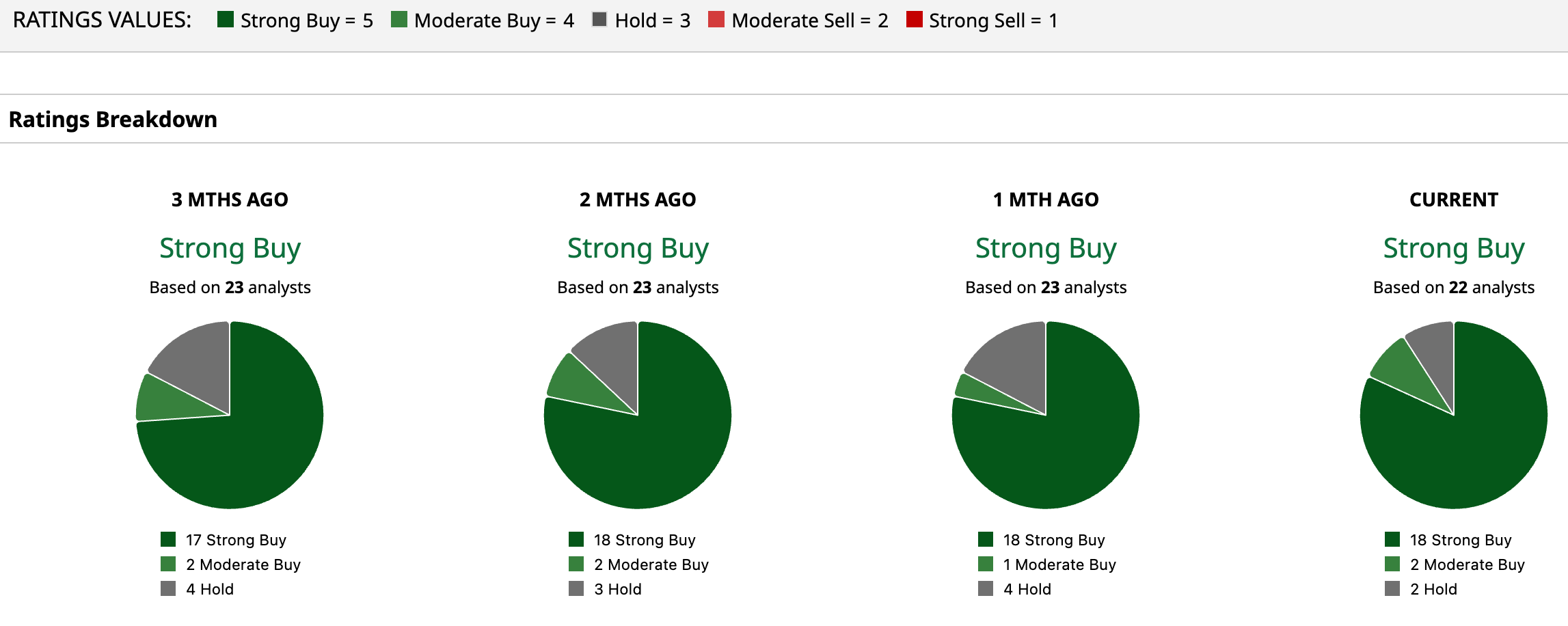

The broader analyst community echoes the optimism. Among 22 analysts covering LNG stock, the overall rating sits at “Strong Buy,” with 18 calling it a “Strong Buy,” two assigning a “Moderate Buy,” and two opting to “Hold.”

To that end, the mean price target of $294.95 signals marginal 4% potential upside. Meanwhile, the Street-high target of $340 suggests a gain of 20% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- This Dividend King Is Down 26%. When Will It Bounce Back?

- Ignore the Panic and Buy the Dip in Micron Stock, Says Bank of America

- Ignore the TurboQuant Panic and Keep Buying Seagate Technology Stock, Says JPMorgan

- Constellation Energy Just Broke Below Its 50-Day Moving Average. Should You Buy the CEG Stock Dip as Company Misses Guidance?